Energizer (NYSE:ENR) Exceeds Q1 Expectations

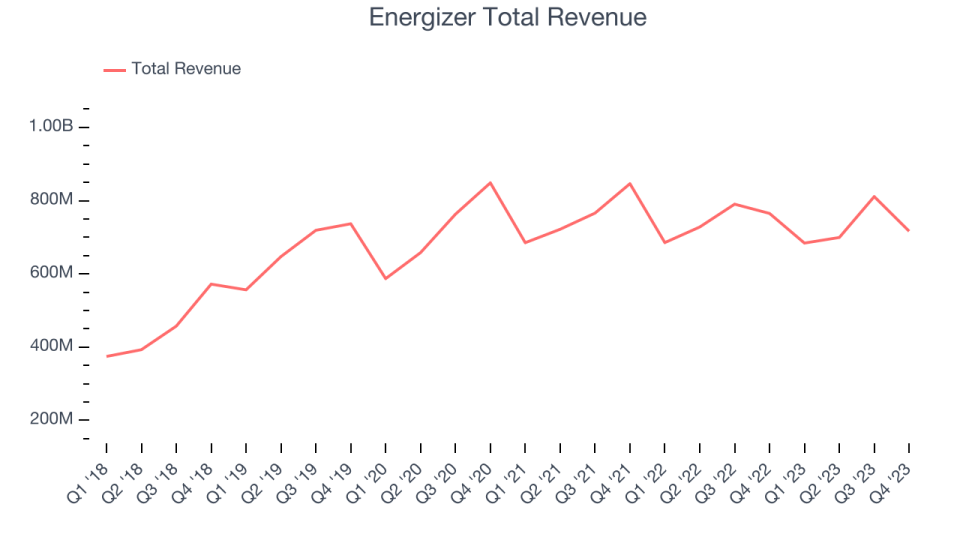

Battery and lighting company Energizer (NYSE:ENR) reported Q1 FY2024 results topping analysts' expectations , with revenue down 6.3% year on year to $716.6 million. It made a non-GAAP profit of $0.59 per share, down from its profit of $0.72 per share in the same quarter last year.

Is now the time to buy Energizer? Find out by accessing our full research report, it's free.

Energizer (ENR) Q1 FY2024 Highlights:

Revenue: $716.6 million vs analyst estimates of $710.8 million (0.8% beat)

EPS (non-GAAP): $0.59 vs analyst estimates of $0.57 (4.1% beat)

EPS (non-GAAP) Guidance for Q2 2024 is $0.68 at the midpoint, below analyst estimates of $0.70

EPS (non-GAAP) Guidance for full year 2024 is $3.20 at the midpoint, in line with analyst estimates

Free Cash Flow of $152.6 million, up 96.9% from the previous quarter

Gross Margin (GAAP): 37.3%, down from 39% in the same quarter last year

Organic Revenue was down 7.4% year on year (miss)

Market Capitalization: $2.23 billion

"Execution against our strategies yielded results in line with our expectations and provides a solid start to the fiscal year," said Mark LaVigne, Chief Executive Officer.

Masterminds behind the viral Energizer Bunny mascot, Energizer (NYSE:ENR) is one of the world's largest manufacturers of batteries.

Household Products

Household products companies engage in the manufacturing, distribution, and sale of goods that maintain and enhance the home environment. This includes cleaning supplies, home improvement tools, kitchenware, small appliances, and home decor items. Companies within this sector must focus on product quality, innovation, and cost efficiency to remain competitive. Household products stocks are generally stable investments, as many of the industry's products are essential for a comfortable and functional living space. Recently, there's been a growing emphasis on eco-friendly and sustainable offerings, reflecting the evolving consumer preferences for environmentally conscious options.

Sales Growth

Energizer carries some recognizable brands and products but is a mid-sized consumer staples company. Its size could bring disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale. On the other hand, Energizer can still achieve high growth rates because its revenue base is not yet monstrous.

As you can see below, the company's revenue was flat over the last three years. This is poor for a consumer staples business.

This quarter, Energizer reported a rather uninspiring 6.3% year-on-year revenue decline to $716.6 million in revenue, in line with Wall Street's estimates. Looking ahead, Wall Street expects revenue to remain flat over the next 12 months.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Key Takeaways from Energizer's Q1 Results

While organic revenue missed, it was encouraging to see Energizer narrowly top analysts' revenue expectations this quarter. We were also happy its EPS narrowly outperformed Wall Street's estimates. While next quarter's EPS outlook was below expectations, full year EPS guidance was in line., Overall, the results were mixed but fine, with no major surprises. The stock is flat after reporting and currently trades at $31.07 per share.

Energizer may not have had the best quarter, but does that create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.