If You Like EPS Growth Then Check Out Austco Healthcare (ASX:AHC) Before It's Too Late

Some have more dollars than sense, they say, so even companies that have no revenue, no profit, and a record of falling short, can easily find investors. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.'

In the age of tech-stock blue-sky investing, my choice may seem old fashioned; I still prefer profitable companies like Austco Healthcare (ASX:AHC). Now, I'm not saying that the stock is necessarily undervalued today; but I can't shake an appreciation for the profitability of the business itself. Conversely, a loss-making company is yet to prove itself with profit, and eventually the sweet milk of external capital may run sour.

Check out our latest analysis for Austco Healthcare

How Fast Is Austco Healthcare Growing?

The market is a voting machine in the short term, but a weighing machine in the long term, so share price follows earnings per share (EPS) eventually. Therefore, there are plenty of investors who like to buy shares in companies that are growing EPS. Impressively, Austco Healthcare has grown EPS by 33% per year, compound, in the last three years. If the company can sustain that sort of growth, we'd expect shareholders to come away winners.

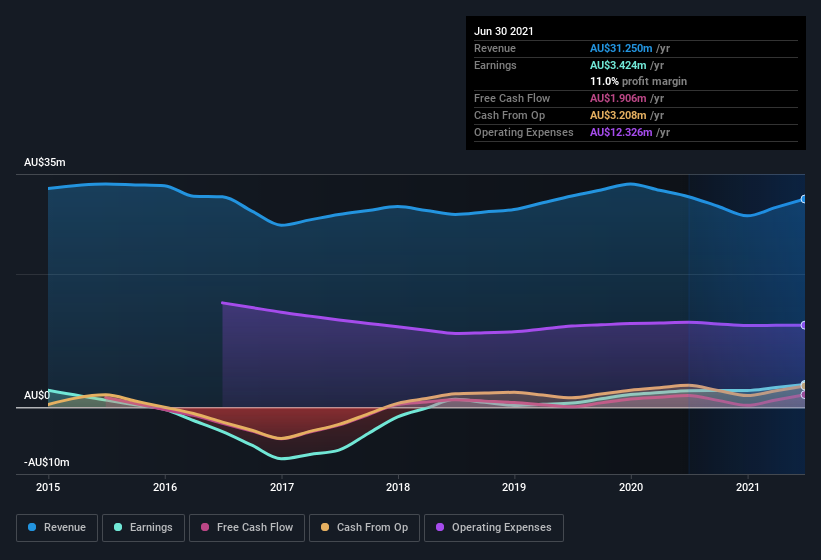

I like to take a look at earnings before interest and (EBIT) tax margins, as well as revenue growth, to get another take on the quality of the company's growth. This approach makes Austco Healthcare look pretty good, on balance; although revenue is flattish, EBIT margins improved from 4.1% to 6.6% in the last year. That's something to smile about.

In the chart below, you can see how the company has grown earnings, and revenue, over time. To see the actual numbers, click on the chart.

Since Austco Healthcare is no giant, with a market capitalization of AU$37m, so you should definitely check its cash and debt before getting too excited about its prospects.

Are Austco Healthcare Insiders Aligned With All Shareholders?

Like that fresh smell in the air when the rains are coming, insider buying fills me with optimistic anticipation. Because oftentimes, the purchase of stock is a sign that the buyer views it as undervalued. However, small purchases are not always indicative of conviction, and insiders don't always get it right.

One positive for Austco Healthcare, is that company insiders paid AU$70k for shares in the last year. While this isn't much, we also note an absence of sales. Zooming in, we can see that the biggest insider purchase was by Independent Non-Executive Director J. Burns for AU$40k worth of shares, at about AU$0.15 per share.

And the insider buying isn't the only sign of alignment between shareholders and the board, since Austco Healthcare insiders own more than a third of the company. In fact, they own 47% of the shares, making insiders a very influential shareholder group. I'm always comforted by solid insider ownership like this, as it implies that those running the business are genuinely motivated to create shareholder value. Of course, Austco Healthcare is a very small company, with a market cap of only AU$37m. That means insiders only have AU$17m worth of shares, despite the large proportional holding. That's not a huge stake in absolute terms, but it should help keep insiders aligned with other shareholders.

Is Austco Healthcare Worth Keeping An Eye On?

Given my belief that share price follows earnings per share you can easily imagine how I feel about Austco Healthcare's strong EPS growth. Not only that, but we can see that insiders both own a lot of, and are buying more, shares in the company. So I do think this is one stock worth watching. Don't forget that there may still be risks. For instance, we've identified 2 warning signs for Austco Healthcare that you should be aware of.

As a growth investor I do like to see insider buying. But Austco Healthcare isn't the only one. You can see a a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.