ETF Scorecard: March 15 Edition

To help investors keep up with the markets, we present our ETF Scorecard. The Scorecard takes a step back and looks at how various asset classes across the globe are performing. The weekly performance is from last Friday’s open to this week’s Thursday close.

A deal between the U.S. and China to end the trade war may not be reached at least until April, as the sides are still negotiating. U.S. President Donald Trump indicated that he is in no rush to sign a trade agreement, adding that he wants to take his time to negotiate a good deal. The U.K. Parliament rejected a second Brexit deal proposed by Prime Minister Theresa May, risking to throw the country into chaos. The most likely scenario now, however, is a delay of the exit day. A vote in the British Parliament on such a motion passed successfully. The U.S. jobs report for February disappointed thoroughly likely due to unusually cold weather in many parts of the U.S. Just 20,000 jobs were added during the month versus 180,000 expected, the worst figure since October 2017. To be sure, the weak report comes after two blockbuster reports in which the U.S. economy added more than 650,000 jobs combined. The U.S. unemployment rate declined from 4% to 3.8%, while wages grew by 0.4%. Year-over-year, wages are up 3.4%, reaching a cycle high. U.S. building permits advanced from 1.33 million to 1.35 million, hitting a one-year high. Analysts had expected 1.29 million permits to be released. U.S. retail sales rose 0.2% in February month-over-month, following an abrupt drop of 1.6% in the prior month. Core retail sales were even stronger, rising 0.9%. U.K. GDP unexpectedly rose 0.5% in January despite uncertainty surrounding Brexit. Analysts had predicted an advance of 0.2%. U.K. manufacturing production, meanwhile, surged 0.8%, marking the first advance in four months. U.S. CPI rose for the first time in four months, resulting in an annual gain of 1.5%, below the Federal Reserve’s target of 2%.

For more ETF news and analysis, subscribe to our free newsletter.

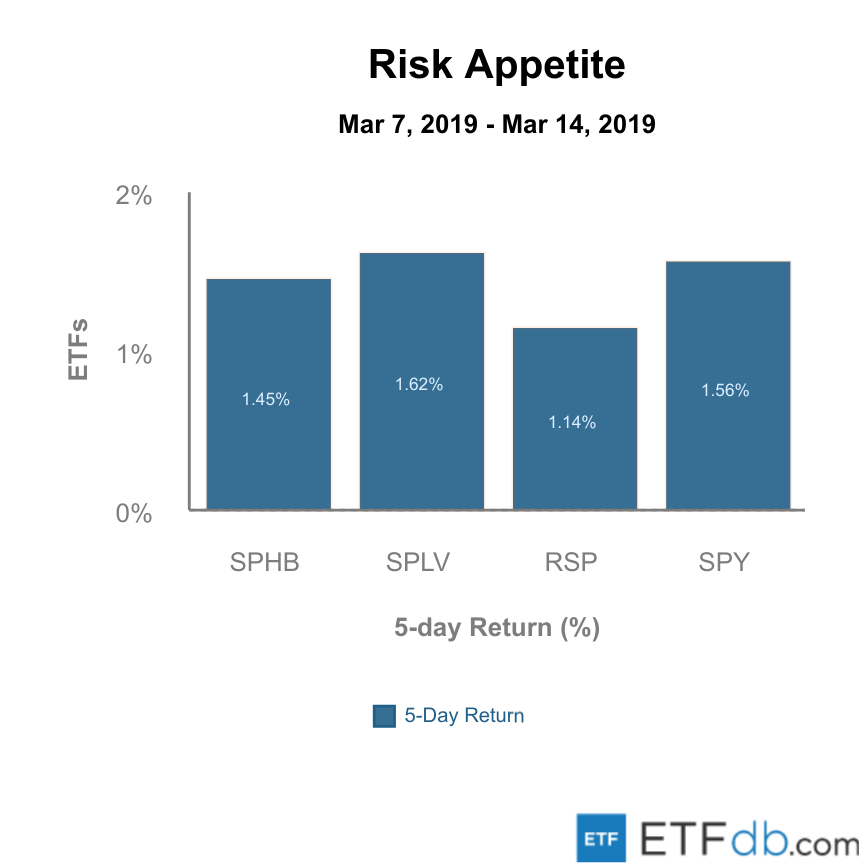

Risk Appetite Review

Markets were up this week. Low volatility ETF (SPLV A) was the best performer, advancing as much as 1.62% for the week. The broad market ETF (SPY A) was the second-best performer with a rise of 1.56%.

Sign up for ETFdb.com Pro and get access to real-time ratings on over 1,900 U.S. listed ETFs.

Major Index Review

With the exception of emerging markets, all indexes were up. Technology stocks (QQQ A-) were the biggest gainers for the week, advancing 2.09%, largely on the back of gains registered by the FANG stocks. A long-awaited initial public offering of Uber, the hottest private company in the world, boosted sentiment. Emerging markets (EEM A-) declined slightly for the week, as investors were worried about the lack of progress on a trade deal between the U.S. and China.

