If EPS Growth Is Important To You, Twin Disc (NASDAQ:TWIN) Presents An Opportunity

For beginners, it can seem like a good idea (and an exciting prospect) to buy a company that tells a good story to investors, even if it currently lacks a track record of revenue and profit. Sometimes these stories can cloud the minds of investors, leading them to invest with their emotions rather than on the merit of good company fundamentals. Loss-making companies are always racing against time to reach financial sustainability, so investors in these companies may be taking on more risk than they should.

So if this idea of high risk and high reward doesn't suit, you might be more interested in profitable, growing companies, like Twin Disc (NASDAQ:TWIN). While this doesn't necessarily speak to whether it's undervalued, the profitability of the business is enough to warrant some appreciation - especially if its growing.

See our latest analysis for Twin Disc

Twin Disc's Improving Profits

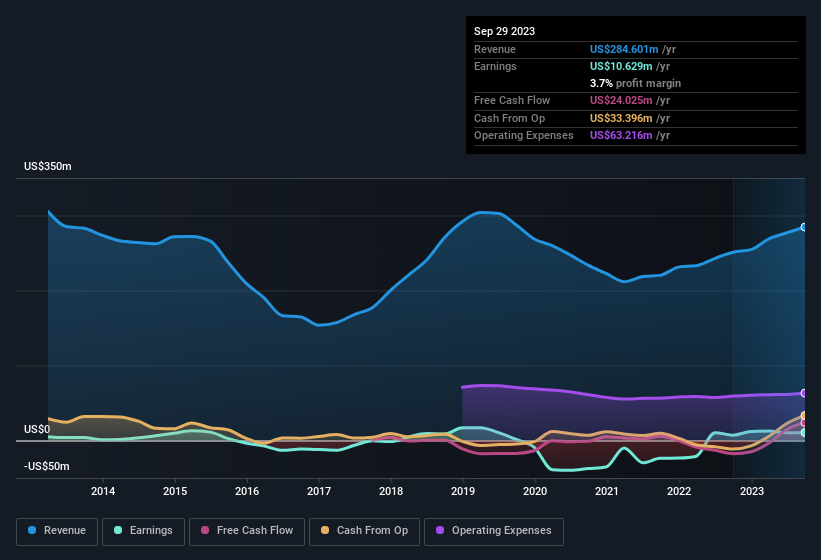

Over the last three years, Twin Disc has grown earnings per share (EPS) at as impressive rate from a relatively low point, resulting in a three year percentage growth rate that isn't particularly indicative of expected future performance. Thus, it makes sense to focus on more recent growth rates, instead. Twin Disc's EPS skyrocketed from US$0.54 to US$0.76, in just one year; a result that's bound to bring a smile to shareholders. That's a fantastic gain of 42%.

Careful consideration of revenue growth and earnings before interest and taxation (EBIT) margins can help inform a view on the sustainability of the recent profit growth. While we note Twin Disc achieved similar EBIT margins to last year, revenue grew by a solid 13% to US$285m. That's a real positive.

In the chart below, you can see how the company has grown earnings and revenue, over time. For finer detail, click on the image.

Twin Disc isn't a huge company, given its market capitalisation of US$224m. That makes it extra important to check on its balance sheet strength.

Are Twin Disc Insiders Aligned With All Shareholders?

It should give investors a sense of security owning shares in a company if insiders also own shares, creating a close alignment their interests. So it is good to see that Twin Disc insiders have a significant amount of capital invested in the stock. As a matter of fact, their holding is valued at US$48m. This considerable investment should help drive long-term value in the business. As a percentage, this totals to 21% of the shares on issue for the business, an appreciable amount considering the market cap.

Does Twin Disc Deserve A Spot On Your Watchlist?

For growth investors, Twin Disc's raw rate of earnings growth is a beacon in the night. Further, the high level of insider ownership is impressive and suggests that the management appreciates the EPS growth and has faith in Twin Disc's continuing strength. The growth and insider confidence is looked upon well and so it's worthwhile to investigate further with a view to discern the stock's true value. Now, you could try to make up your mind on Twin Disc by focusing on just these factors, or you could also consider how its price-to-earnings ratio compares to other companies in its industry.

Although Twin Disc certainly looks good, it may appeal to more investors if insiders were buying up shares. If you like to see companies with insider buying, then check out this handpicked selection of companies that not only boast of strong growth but have also seen recent insider buying..

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.