DXC Technology Co Reports Mixed Q3 FY24 Results Amid Share Buyback and Free Cash Flow Growth

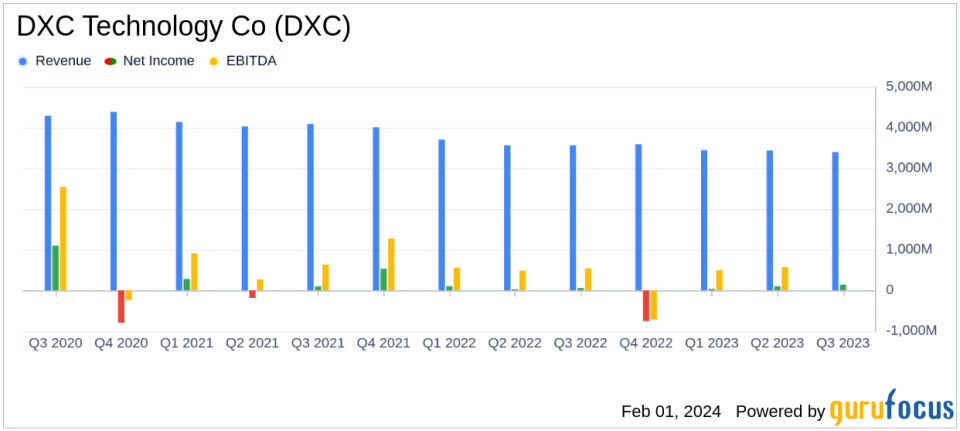

Revenue: $3.40 billion, a decrease of 4.7% year-over-year.

Net Income: Improved to $140 million, representing 4.1% of sales.

Free Cash Flow: Increased to $585 million, up from $463 million in Q3 FY23.

Earnings Per Share (EPS): Diluted EPS rose to $0.81, Non-GAAP diluted EPS was $0.87.

Share Buyback: $252 million returned to shareholders, reducing shares outstanding by 5.8%.

Book-to-Bill Ratio: Stood at 0.99x for the quarter, with a trailing twelve-month ratio of 0.93x.

On February 1, 2024, DXC Technology Co (NYSE:DXC) released its third-quarter fiscal year 2024 results, revealing a mix of challenges and financial achievements. The company's 8-K filing shows a revenue decline but improvements in net income and free cash flow, alongside an aggressive share buyback program.

Company Overview

DXC Technology Co is a leading independent IT services provider, with a focus on Global Business Services (GBS) and Global Infrastructure Services (GIS). The company primarily generates revenue from its GIS segment, which includes Cloud and Security, IT Outsourcing, and Modern Workplace services. DXC has a strong presence in the Other Europe region, which contributes the majority of its revenue.

Performance and Challenges

DXC's revenue for the quarter was $3.40 billion, marking a 4.7% decrease compared to the previous year. This decline reflects a 4.5% drop on an organic basis. Despite the revenue challenges, the company's net income rose to $140 million, or 4.1% of sales, compared to $61 million, or 1.7% of sales, in the prior year's quarter. This improvement was attributed to gains on the sale of businesses, lower depreciation and amortization, and reduced restructuring costs.

The company's performance is critical as it indicates the effectiveness of DXC's strategy in a competitive IT services market. However, the revenue decline poses potential problems, signaling the need for DXC to adapt to market demands and enhance its service offerings.

Financial Achievements

DXC's financial achievements this quarter are noteworthy, particularly the significant increase in free cash flow to $585 million, up from $463 million in the same quarter last year. This metric is crucial for the company's ability to invest in growth initiatives, reduce debt, and return value to shareholders through buybacks and dividends.

The company's aggressive share repurchase program, which returned $252 million to shareholders and reduced outstanding shares by 5.8%, underscores management's confidence in DXC's value proposition and commitment to enhancing shareholder returns.

Financial Metrics and Commentary

Key financial metrics from DXC's earnings report include:

"We achieved or exceeded our third quarter organic revenue, adjusted EBIT and non-GAAP EPS guidance and delivered $585 million of free cash flow in the quarter," said Raul Fernandez, Chief Executive Officer of DXC.

This commentary highlights the company's ability to meet its financial targets despite the revenue downturn, showcasing operational efficiency and cost management.

Segment Performance

The GBS segment saw a slight organic revenue growth of 0.3%, driven by growth in Analytics & Engineering and Insurance offerings. However, segment profit margin declined to 11.9%, down from 14.0% in the prior year. The GIS segment experienced a revenue decline of 6.8% year-over-year, with organic revenue growth down by 8.9%. Despite this, the segment profit margin improved slightly to 7.1%.

Analysis and Outlook

DXC's mixed financial results reflect the company's resilience in generating cash flow and managing costs amidst revenue headwinds. The company's focus on share buybacks and maintaining a healthy book-to-bill ratio indicates a strategic approach to driving shareholder value and positioning for future growth.

For the upcoming quarter and full fiscal year 2024, DXC has adjusted its guidance, reflecting a more conservative outlook on organic revenue growth and adjusted EBIT margin. However, the company maintains its free cash flow guidance of $800 million, signaling confidence in its cash-generating capabilities.

DXC Technology's earnings report presents a complex picture of a company navigating industry challenges while maintaining financial discipline and a commitment to shareholder returns. For value investors, DXC's ability to generate free cash flow and execute share buybacks may be attractive, even as the company faces the need to drive revenue growth in a competitive market.

For more detailed analysis and up-to-date financial news, visit GuruFocus.com.

Explore the complete 8-K earnings release (here) from DXC Technology Co for further details.

This article first appeared on GuruFocus.