With EPS Growth And More, Digitalbox (LON:DBOX) Makes An Interesting Case

The excitement of investing in a company that can reverse its fortunes is a big draw for some speculators, so even companies that have no revenue, no profit, and a record of falling short, can manage to find investors. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.' Loss making companies can act like a sponge for capital - so investors should be cautious that they're not throwing good money after bad.

Despite being in the age of tech-stock blue-sky investing, many investors still adopt a more traditional strategy; buying shares in profitable companies like Digitalbox (LON:DBOX). While profit isn't the sole metric that should be considered when investing, it's worth recognising businesses that can consistently produce it.

Check out our latest analysis for Digitalbox

How Fast Is Digitalbox Growing Its Earnings Per Share?

Over the last three years, Digitalbox has grown earnings per share (EPS) at as impressive rate from a relatively low point, resulting in a three year percentage growth rate that isn't particularly indicative of expected future performance. As a result, we'll zoom in on growth over the last year, instead. In impressive fashion, Digitalbox's EPS grew from UK£0.0034 to UK£0.0068, over the previous 12 months. It's not often a company can achieve year-on-year growth of 100%.

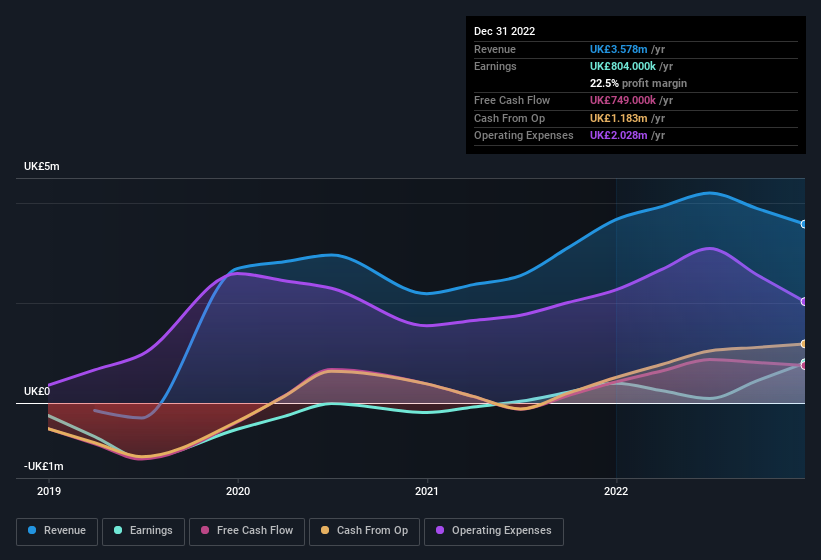

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. We note that while EBIT margins have improved from 17% to 23%, the company has actually reported a fall in revenue by 2.4%. While not disastrous, these figures could be better.

The chart below shows how the company's bottom and top lines have progressed over time. Click on the chart to see the exact numbers.

Digitalbox isn't a huge company, given its market capitalisation of UK£7.8m. That makes it extra important to check on its balance sheet strength.

Are Digitalbox Insiders Aligned With All Shareholders?

Insider interest in a company always sparks a bit of intrigue and many investors are on the lookout for companies where insiders are putting their money where their mouth is. That's because insider buying often indicates that those closest to the company have confidence that the share price will perform well. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

Digitalbox top brass are certainly in sync, not having sold any shares, over the last year. But the bigger deal is that the CFO & Director, David Joseph, paid UK£44k to buy shares at an average price of UK£0.08. It seems at least one insider has seen potential in the company's future - and they're willing to put money on the line.

Is Digitalbox Worth Keeping An Eye On?

Digitalbox's earnings per share growth have been climbing higher at an appreciable rate. Growth investors should find it difficult to look past that strong EPS move. And in fact, it could well signal a fundamental shift in the business economics. If this is the case, then keeping a watch over Digitalbox could be in your best interest. You should always think about risks though. Case in point, we've spotted 3 warning signs for Digitalbox you should be aware of, and 1 of them is potentially serious.

There are plenty of other companies that have insiders buying up shares. So if you like the sound of Digitalbox, you'll probably love this free list of growing companies that insiders are buying.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here