Eastern Platinum (TSE:ELR) Shareholders Will Want The ROCE Trajectory To Continue

If you're not sure where to start when looking for the next multi-bagger, there are a few key trends you should keep an eye out for. Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. If you see this, it typically means it's a company with a great business model and plenty of profitable reinvestment opportunities. So on that note, Eastern Platinum (TSE:ELR) looks quite promising in regards to its trends of return on capital.

What Is Return On Capital Employed (ROCE)?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. To calculate this metric for Eastern Platinum, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

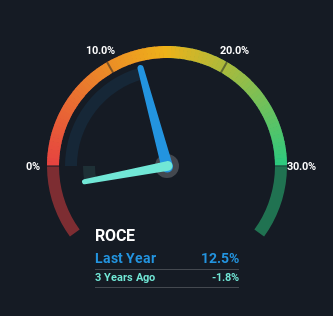

0.12 = US$11m ÷ (US$158m - US$71m) (Based on the trailing twelve months to September 2023).

So, Eastern Platinum has an ROCE of 12%. On its own, that's a standard return, however it's much better than the 1.8% generated by the Metals and Mining industry.

See our latest analysis for Eastern Platinum

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you'd like to look at how Eastern Platinum has performed in the past in other metrics, you can view this free graph of Eastern Platinum's past earnings, revenue and cash flow.

What Does the ROCE Trend For Eastern Platinum Tell Us?

Like most people, we're pleased that Eastern Platinum is now generating some pretax earnings. The company was generating losses five years ago, but now it's turned around, earning 12% which is no doubt a relief for some early shareholders. Additionally, the business is utilizing 46% less capital than it was five years ago, and taken at face value, that can mean the company needs less funds at work to get a return. Eastern Platinum could be selling under-performing assets since the ROCE is improving.

On a side note, we noticed that the improvement in ROCE appears to be partly fueled by an increase in current liabilities. The current liabilities has increased to 45% of total assets, so the business is now more funded by the likes of its suppliers or short-term creditors. And with current liabilities at those levels, that's pretty high.

The Bottom Line

From what we've seen above, Eastern Platinum has managed to increase it's returns on capital all the while reducing it's capital base. Given the stock has declined 49% in the last five years, this could be a good investment if the valuation and other metrics are also appealing. That being the case, research into the company's current valuation metrics and future prospects seems fitting.

One more thing: We've identified 4 warning signs with Eastern Platinum (at least 1 which is concerning) , and understanding them would certainly be useful.

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.