If EPS Growth Is Important To You, Rave Restaurant Group (NASDAQ:RAVE) Presents An Opportunity

It's common for many investors, especially those who are inexperienced, to buy shares in companies with a good story even if these companies are loss-making. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.' Loss making companies can act like a sponge for capital - so investors should be cautious that they're not throwing good money after bad.

If this kind of company isn't your style, you like companies that generate revenue, and even earn profits, then you may well be interested in Rave Restaurant Group (NASDAQ:RAVE). Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide Rave Restaurant Group with the means to add long-term value to shareholders.

View our latest analysis for Rave Restaurant Group

Rave Restaurant Group's Improving Profits

In business, profits are a key measure of success; and share prices tend to reflect earnings per share (EPS) performance. So a growing EPS generally brings attention to a company in the eyes of prospective investors. It's an outstanding feat for Rave Restaurant Group to have grown EPS from US$0.12 to US$0.55 in just one year. While it's difficult to sustain growth at that level, it bodes well for the company's outlook for the future.

It's often helpful to take a look at earnings before interest and tax (EBIT) margins, as well as revenue growth, to get another take on the quality of the company's growth. On the one hand, Rave Restaurant Group's EBIT margins fell over the last year, but on the other hand, revenue grew. So if EBIT margins can stabilize, this top-line growth should pay off for shareholders.

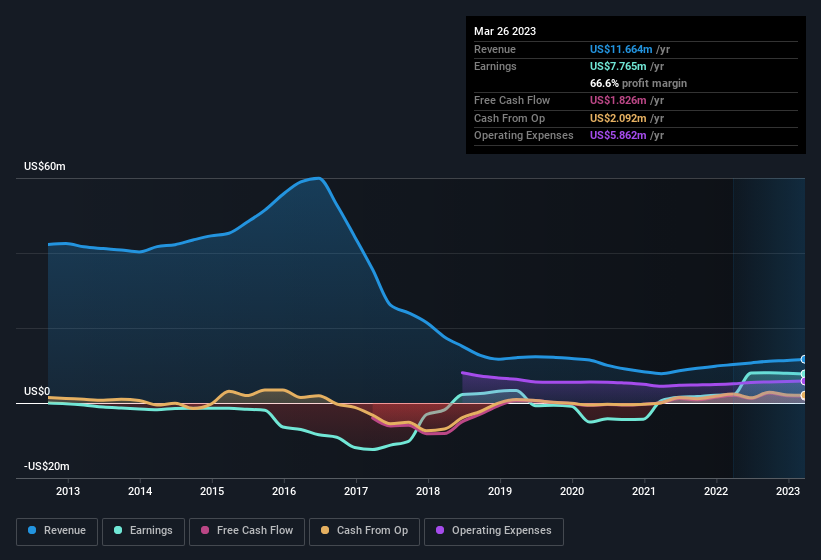

The chart below shows how the company's bottom and top lines have progressed over time. To see the actual numbers, click on the chart.

Rave Restaurant Group isn't a huge company, given its market capitalisation of US$29m. That makes it extra important to check on its balance sheet strength.

Are Rave Restaurant Group Insiders Aligned With All Shareholders?

It's said that there's no smoke without fire. For investors, insider buying is often the smoke that indicates which stocks could set the market alight. Because often, the purchase of stock is a sign that the buyer views it as undervalued. However, small purchases are not always indicative of conviction, and insiders don't always get it right.

It's nice to see that there have been no reports of any insiders selling shares in Rave Restaurant Group in the previous 12 months. With that in mind, it's heartening that Brandon Solano, the President of the company, paid US$39k for shares at around US$1.57 each. Purchases like this can help the investors understand the views of the management team; in which case they see some potential in Rave Restaurant Group.

Should You Add Rave Restaurant Group To Your Watchlist?

Rave Restaurant Group's earnings have taken off in quite an impressive fashion. Growth-minded people will be intrigued by the incredible movement in EPS growth. And indeed, it could be a sign that the business is at an inflection point. If that's the case, you may regret neglecting to put Rave Restaurant Group on your watchlist. You should always think about risks though. Case in point, we've spotted 2 warning signs for Rave Restaurant Group you should be aware of.

There are plenty of other companies that have insiders buying up shares. So if you like the sound of Rave Restaurant Group, you'll probably love this free list of growing companies that insiders are buying.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.