Expedia Offers an Attractive Buyback Yield and Upside Potential

In the past 12 months, Expedia Group Inc. (NASDAQ:EXPE) has delivered a decent gain of 29%. However, its long-term performance is a bit disappointing. In the past 10 years, it has only returned 90%, or a compounded annual return of 6.60%, which is lower than the S&P 500 at 10.30%.

As such, with the projected business growth going forward, the stock is quite undervalued at the current price.

Business overview

Expedia is a leading online travel company that has a comprehensive global network with more than 3 million lodging properties, including 940,000 hotels, alongside partnerships with over 500 airlines and a wide array of rental car services, cruises, insurance options and experiences. This extensive offering is made accessible through three consumer brands: Expedia, Hotels.com and Vrbo. The company operates across three main segments: Business to Consumer, Business to Business and Trivago.

The business-to-consumer segment, which is the primary source of revenue, generated $9.1 billion in 2023, accounting for approximately 71% of the company's total revenue. The business-to-business segment ranked second, contributing $3.39 billion, or 26.4% of the total. Trivago, the smallest segment, brought in $338 million in sales in 2023.

Expedia offers a diverse range of services to both consumers and businesses, including airline bookings, advertising and media solutions and lodging. Lodging stands out as the most significant service category, generating $10.26 billion in revenue in 2023, underscoring the company's strong position in the online travel market.

Growing revenue and consistent profitability

Expedia generates revenue by charging commissions on travel bookings made through its platform. This revenue comes from the gross bookings, which represent the total retail value of transactions booked for both agency and merchant transactions. Expedia earns a percentage of these gross bookings as its revenue, known as the revenue margin. Therefore, the company can increase its revenue in two ways: by increasing gross bookings or by improving the revenue margin.

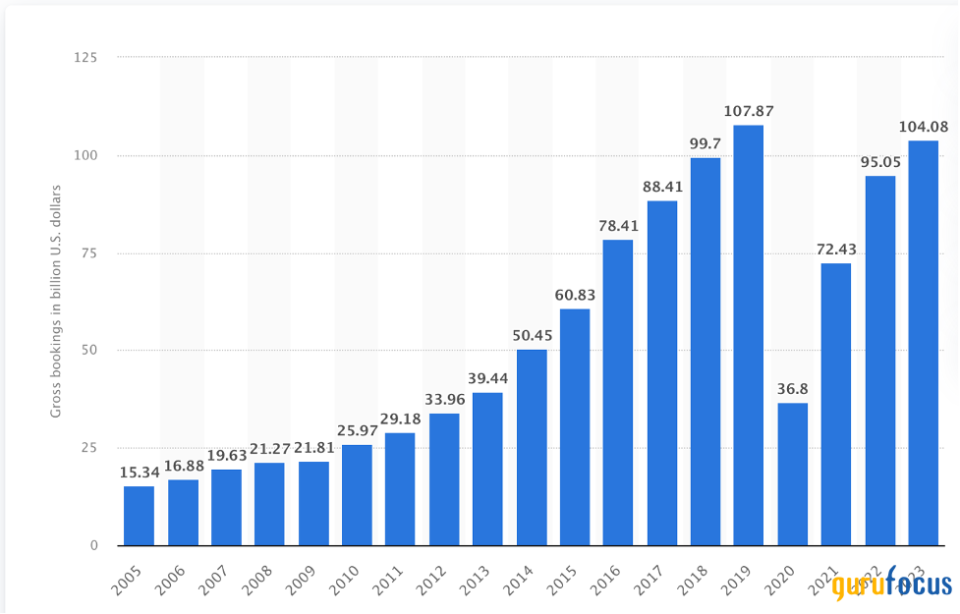

Since 2005, the company has successfully grown its gross bookings every year, with the exception of 2020 due to the Covid-19 pandemic. The gross bookings increased from $15.34 billion in 2005 to $107.87 billion in 2019. However, the pandemic severely impacted the global travel market, causing gross bookings to plummet to $36.80 billion. After the pandemic, gross bookings rebounded strongly to reach $104.10 billion in 2023.

Source: Statista

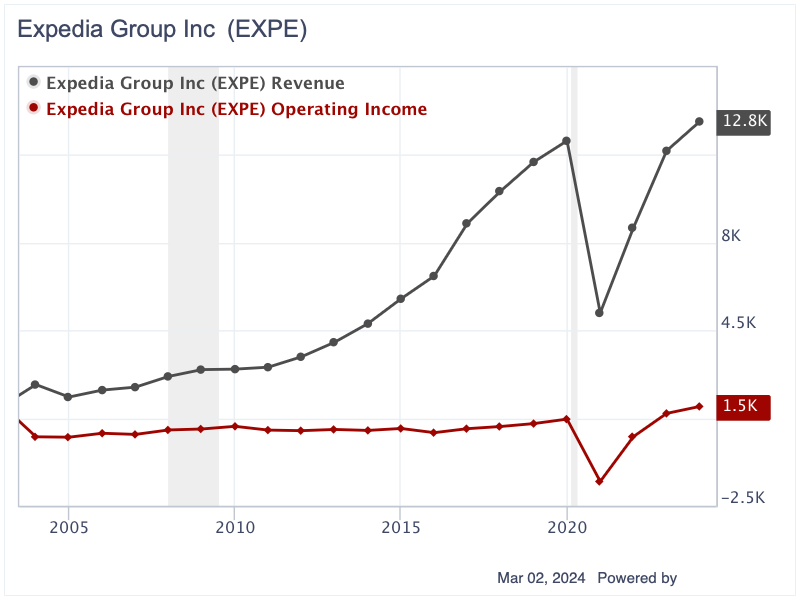

With the exception of 2020, Expedia's revenue and operating income have followed a consistent growth trend over the past 19 years. Revenue increased annually from $2.12 billion in 2005 to $12 billion in 2019, while the operating income surged from $397 million to $961 million. In 2020, when the whole world was locked down, less people were travelling and a lot of airlines and hotels went bankrupt, Expedia's business was also negatively affected. Its revenue fell to $5.20 billion while the operating income plummeted to $1.53 billion in losses. Fortunately, the company's revenue has recovered to $12.84 billion in 2023 and the operating income rebounded to $1.47 billion, surpassing the pre-pandemic level.

