ETF Scorecard: January 11 Edition

To help investors keep up with the markets, we present our ETF Scorecard. The Scorecard takes a step back and looks at how various asset classes across the globe are performing. The weekly performance is from last Friday’s open to this week’s Thursday close.

Despite worries about trade wars and an economic slowdown across the board, the U.S. job market is making great strides. In the last month of 2018, the U.S. economy added 312,000 jobs, nearly double the figure expected by analysts. The showing for November itself was revised up by 21,000 to 176,000. At the same time, hourly earnings increased by 0.4% in December on average compared with 0.3% expected by pundits. Such a rise in hourly earnings has not been seen since September. Meanwhile, the unemployment rate jumped from 3.7% to 3.9%, a sign the labor market is expanding and more people are joining the labor force. Amid market turbulence, Federal Reserve Chair Jerome Powell attempted to ease market concerns, saying he was aware of the risks stemmed from raising interest rates too quickly and was listening carefully to what the markets had to say. Stocks posted a strong rally this week. On Thursday, Powell spoke again, saying the Fed can be patient on monetary policy given the stable inflation. The Federal Reserve minutes revealed that policymakers have become more dovish, finally acknowledging the risks related to a slowdown in China, trade wars and political turbulence. U.S. non-manufacturing purchasing managers’ index (PMI) dropped dramatically in December, from 60.7 to 57.6, signaling a deteriorating sentiment. U.S. crude oil inventories declined by 1.7 million barrels in the week ended January 4, following two straight weeks of flat gains. Stockpiles have not seen a weekly rise since the end of November when they ended a ten-week streak of gains. U.K. economic output expanded 0.2% in November, beating expectations of 0.1%. The upbeat figure comes as the country still struggles to reach a Brexit solution, with the government and the Parliament at odds. An increasingly likely scenario is to push back the March 29 exit date to avoid chaos.

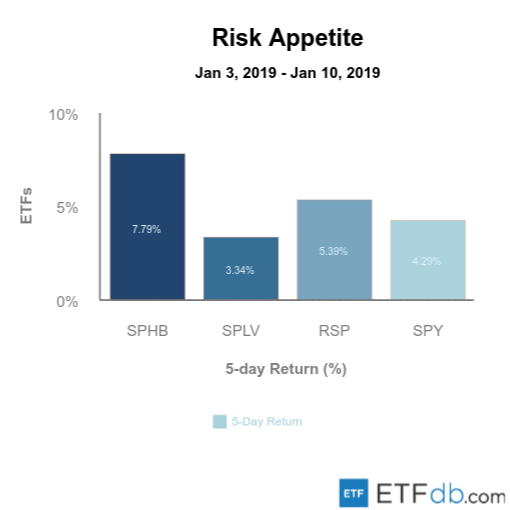

Risk Appetite Review

The markets rallied this week, cheering the Federal Reserve’s increasingly dovish stance. Risk equities (SPHB B-) were the biggest risers this week, advancing as much as 7.8%. Low volatility (SPLV A), meanwhile, fell 3.34%, representing the worst performance. The broad market (SPY A) advanced 4.29%.

Sign up for ETFdb.com Pro and get access to real-time ratings on over 1,900 U.S.-listed ETFs.

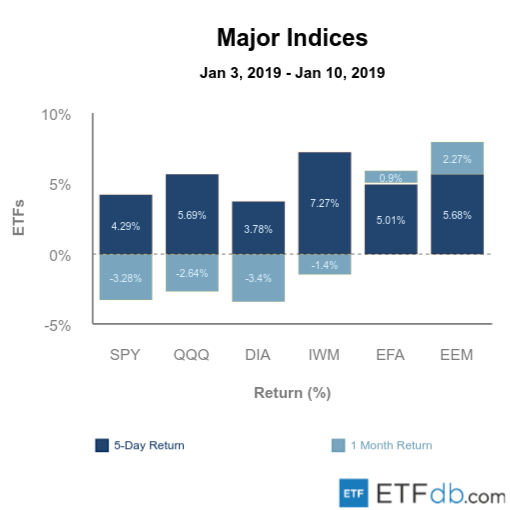

Major Index Review

Major indexes were all up. Small-cap stocks (IWM B+) powered ahead this week, surging 7.3%, thanks to the Federal Reserve’s dovish comments. Dow Jones (DIA A-), meanwhile, posted measured gains of 3.8%, making it the worst performer both for the week and the rolling month. (DIA A-) is down 3.4% for the past 30 days. Emerging markets (EEM A-) recorded the strongest monthly gains, rising 2.27%.

To see how these indices performed over the past year, check out ETF Scorecard: January 4 Edition

Sectors Review

The telecom sector (XTL A) was the biggest beneficiary of this broad market rally, climbing nearly 8% over the past five days. Consumer staples (XLP A) are the poorest performers both for the week and the rolling month, up 2.16% and down 6.57%, respectively. The retail sector (XLY A) managed to post the smallest losses for the past 30 days, down 0.49%.

Use our Head-to-Head Comparison tool to compare two ETFs such as (XTL A) and (XLP A) on a variety of criteria such as performance, AUM, trading volume and expenses.

