Dynatrace Is Positioned for High Growth Through AI Monitoring

Investors looking for quality exposure to advanced technology companies would be wise to carefully review their options. I believe a bubble may form in the markets as artificial intelligence proliferates and investor sentiment over companies involved with AI products and services increases to speculative levels. Nonetheless, based on my sensitive valuation analysis of Dynatrace Inc. (NYSE:DT), I consider it moderately undervalued. I believe it offers strong operations and financials to compete effectively in the markets over the long term.

Company overview and updates

Dynatrace is a specialist in software intelligence, evolving from application performance management to a leader in cloud-based, automatic and intelligent full-stack monitoring. Its key offerings are outlined as follows:

Full-stack monitoring o ffers a comprehensive suite of monitoring tools for a full view of enterprise IT environments, including the performance of applications underlying the hardware and network.

As for AI and automation, the company has an AI engine called Davis, which automatically detects and diagnoses problems in real-time, often before users are impacted. It improves efficiency and reduces manual oversight across a range of applications.

Cloud-native support provides visibility and insights into the performance of cloud applications and infrastructure, optimizing performance and reducing costs.

Digital experience monitoring offers tools for real-user monitoring and synthetic monitoring of web and mobile applications, optimizing the end-user experience across different digital channels.

Security offers application security, helping to identify and mitigate vulnerabilities in development operations early on.

Dynatrace's Perform 2024 conference showcased its focus on AI-supported analytics and automation. It recently announced partnerships with major cloud providers like Amazon (NASDAQ:AMZN) Web Services, Microsoft (NASDAQ:MSFT) and Alphabet's (GOOGL) Google Cloud. The aim of these partnerships is to simplify cloud migration, enhance cloud architecture and optimize efficiency. For example, Dynatrace integrated into the AWS Migration Hub to assist in cloud migration, providing performance insights and security post-migration.

In its earnings report for the fiscal third quarter of 2024, it recorded 23% year-over-year growth in total annual recurring revenue to $1.43 billion. Subscription revenue increased 25% and management highlighted a strong non-GAAP operating margin of 29%. It also outlined strategic acquisitions, including Runecast, to enhance its AI-powered security and compliance capabilities. Notably, in the last three months, analyst earnings estimates have seen 28 upward revisions, indicating increasing sentiment for the stock.

Competition and market analysis

There are a range of companies that are directly competing with Dynatrace in its field of operations. However, narrowing these down to two significant peers with worthy competitive traits, I have opted for Datadog (NASDAQ:DDOG) and Splunk (NASDAQ:SPLK).

Datadog is known for comprehensive cloud monitoring services, including infrastructure, application performance monitoring and log management. Its machine learning focus and integration capabilities make it a significant competitor. Splunk specializes in analyzing machine-generated data. Its focus is on security and full-stack monitoring and analysis, catering to many Fortune 100 companies. Consider the following statistics for competitive analysis:

Dynatrace: Equity-to-asset ratio of 0.64, net margin of 14.44%, three-year revenue growth rate of 24.50% and forward price-earnings ratio of 37.40.

Datadog: Equity-to-asset ratio of 0.52, net margin of 2.28%, three-year revenue growth rate of 44.60% and forward price-earnings ratio of 82.17.

Splunk: Equity-to-asset ratio of 0.11, net margin of 6.26%, three-year revenue growth rate of 19.90% and forward price-earnings ratio of 23.72.

Dynatrace appears to be the strongest of the three based on core metrics, with a more stable balance sheet, higher net margin and much more favorable valuation when compared to Datadog.

To understand the significant growth opportunity related to all three companies, consider Mordor Intelligence's estimate of a 30.75% comound annual growth ratio from 2024 to 2029 for the application performance management market. On the other hand, The Business Research Company offers a more conservative 12.80% CAGR estimate for the application performance monitoring market from 2024 to 2028. If we consider a mid-level outcome, an indicated market CAGR of around 20% seems reasonable and achievable over the next five years.

Further considerations and risk mitigation

Dynatrace's strong balance sheet is supported by its cash flow statement, where it has only issued debt once since 2017 for $1.12 billion. Since this issuance in 2019, it has repaid significant portions of the debt every year on record. In addition, it has not favored the repurchase of common stock over debt repayments, which I believe is prudent. However, I believe if the company continues to maintain its strong capital structure, it can begin to repurchase common stock to bolster shareholder value at no significant detriment to the balance sheet, considering its equity-to-asset ratio of 0.64 at the time of writing.

