With EPS Growth And More, A.G. BARR (LON:BAG) Makes An Interesting Case

Investors are often guided by the idea of discovering 'the next big thing', even if that means buying 'story stocks' without any revenue, let alone profit. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.' Loss making companies can act like a sponge for capital - so investors should be cautious that they're not throwing good money after bad.

Despite being in the age of tech-stock blue-sky investing, many investors still adopt a more traditional strategy; buying shares in profitable companies like A.G. BARR (LON:BAG). Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide A.G. BARR with the means to add long-term value to shareholders.

See our latest analysis for A.G. BARR

How Quickly Is A.G. BARR Increasing Earnings Per Share?

If you believe that markets are even vaguely efficient, then over the long term you'd expect a company's share price to follow its earnings per share (EPS) outcomes. That means EPS growth is considered a real positive by most successful long-term investors. Impressively, A.G. BARR has grown EPS by 26% per year, compound, in the last three years. As a general rule, we'd say that if a company can keep up that sort of growth, shareholders will be beaming.

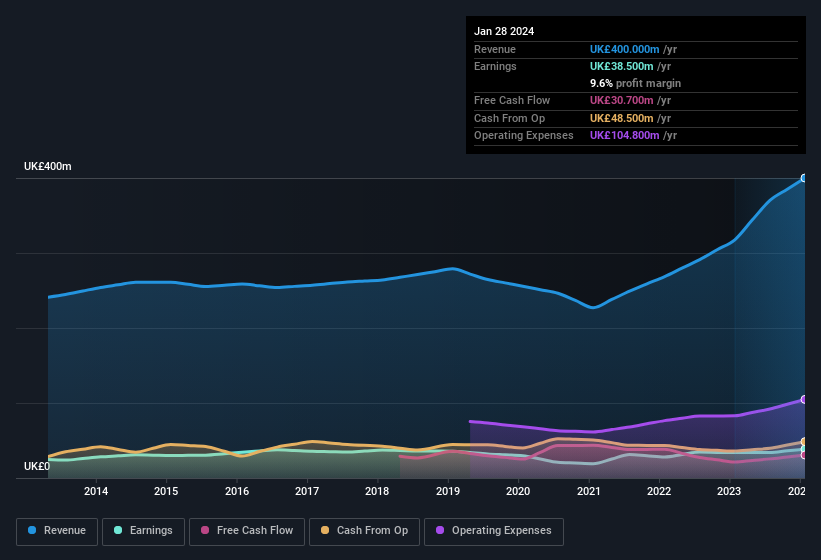

Top-line growth is a great indicator that growth is sustainable, and combined with a high earnings before interest and taxation (EBIT) margin, it's a great way for a company to maintain a competitive advantage in the market. While we note A.G. BARR achieved similar EBIT margins to last year, revenue grew by a solid 26% to UK£400m. That's a real positive.

The chart below shows how the company's bottom and top lines have progressed over time. To see the actual numbers, click on the chart.

In investing, as in life, the future matters more than the past. So why not check out this free interactive visualization of A.G. BARR's forecast profits?

Are A.G. BARR Insiders Aligned With All Shareholders?

Insider interest in a company always sparks a bit of intrigue and many investors are on the lookout for companies where insiders are putting their money where their mouth is. That's because insider buying often indicates that those closest to the company have confidence that the share price will perform well. Of course, we can never be sure what insiders are thinking, we can only judge their actions.

A great takeaway for shareholders is that company insiders within A.G. BARR have collectively spent UK£10k acquiring shares in the company. This might not be a huge sum, but it's well worth noting anyway, given the complete lack of selling.

On top of the insider buying, it's good to see that A.G. BARR insiders have a valuable investment in the business. Notably, they have an enviable stake in the company, worth UK£102m. This totals to 16% of shares in the company. Enough to lead management's decision making process down a path that brings the most benefit to shareholders. Looking very optimistic for investors.

Is A.G. BARR Worth Keeping An Eye On?

You can't deny that A.G. BARR has grown its earnings per share at a very impressive rate. That's attractive. Furthermore, company insiders have been adding to their significant stake in the company. Astute investors will want to keep this stock on watch. Don't forget that there may still be risks. For instance, we've identified 1 warning sign for A.G. BARR that you should be aware of.

There are plenty of other companies that have insiders buying up shares. So if you like the sound of A.G. BARR, you'll probably love this curated collection of companies in GB that have witnessed growth alongside insider buying in the last three months.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.