To see how these indices performed over the past year, check out ETF Scorecard: March 8 Edition

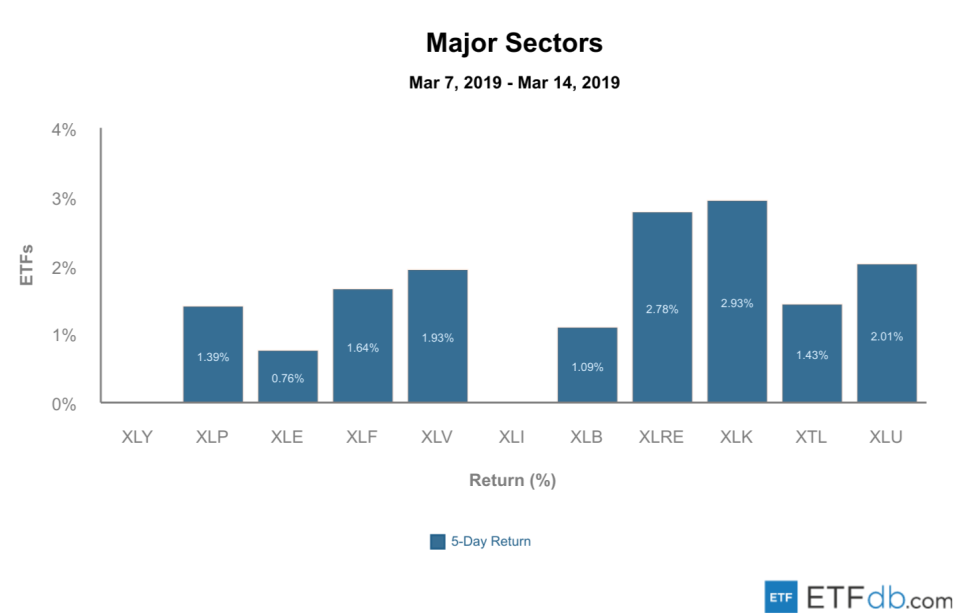

Sectors Review

Sectors were mostly up or remained flat. The technology ETF (XLK A) was the best performer from the pack, with a jump of nearly 3%. Meanwhile, the industrial (XLI A) and consumer discretionary (XLY A) ETFs shared the position of the worst performer with flat gains.

Use our head to head comparison tool to compare two ETFs such as (XLI A) and (XLY A) on a variety of criteria such as performance, AUM, trading volume and expenses.

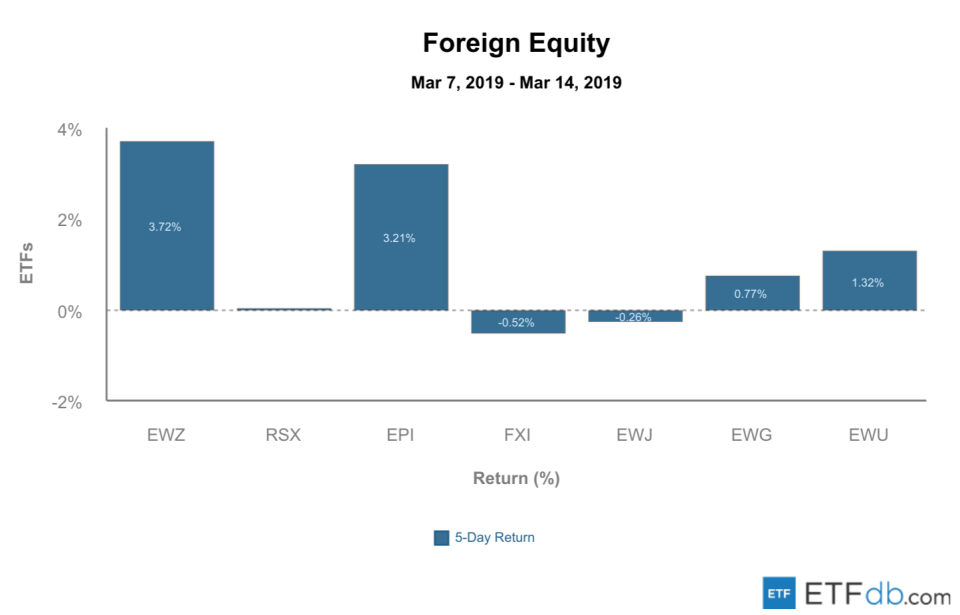

Foreign Equity Review

Foreign equities were mixed. Brazilian equities (EWZ B+) surged 3.72% this week, reaching a record high on optimism rooted in President Jair Bolsonaro’s promised reforms. At the same time, Chinese equities (FXI A-) declined 0.52%, as a deal with U.S. on trade is expected to be delayed at least until April.

