Down More Than 50%: Analysts Say Buy These 2 Beaten-Down Stocks Before They Rebound

Old school investors will tell you that ‘buying low and selling high’ is the key to market success. The advice may be cliché, but it’s based on mathematical truth. The hard part, however, is understanding when prices are low, because that’s not always an absolute number.

In recognizing that lower price range, investors can turn to Wall Street’s analysts for help. These professional stock watchers build their reputations on the quality of their calls, sorting through reams of data to find and recommend just the right stocks.

With this in mind, we’ve used the TipRanks database to pinpoint two beaten-down stocks that analysts believe are gearing up for a rebound. In fact, despite having experienced a decline of over 50% from their most recent peak, the two tickers have scored enough praise from the Street to earn a “Strong Buy” consensus rating. Let’s take a closer look.

SoundThinking, Inc. (SSTI)

We’ll start with SoundThinking, a public safety technology company best known for its sound-based gunshot detection system, used to efficiently direct police to urban hotspots. While the ShotSpotter platform is the firm’s most publicized product, it also offers several other innovative tech services for law enforcement: CrimeTracer, a law enforcement search engine; CaseBuilder, an investigation management system; and ResourceRouter, a software package designed to maximize the efficiency and impact of community anti-violence resources and patrol activities.

By the numbers, SoundThinking has been in business for more than 25 years and has amassed 40 patents for its industry-specific tech. The company has a presence in 64% of the nation’s top 50 metro areas and can boast of a wide customer base, featuring more than 2,000 public safety agencies.

Despite these undoubted successes, SoundThinking has seen its shares fall this year. The stock peaked in late March and has since fallen ~51% from that peak. Pressures on the stock have included the Chicago Mayoral race in April of this year when winning candidate Brandon Johnson indicated that he did not favor retaining the company’s services in the nation’s third-largest city.

At the same time, the company’s revenues have been on an upward trend for most of the last 12 months. In the last quarterly release, 2Q23, SoundThinking reported a top line of $22.1 million, growing 10.3% year-over-year and beating the forecast by ~$144,000. The company’s bottom line numbers were less impressive; SoundThinking’s non-GAAP EPS came in at a 28-cent loss per share, a result that was 25 cents per share below expectations.

On a positive note, SoundThinking reaffirmed its revenue guidance for the full-year 2023, predicting a top line in the range of $92 million to $94 million. This would represent a y/y gain of 15% at the midpoint.

Among the bulls is JMP Securities analyst Trevor Walsh, who is impressed by this firm’s ability to open up a new niche for technology services and sees plenty of room for growth going forward.

“We like SoundThinking over the long term for several reasons, including: 1) an attractive profitability profile with adjusted EBITDA margins that we project to nearly double to 40%; 2) position as the market leader in a relatively uncontested market; 3) a proven technology solution to the growing, persistent problem of gun violence, improving closed case conversion rates which are historically quite low; 4) crime prevention and police patrolling is a frontier ripe for data-driven insights; and 5) continued revenue diversification beyond the core ShotSpotter product as well as into international markets,” Walsh wrote.

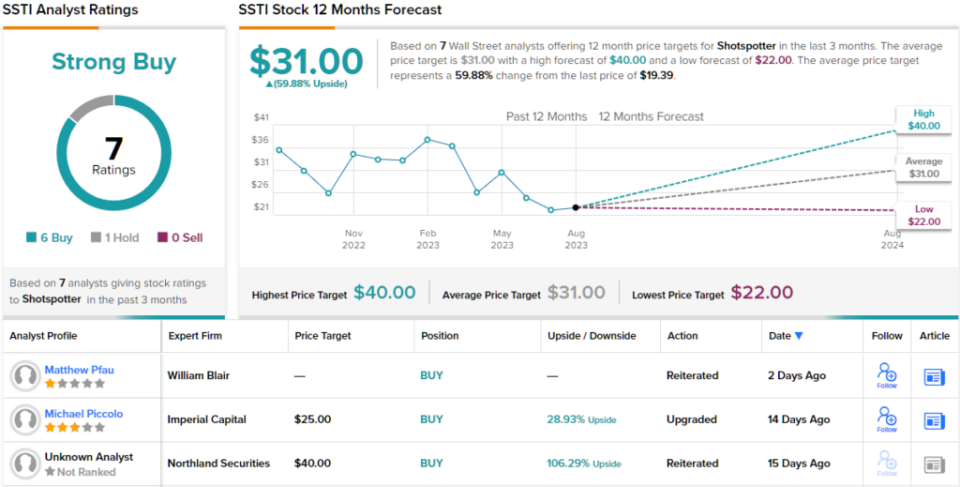

Along with these reasons, Walsh gives SSTI shares an Outperform (i.e. Buy) rating, with a $35 price target that implies a one-year upside potential of ~80%. (To watch Walsh’s track record, click here)

Overall, there are 7 recent analyst reviews here, and the 6 to 1 breakdown, favoring Buys over Holds for a Strong Buy consensus rating, shows that the Street is bullish. SSTI’s $31 average price target suggests ~60% one-year increase from the current share price of $19.39. (See SSTI stock forecast)

Driven Brands Holdings (DRVN)

There are nearly 1.5 billion cars on the world’s roads, and 19% of them, about 280 million vehicles, are in the US. Driven Brands, the largest car-service company in the North American market, offers automotive services through franchise-operated subsidiaries.

