With EPS Growth And More, TerraCom (ASX:TER) Makes An Interesting Case

Investors are often guided by the idea of discovering 'the next big thing', even if that means buying 'story stocks' without any revenue, let alone profit. Sometimes these stories can cloud the minds of investors, leading them to invest with their emotions rather than on the merit of good company fundamentals. While a well funded company may sustain losses for years, it will need to generate a profit eventually, or else investors will move on and the company will wither away.

In contrast to all that, many investors prefer to focus on companies like TerraCom (ASX:TER), which has not only revenues, but also profits. While profit isn't the sole metric that should be considered when investing, it's worth recognising businesses that can consistently produce it.

View our latest analysis for TerraCom

TerraCom's Improving Profits

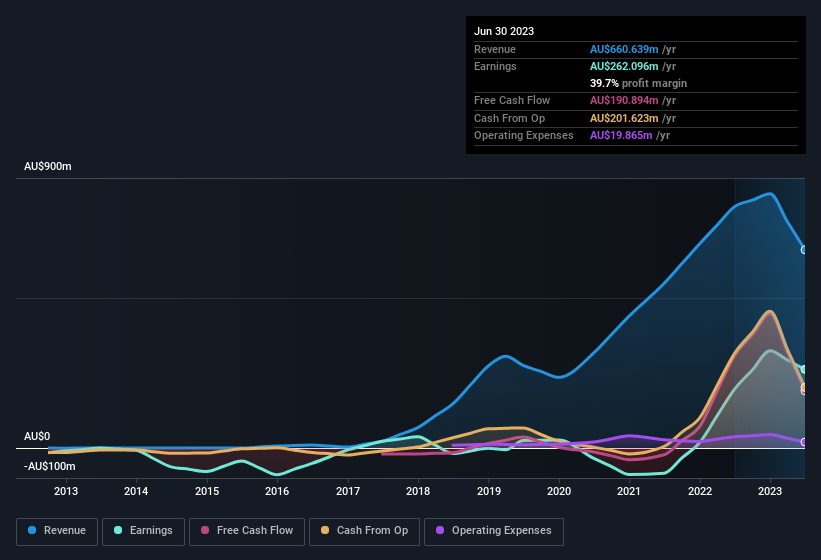

TerraCom has undergone a massive growth in earnings per share over the last three years. So much so that this three year growth rate wouldn't be a fair assessment of the company's future. Thus, it makes sense to focus on more recent growth rates, instead. To the delight of shareholders, TerraCom's EPS soared from AU$0.26 to AU$0.33, over the last year. That's a impressive gain of 26%.

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. TerraCom's EBIT margins have actually improved by 4.6 percentage points in the last year, to reach 48%, but, on the flip side, revenue was down 18%. While not disastrous, these figures could be better.

In the chart below, you can see how the company has grown earnings and revenue, over time. For finer detail, click on the image.

TerraCom isn't a huge company, given its market capitalisation of AU$404m. That makes it extra important to check on its balance sheet strength.

Are TerraCom Insiders Aligned With All Shareholders?

Insider interest in a company always sparks a bit of intrigue and many investors are on the lookout for companies where insiders are putting their money where their mouth is. This view is based on the possibility that stock purchases signal bullishness on behalf of the buyer. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

We note that TerraCom insiders spent AU$262k on stock, over the last year; in contrast, we didn't see any selling. That's nice to see, because it suggests insiders are optimistic. It is also worth noting that it was Non-Executive Director Glen Lewis who made the biggest single purchase, worth AU$103k, paying AU$1.03 per share.

On top of the insider buying, it's good to see that TerraCom insiders have a valuable investment in the business. As a matter of fact, their holding is valued at AU$22m. That's a lot of money, and no small incentive to work hard. That amounts to 5.4% of the company, demonstrating a degree of high-level alignment with shareholders.

Is TerraCom Worth Keeping An Eye On?

You can't deny that TerraCom has grown its earnings per share at a very impressive rate. That's attractive. Furthermore, company insiders have been adding to their significant stake in the company. So it's fair to say that this stock may well deserve a spot on your watchlist. We should say that we've discovered 2 warning signs for TerraCom (1 doesn't sit too well with us!) that you should be aware of before investing here.

Keen growth investors love to see insider buying. Thankfully, TerraCom isn't the only one. You can see a a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.