To find out more about ETFs exposed to particular countries, check our ETF Country Exposure Tool. Select a particular country from a world map and get a list of all ETFs tracking your pick.

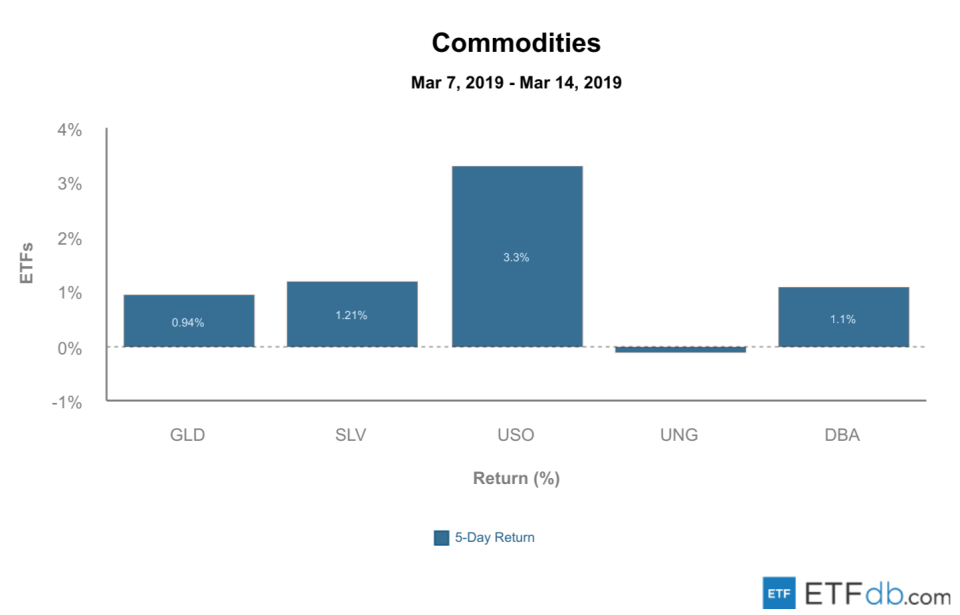

Commodities Review

Oil (USO A) advanced 3.3% this week, likely due to worries about production cuts prompted by OPEC and U.S. sanctions against Venezuela and Iran. However, an economic slowdown across the board threatens to derail the rally. Natural gas (UNG B-) was the worst performer, declining 0.12% for the week.

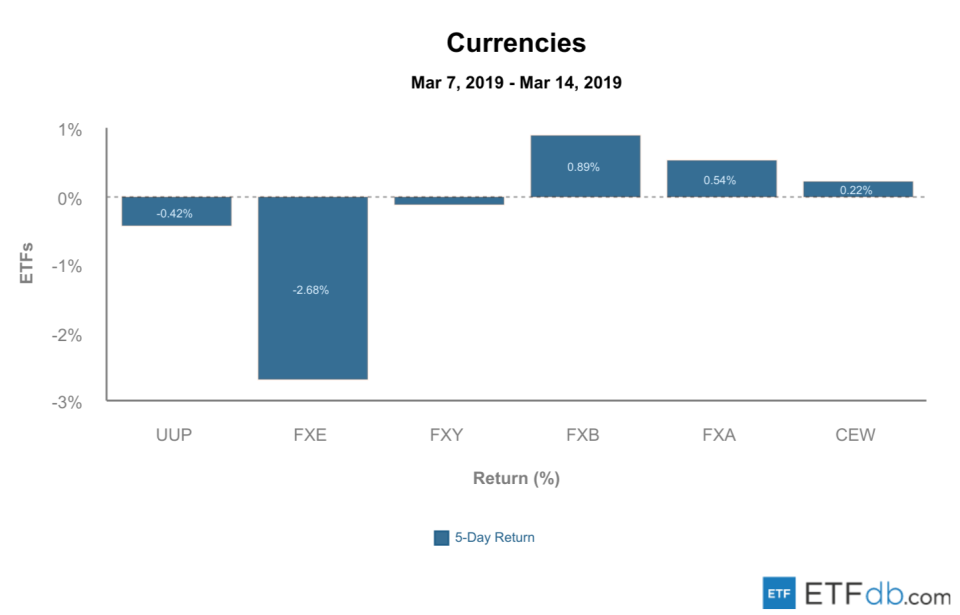

Currency Review

Euro (FXE A) continued to drop this week, losing as much as 2.68% of its value. The British pound (FXB A-), meanwhile, was surprisingly the best performer with an advance of 0.89% during the week. Investors likely cheered the fact that the British Parliament voted down a proposal to exit the European Union without a deal.

For more ETF analysis, make sure to sign up for our free ETF newsletter.

Disclosure: No positions at time of writing.