Dutch Bros (NYSE:BROS) Reports Q4 In Line With Expectations But Full-Year Sales Guidance Misses Expectations

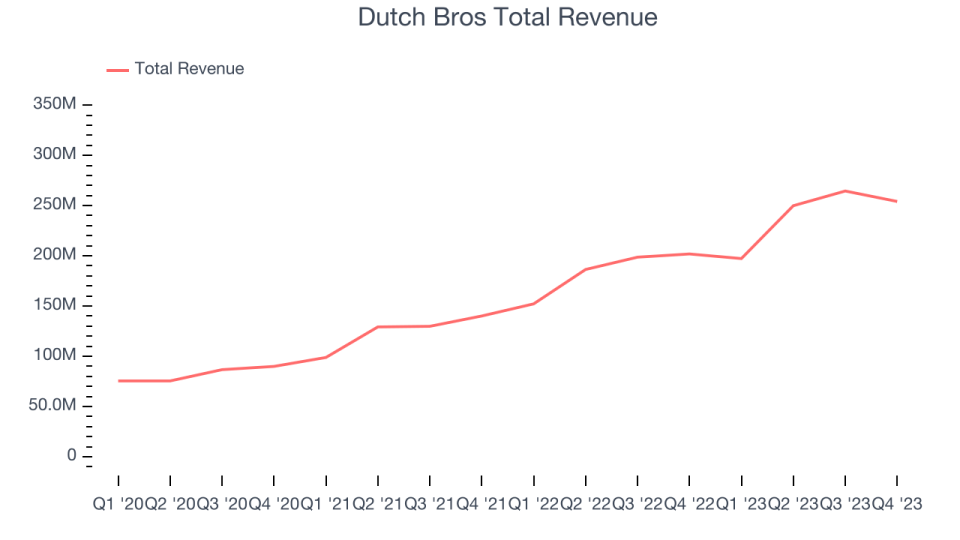

Coffee chain Dutch Bros (NYSE:BROS) reported results in line with analysts' expectations in Q4 FY2023, with revenue up 25.9% year on year to $254.1 million. On the other hand, the company's full-year revenue guidance of $1.20 billion at the midpoint came in 1.9% below analysts' estimates. It made a non-GAAP profit of $0.04 per share, improving from its profit of $0.03 per share in the same quarter last year.

Is now the time to buy Dutch Bros? Find out by accessing our full research report, it's free.

Dutch Bros (BROS) Q4 FY2023 Highlights:

Revenue: $254.1 million vs analyst estimates of $252.9 million (small beat)

EPS (non-GAAP): $0.04 vs analyst estimates of $0.01 ($0.03 beat)

Management's revenue guidance for the upcoming financial year 2024 is $1.20 billion at the midpoint, missing analyst estimates by 1.9% and implying 24% growth (vs 30.7% in FY2023)

Gross Margin (GAAP): 23.3%, down from 26.9% in the same quarter last year

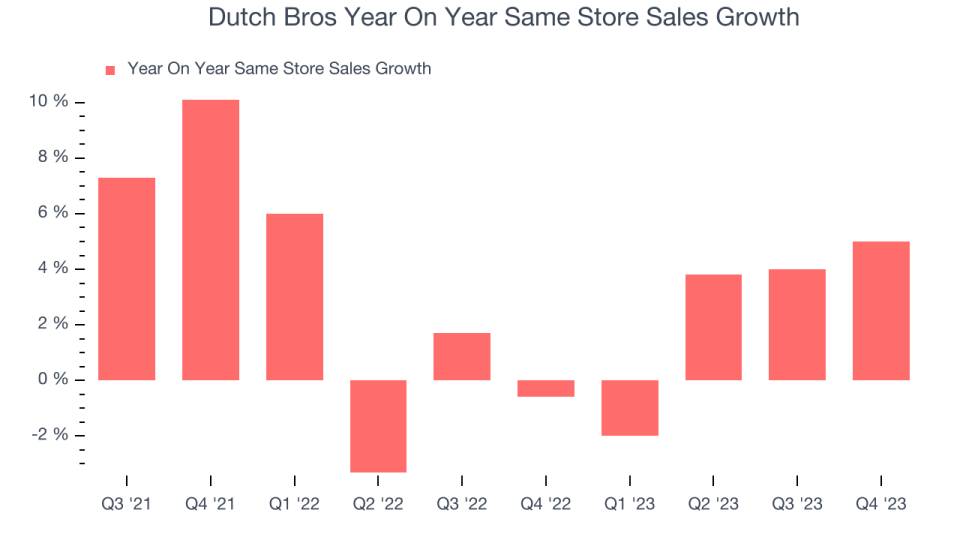

Same-Store Sales were up 5% year on year (beat vs. expectations of up 2.4% year on year)

Store Locations: 831 at quarter end, increasing by 160 over the last 12 months

Market Capitalization: $2.05 billion

Christine Barone, Chief Executive Officer and President of Dutch Bros, stated, “We had an exceptional 2023 and entered 2024 with great momentum. We continued to drive steady new shop growth, and Q4 marked our 10th consecutive quarter of 30+ new shop openings. In 2023, we opened 159 shops, of which 146 were company-operated. Our system AUV reached its highest on record since the IPO, and we delivered a 2.8% increase in system same shop sales growth. These results led to a terrific 2023 where we delivered 31% in annual revenue growth. Early last year, we began a series of traffic-driving initiatives outlined on our Q1 call in May. We saw the impact of these efforts culminate with a 5.0% increase in system same shop sales in Q4, driven by a sequential improvement in customer traffic.”

Started in 1992 by two brothers as a single pushcart, Dutch Bros (NYSE:BROS) is a dynamic coffee chain that’s captured the hearts of coffee enthusiasts across the United States.

Traditional Fast Food

Traditional fast-food restaurants are renowned for their speed and convenience, boasting menus filled with familiar and budget-friendly items. Their reputations for on-the-go consumption make them favored destinations for individuals and families needing a quick meal. This class of restaurants, however, is fighting the perception that their meals are unhealthy and made with inferior ingredients, a battle that's especially relevant today given the consumers increasing focus on health and wellness.

Sales Growth

Dutch Bros is a mid-sized restaurant chain, which sometimes brings disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale. On the other hand, Dutch Bros can still achieve high growth rates because its revenue base is not yet monstrous.

As you can see below, the company's annualized revenue growth rate of 41.9% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was incredible as it added more dining locations and increased sales at existing, established restaurants.

This quarter, Dutch Bros's year-on-year revenue growth of 25.9% was excellent, and its $254.1 million in revenue was in line with Wall Street's estimates. Looking ahead, Wall Street expects sales to grow 26.2% over the next 12 months, an acceleration from this quarter.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Same-Store Sales

Dutch Bros's demand within its existing restaurants has been relatively stable over the last eight quarters but fallen behind the broader sector. On average, the company's same-store sales have grown by 1.8% year on year. With positive same-store sales growth amid an increasing number of restaurants, Dutch Bros is reaching more diners and growing sales.

In the latest quarter, Dutch Bros's same-store sales rose 5% year on year. This growth was a well-appreciated turnaround from the 0.6% year-on-year decline it posted 12 months ago, showing the business is regaining momentum.

Key Takeaways from Dutch Bros's Q4 Results

We liked how Dutch Bros beat same-store sales and EPS expectations this quarter. We were also happy its revenue narrowly outperformed Wall Street's estimates. On the other hand, its gross margin missed analysts' expectations and its full-year revenue guidance missed Wall Street's estimates. Overall, the results could have been better. The stock is flat after reporting and currently trades at $27 per share.

Dutch Bros may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.