Driven Brands divides its operations into several segments: Maintenance, Paint, Collision & Glass, Platform Services, and Carwash. The company’s portfolio includes well-known names in the automotive service industry, such as Meineke, Maaco, and Take 5 Oil Change. These brands are operated through a network of over 4,400 locations, servicing more than 70 million vehicles annually.

The company’s revenues have shown a steady increase over the past several years. This growth trend continued in the second quarter of the current year. During the quarter, Driven Brands opened 74 new locations, and saw same-store sales growth of 8%. System-wide, sales were up 18% to $1.7 billion, and led to a net revenue of $606.9 million, up 19% from 2Q22 – and coming in more than $19 million better than expected.

However, Driven experienced an 18% decline in adjusted net income, amounting to $49.1 million, resulting in a non-GAAP EPS of 29 cents per diluted share. This performance contrasted with the 35-cent EPS reported in the previous year and fell short by 2 cents per share compared to the forecast.

Looking ahead, the company projected a 2023 top-line revenue of $2.3 billion, slightly below the previous guidance of $2.35 billion and the consensus figure of $2.37 billion. The EPS guidance, set at $0.92 per share, also missed expectations, being lower than both the prior guidance of $1.21 and the forecasted $1.23.

Following the earnings release, shares of DRVN experienced a sharp decline. All in all, the stock price tumbled a whopping 53% from its peak back in April of this year.

In the eyes of Piper Sandler’s 5-star analyst, Peter Keith, the current low share price is an opportunity for investors.

“We believe DRVN has potential to generate a 16.5% EBITDA CAGR to achieve its goal in 3.5 years. In particular, we believe unlocking cross-marketing opportunities from DRVN’s extensive CRM database and opening up national insurance to its glass business are two key drivers… We still see tremendous long-term opportunity for DRVN across the healthy aftermarket space, and we expect the Sept 20 analyst day will help to demonstrate cross marketing benefits of DRVN’s extensive CRM database. Finally, shares look inexpensive relative to peers,” Keith opined.

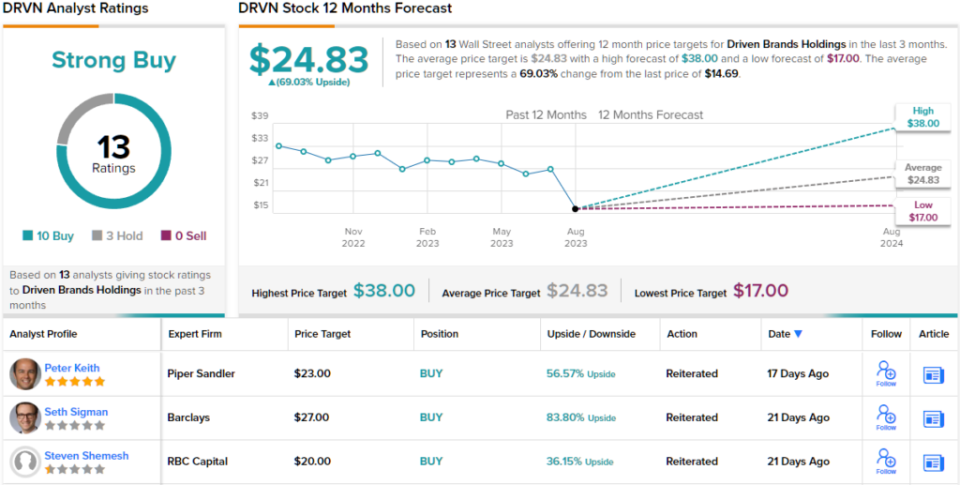

Keith quantifies his bullish stance with an Overweight (i.e. Buy) rating, and a $23 price target that points toward ~57% upside on the one-year horizon. (To watch Keith’s track record, click here)

Overall, Driven Brands has picked up 13 recent analyst reviews, including 10 to Buy and 3 to Hold, for its Strong Buy consensus rating. The shares are priced at $14.69, and the average price target of $24.83 suggests that they will gain 69% going forward into next year. (See DRVN stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.