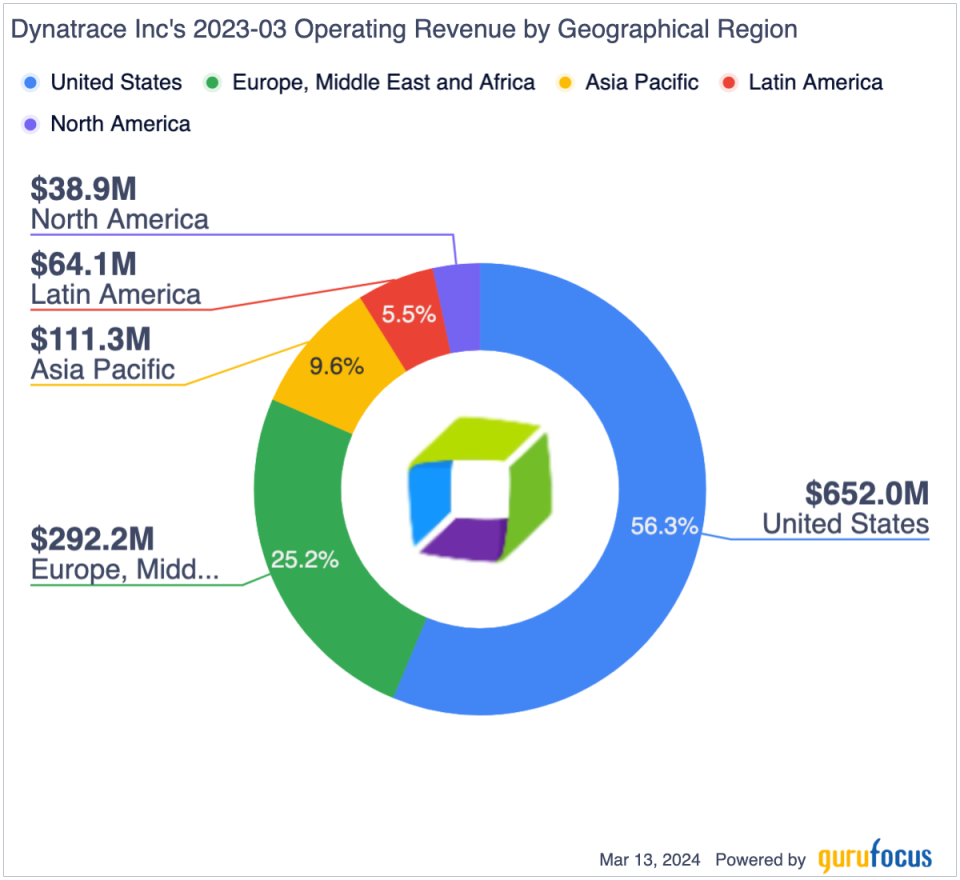

Additionally, investors should consider the geographic diversification provided by the shares useful for risk mitigation. While 56.30% of its operating revenue comes from the United States, a large portion of its operating revenue comes from a range of diverse economies, reducing revenue depletion from localized economic recessions.

That being said, the company is a pure technology company and is heavily concentrated on cloud and AI-led data analysis, so I believe investors would be wise to consider the valuation risk that comes with investing in technology companies at this time. The largest potential long-term problem could be reduced investor sentiment in the technology markets during a period when I believe AI has the potential to recreate a stock market bubble akin to the 1990s internet boom. If this happens, even great companies, which I believe Dynatrace is, will likely face a large pullback in price as investor sentiment wanes and the excellent companies correct to a more appropriate valuation over time. It is crucial, therefore, to select based on operational strengths, business structure and financial management positives rather than relying too heavily on market CAGR forecasts and high momentum indicators to support investment decisions in risky niche AI-integrated companies.

Value analysis

Dynatrace is trading at a significant premium to what is usual for U.S. stocks. Consider the S&P 500's 10-year median price-earnings ratio of 20.60. While Dynatrace has a 10-year median of 193.4, it has been at a loss for all years other than the past three. Consider also the sector median price-earnings ratio of 28. I believe it is difficult to get a nuanced understanding of fair value for a stock with a history of such a premium over both its sector and the wider economy's norm, as well as the fact that it is early on in reporting profitability.

