Is Elders Limited’s (ASX:ELD) PE Ratio A Signal To Buy For Investors?

This analysis is intended to introduce important early concepts to people who are starting to invest and want to learn about the link between company’s fundamentals and stock market performance.

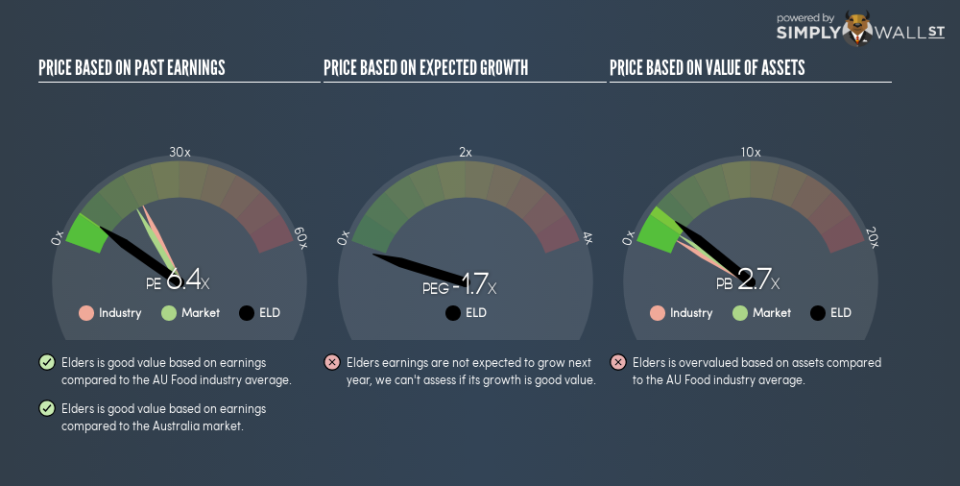

Elders Limited (ASX:ELD) trades with a trailing P/E of 6.4x, which is lower than the industry average of 19.2x. While this makes ELD appear like a great stock to buy, you might change your mind after I explain the assumptions behind the P/E ratio. In this article, I will break down what the P/E ratio is, how to interpret it and what to watch out for.

See our latest analysis for Elders

What you need to know about the P/E ratio

The P/E ratio is one of many ratios used in relative valuation. By comparing a stock’s price per share to its earnings per share, we are able to see how much investors are paying for each dollar of the company’s earnings.

P/E Calculation for ELD

Price-Earnings Ratio = Price per share ÷ Earnings per share

ELD Price-Earnings Ratio = A$6.67 ÷ A$1.039 = 6.4x

The P/E ratio isn’t a metric you view in isolation and only becomes useful when you compare it against other similar companies. We want to compare the stock’s P/E ratio to the average of companies that have similar characteristics as ELD, such as size and country of operation. One way of gathering a peer group is to use firms in the same industry, which is what I’ll do. Since ELD’s P/E of 6.4 is lower than its industry peers (19.2), it means that investors are paying less for each dollar of ELD’s earnings. This multiple is a median of profitable companies of 20 Food companies in AU including Jiajiafu Modern Agriculture, Bojun Agriculture Holdings and Dongfang Modern Agriculture Holding Group. You can think of it like this: the market is suggesting that ELD is a weaker business than the average comparable company.

Assumptions to watch out for

However, it is important to note that this conclusion is based on two key assumptions. The first is that our “similar companies” are actually similar to ELD, or else the difference in P/E might be a result of other factors. For example, if you compared lower risk firms with ELD, then investors would naturally value it at a lower price since it is a riskier investment. The second assumption that must hold true is that the stocks we are comparing ELD to are fairly valued by the market. If this does not hold, there is a possibility that ELD’s P/E is lower because our peer group is overvalued by the market.

What this means for you:

You may have already conducted fundamental analysis on the stock as a shareholder, so its current undervaluation could signal a good buying opportunity to increase your exposure to ELD. Now that you understand the ins and outs of the PE metric, you should know to bear in mind its limitations before you make an investment decision. Remember that basing your investment decision off one metric alone is certainly not sufficient. There are many things I have not taken into account in this article and the PE ratio is very one-dimensional. If you have not done so already, I highly recommend you to complete your research by taking a look at the following:

Future Outlook: What are well-informed industry analysts predicting for ELD’s future growth? Take a look at our free research report of analyst consensus for ELD’s outlook.

Past Track Record: Has ELD been consistently performing well irrespective of the ups and downs in the market? Go into more detail in the past performance analysis and take a look at the free visual representations of ELD’s historicals for more clarity.

Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

To help readers see past the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price-sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned. For errors that warrant correction please contact the editor at editorial-team@simplywallst.com.