Expedia's business demonstrates notable resilience, with its performance only significantly impacted by extraordinary events like the pandemic. This resilience is underscored by the strong rebound in revenue and operating income, illustrating the company's robust recovery and growth capability in the aftermath of major global disruptions.

Huge cash position with conservative leverage

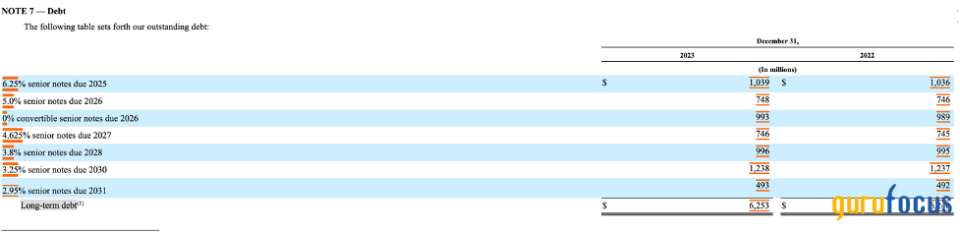

Expedia's balance sheet is quite strong with $2.8 billion in shareholders' equity at the end of 2023, including $5.66 billion in cash and restricted cash. Its long-term debt stood at $6.25 billion, resulting in a net cash position of $590 million. Thus, the company's net debt-to-equity ratio was quite conservative at 0.21. Debt maturities are spread from 2025 to 2031, with amounts due ranging from $750 million to $1.24 billion annually. The nearest debt obligation is $1.04 billion due in 2025. Given its operating cash flow of nearly $2.7 billion and substantial cash reserves, Expedia can comfortably manage its debt and interest payments.

Source: Expedia's 10-K filing

Expedia has regularly rewarded its shareholders through dividends and share buybacks. However, due to the pandemic, the company paused dividend payments and shifted its focus to increasing share repurchases. Over the past two years, Expedia has spent $2.55 billion to buy back 24.30 million shares, which represents 15% of its total outstanding shares. In October, it announced a new share buyback program worth up to $5 billion, offering a juicy repurchase yield of 26.80% based on the current market price.

Potential upside

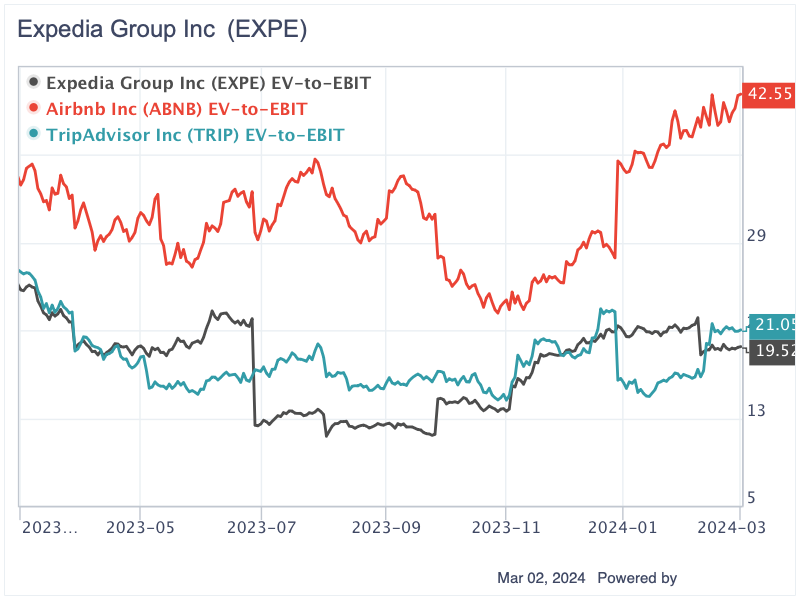

Compared to its competitors, including Airbnb (NASDAQ:ABNB) and TripAdvisor (NASDAQ:TRIP), Expedia is currently the most undervalued with an Ebit multiple of 19.52, while Airbnb and TripAdvisor have multiples of 42.55 and 21.05.

Analysts predict Expedia's revenue could reach $15.23 billion by 2025. Assuming the company maintains its 2023 operating margin of approximately 11.40%, this would result in an operating profit of $1.74 billion. By applying a 20 times earnings multiple, Expedia's enterprise value could approach nearly $35 billion by 2025. After applying a 10% discount rate, the company's value is estimated to be $28.90 billion. We also assume the company repurchases 10% of its total shares by 2025, reducing the total share count to 122.60 million, the value per share could be approximately $236, which is 72% higher than the current price.

Conclusion

Expedia can be considered a prime investment candidate with a robust balance sheet and prudent leverage, a resilient business model manifesting in consistent revenue and operating income growth, alongside a compelling potential for 72% upside in value. This unique combination of financial health, strategic market positioning and aggressive shareholder value enhancement initiatives, particularly through substantial share buyback programs, underscores Expedia's attractiveness.

For investors eyeing long-term gains within the rebounding travel sector, Expedia is a compelling opportunity, buoyed by its undervaluation relative to peers and promising growth trajectory.

This article first appeared on GuruFocus.