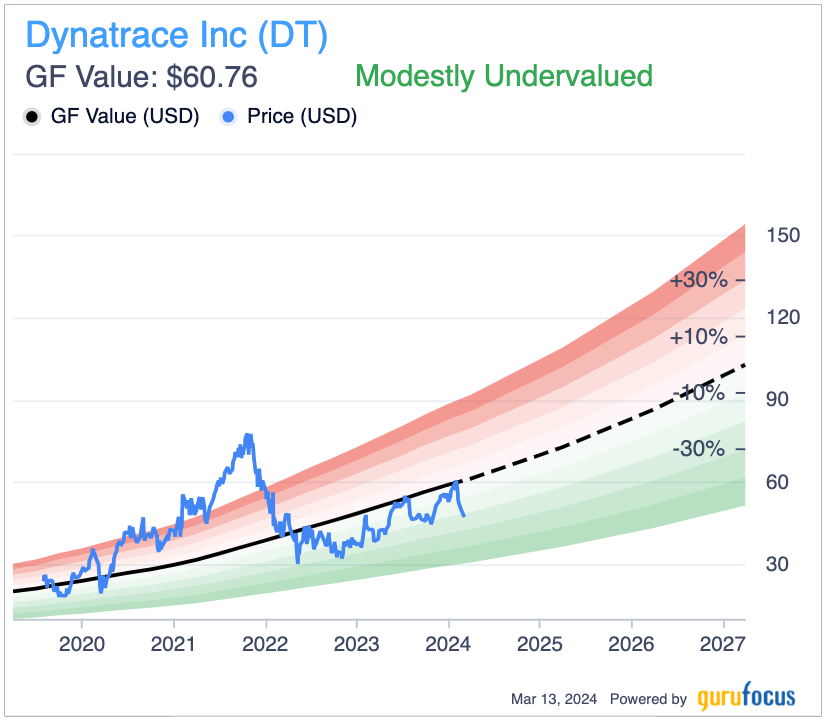

The GF Value Line indicates a moderate undervaluation, a mix of ratios blended with historical and future earnings estimates through an algorithm that is undisclosed. However, I believe it does an excellent job of pricing in the value of investor sentiment and grounding this in earnings results.

As the company is trading over 40% below its high, we could reduce its 10-year median price-earnings ratio by 40%, arriving at 116.03 as a fair reflection of reduced investor sentiment as it relates to earnings. However, as earnings are growing significantly, the price-earnings ratio is actually 70.76, indicating what could be deemed a 39% undervaluation. We can also then reduce this margin of safety by the negative premium Dynatrace has compared to the software industry's median price-earnings ratio of 27.79 of -60.73%. That indicates an 11.81% margin of safety at the time of writing based on my analysis.

Notable risks

I reiterate that my sensitive and nuanced approach to the valuation, which incorporates a high value on investor sentiment, comes with a set of risks in how the market may change its mind around the technology industry, which could result in much higher downside volatility than when investing for value through a discounted cash flow analysis. This is one of the main risks that investors face when allocating to technology stocks with a premium, and the risk goes up with companies that are newly profitable or yet to report profitability.

Additionally, operational hazards include cybersecurity threats that, if not managed effectively, could result in significant reputational damage. 2023 saw multiple security threats to notable companies, including PayPal (NASDAQ:PYPL) experiencing a credential stuffing attack, DISH Network (DISH) suffering a ransomware attack leading to a data breach and GoDaddy (NYSE:GDDY) disclosed a multiyear breach where source code had been stolen and malware installed. Considering these were not the only high-profile breaches, this represents the very real and prescient need for high levels of advanced cybersecurity. Thankfully, Dynatrace's balance sheet positions it well to fund expansions in its security efforts.

Conclusion

In summary, Dynatrace offers concentrated exposure to advanced application performance management, and it is one of the leaders in its space with what I believe are the best financials among peers, supporting an investment decision. While my analysis reveals a moderate undervaluation, akin to that predicted by the GF Value chart, I believe investors would be wise to consider the higher risk that comes with investing for value without a typical DCF analysis. While return can be higher, so can losses. However, if investors are willing to take on slightly more risk for more reward with the investment, my analyst rating for the stock is a buy.

This article first appeared on GuruFocus.