Estée Lauder (NYSE:EL) Surprises With Q2 Sales, Stock Jumps 10.6%

Beauty products company Estée Lauder (NYSE:EL) beat analysts' expectations in Q2 FY2024, with revenue down 7.4% year on year to $4.28 billion. It made a non-GAAP profit of $0.88 per share, down from its profit of $1.54 per share in the same quarter last year.

Is now the time to buy Estée Lauder? Find out by accessing our full research report, it's free.

Estée Lauder (EL) Q2 FY2024 Highlights:

Revenue: $4.28 billion vs analyst estimates of $4.24 billion (0.9% beat)

EPS (non-GAAP): $0.88 vs analyst estimates of $0.56 (57.5% beat)

EPS (non-GAAP) Guidance for Q3 2024 is $0.41 at the midpoint, below analyst estimates of $0.83

Free Cash Flow of $1.11 billion is up from -$703 million in the previous quarter

Gross Margin (GAAP): 73%, in line with the same quarter last year

Organic Revenue was down 7.9% year on year

Market Capitalization: $47.99 billion

Fabrizio Freda, President and Chief Executive Officer said, “For the second quarter of fiscal 2024, we delivered our organic sales outlook and exceeded expectations for profitability. The Ordinary and La Mer in Skin Care, Clinique in Makeup, and Le Labo and Jo Malone London in Fragrance performed strongly. Many developed and emerging markets around the world continued to grow organically and at retail. While mainland China and Asia travel retail declined, our retail sales trended ahead of organic sales, and these businesses are poised to return to organic sales growth in the second half.

Named after its founder, who was an entrepreneurial woman from New York with a passion for skincare, Estée Lauder (NYSE:EL) is a one-stop beauty shop with products in skincare, fragrance, makeup, sun protection, and men’s grooming.

Personal Care

Personal care products include lotions, fragrances, shampoos, cosmetics, and nutritional supplements, among others. While these products may seem more discretionary than food, consumers tend to maintain or even boost their spending on the category during tough times. This phenomenon is known as "the lipstick effect" by economists, which states that consumers still want some semblance of affordable luxuries like beauty and wellness when the economy is sputtering. As with other consumer staples categories, personal care brands must exude quality and be priced optimally given the crowded competitive landscape. Consumer tastes are constantly changing, and personal care companies are currently responding to the public’s increased desire for ethically produced goods by featuring natural ingredients in their products.

Sales Growth

Estée Lauder is one of the larger consumer staples companies and benefits from a well-known brand, giving it customer mindshare and influence over purchasing decisions.

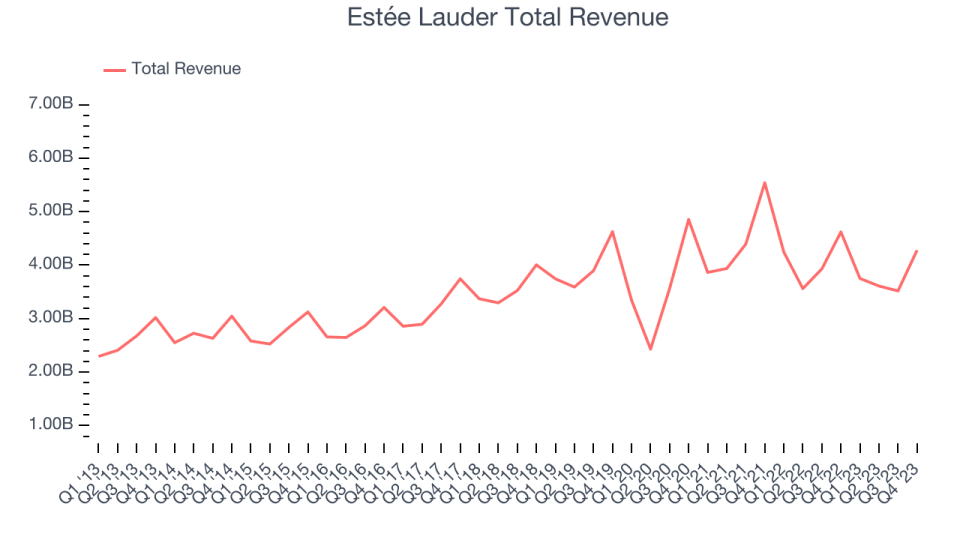

As you can see below, the company's annualized revenue growth rate of 2.2% over the last three years was weak for a consumer staples business.

This quarter, Estée Lauder reported a rather uninspiring 7.4% year-on-year revenue decline to $4.28 billion in revenue, in line with Wall Street's estimates. Looking ahead, Wall Street expects sales to grow 8.2% over the next 12 months, an acceleration from this quarter.

Today’s young investors likely haven’t read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Key Takeaways from Estée Lauder's Q2 Results

We were impressed by how significantly Estée Lauder blew past analysts' EPS expectations this quarter. We were also excited its operating margin outperformed Wall Street's estimates. On the other hand, its earnings forecast for next quarter missed analysts' expectations and its full-year earnings guidance missed Wall Street's estimates. The company did provide some silver lining, though, projecting a "return to double-digit organic net sales growth in the second half of fiscal 2024." Overall, this quarter's results still seemed fairly positive given that outlook for a topline recovery. The stock is up 10.6% after reporting and currently trades at $148.5 per share.

So should you invest in Estée Lauder right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.