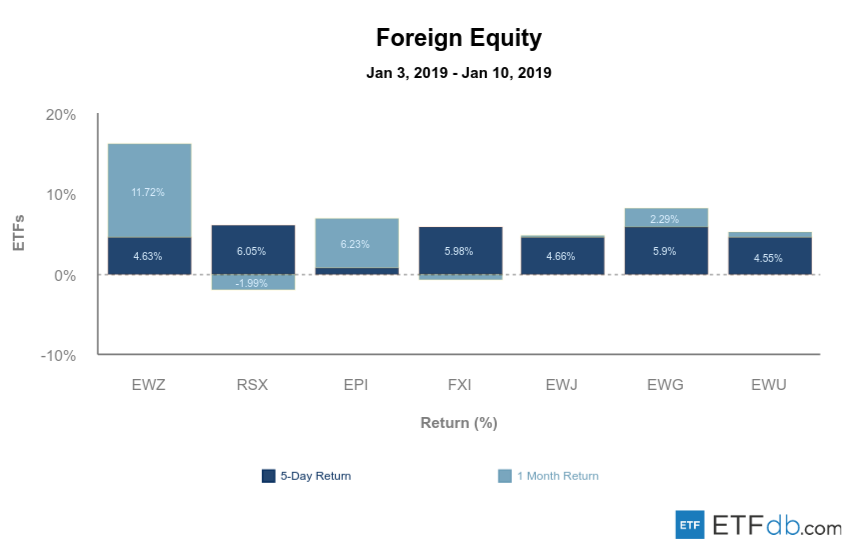

Foreign Equity Review

Russia (RSX B+) jumped more than 6% over the past week, helped in part by a strong rally in oil prices. Still, the largest country in the world remains the worst performer for the rolling month, down nearly 2%. Brazil (EWZ B+), meanwhile, is by far the strongest performer for the month with a gain of 11.7%. India (EPI B+) is up just 0.87% for the week, although it is among the best performers for the month.

To find out more about ETFs exposed to particular countries, check out our ETF Country Exposure tool. Select a particular country from a world map and get a list of all ETFs tracking your pick.

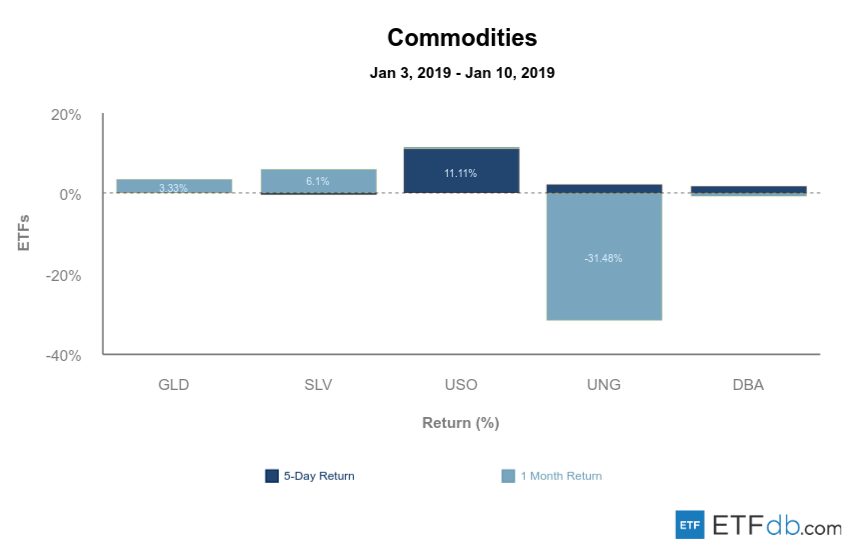

Commodities Review

Optimism about global trade and supply cuts by OPEC prompted an 11% rise in oil prices (USO A), helping the commodity to be slightly in the black for the rolling month. After weeks of gains, silver (SLV C+) is now the worst performer and among the few losers, down 0.61%. However, the precious commodity remains the best performer for the rolling month, up 6.1%. Natural gas (UNG B-) recovered some of the steep losses recorded in previous weeks, but it is still down 31% for the rolling month.

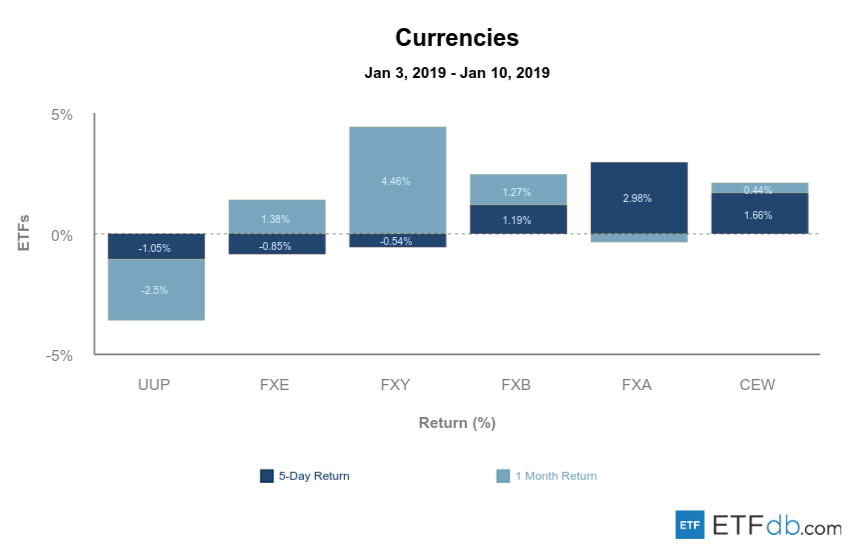

Currency Review

The U.S. dollar (UUP A) has been the chief loser both for the week and the rolling month, losing 1% and 2.5%, respectively. The dovish Federal Reserve stance prompted a sell-off in the greenback. The Australian dollar (FXA A-), one of the most volatile currencies from the pack, was the best performer for the past five days, advancing nearly 3%. Meanwhile, the Japanese yen (FXY C+) is the best monthly performer with a gain of 4.46%.

For more ETF news and analysis, subscribe to our free newsletter.