Envestnet (ENV) Benefits From a Strategic Business Model

Envestnet, Inc. ENV has strong asset-based and subscription-based recurring revenue generation capacity. The company continues to focus on technology development to improve operational efficiency and increase market competitiveness.

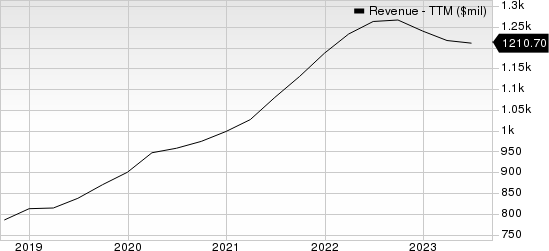

Envestnet reported mixed second-quarter 2023 results with earnings beating the Zacks Consensus Estimate but revenues missing the same. Adjusted earnings (excluding 85 cents from non-recurring items) came in at 46 cents per share, matching the consensus estimate but decreasing 6.1% from the year-ago figure. Total revenues of $312.43 million missed the consensus estimate by 0.85%. Revenues decreased 2% on a year-over-year basis.

Factors in Favor

In recent years, Envestnet has demonstrated a robust capacity for generating recurring revenues, primarily driven by its asset-based and subscription-based business models. The company serves financial services clients through a business-to-business-to-consumer approach, thus enabling these clients to offer Envestnet's platform-based solutions to their end users. Moreover, on a business-to-business level, Envestnet provides an open platform to customers and third-party developers through an open API framework. Envestnet's recurring revenues have displayed consistent growth, with a 4.5% year-over-year increase in 2022, following impressive gains of 20.2% in 2021 and 10.2% in 2020.

Envestnet, Inc Revenue (TTM)

Envestnet, Inc revenue-ttm | Envestnet, Inc Quote

Envestnet is actively prioritizing technology development to enhance efficiency, competitiveness, compliance with regulations, and responsiveness to client demands. The company’s current technology infrastructure employs a three-tier architecture, encompassing a web-based user interface, an application tier housing core business logic, and a SQL Server database, which it believes offers substantial scalability potential.

Several market trends are offering significant opportunities for Envestnet's technology-driven solutions. Investment advice is increasingly integral to financial planning, and clients are seeking personalized wealth management services. The adoption of technology is set to rise, driven by the need for cost-effective, guided interactions with clients.

Key Risks

Envestnet's current ratio at the end of second-quarter 2023 was pegged at 0.73, lower than the previous quarter's current ratio of 0.75 and the prior-year quarter's current ratio of 0.77. Decreasing current ratio is not desirable as it indicates that the company may have problems meeting its short-term debt obligations.

ENV currently carries a Zacks Rank #3(Hold). Here are some better-ranked stocks from the Business Service sector which may be considered by investors:

Verisk Analytics VRSK has beaten the Zacks Consensus Estimate in three of the four previous quarters and matched on one instance, the average surprise being 9.9% The consensus mark for 2023 revenues is pegged at $2.66 billion, which reflects decrease of 8.2% from the year-ago figure. Earnings are pegged at $5.71 per share for 2023, which is 14% above the year-ago figure. VRSK currently holds a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Automatic Data ADP currently has a Zacks Rank of 2. The company beat the Zacks Consensus Estimate in all the trailing four quarters, the average surprise being 3.1%. The consensus estimate for fiscal 2023 revenues and earnings implies growth of 6.3% and 11.1%, respectively.

Broadridge BR currently carries a Zacks Rank of 2. It beat the Zacks Consensus Estimate in two of the trailing four quarters, missed once and matched on one instance, the average surprise being 0.5%. The Zacks Consensus Estimate for fiscal 2024 revenues and earnings calls for a rise of 7.2% and 8.8%, respectively.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Broadridge Financial Solutions, Inc. (BR) : Free Stock Analysis Report

Automatic Data Processing, Inc. (ADP) : Free Stock Analysis Report

Envestnet, Inc (ENV) : Free Stock Analysis Report

Verisk Analytics, Inc. (VRSK) : Free Stock Analysis Report