Is Fabrinet (FN) Modestly Overvalued? A Comprehensive Valuation Analysis

With a daily gain of 31.58%, a three-month gain of 57.58%, and an Earnings Per Share (EPS) of 6.58, Fabrinet (NYSE:FN) has been a stock of interest to investors. However, the question remains: is the stock modestly overvalued? This article aims to provide an in-depth valuation analysis of Fabrinet, encouraging readers to delve into the financial details and make informed investment decisions.

Company Overview

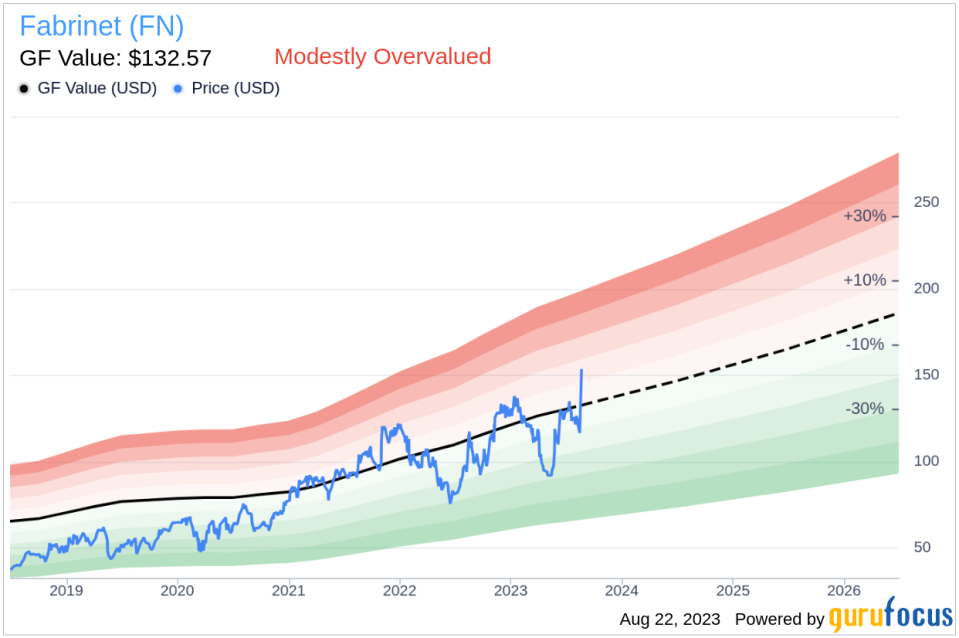

Fabrinet is a United States-based company engaged in providing outsourced manufacturing services to original equipment manufacturers (OEM). It offers a wide range of optical and electro-mechanical manufacturing capabilities across the whole producing process, helping its customers manufacture various products. With a market cap of $5.60 billion and a current stock price of $153.66 per share, Fabrinet appears to be modestly overvalued when compared to its GF Value of $132.57.

Understanding the GF Value

The GF Value is a unique measure of a stock's intrinsic value, calculated considering historical trading multiples, a GuruFocus adjustment factor based on past performance and growth, and future business performance estimates. If the stock price is significantly above the GF Value Line, it is overvalued and its future return is likely to be poor. Conversely, if it is significantly below the GF Value Line, its future return will likely be higher. Given that Fabrinet's stock price is slightly above its GF Value, it appears to be modestly overvalued, which suggests that the long-term return of its stock is likely to be lower than its business growth.

Financial Strength

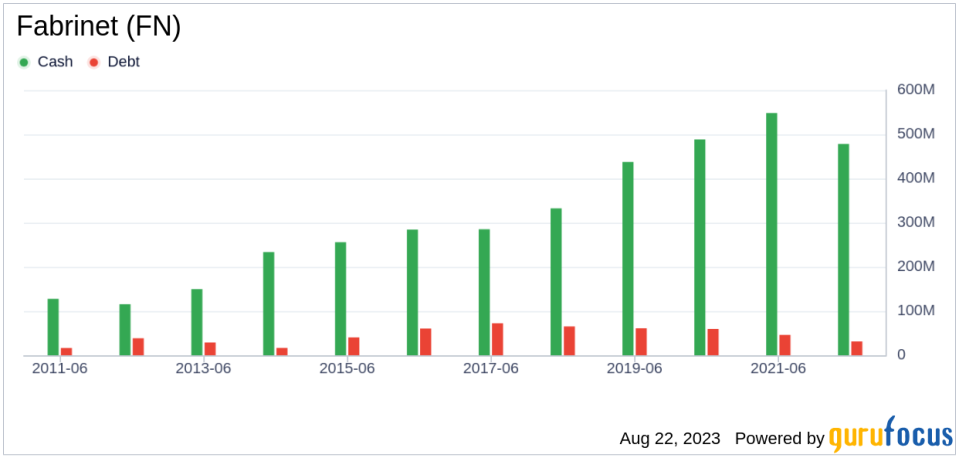

Investing in companies with poor financial strength can pose a high risk of permanent capital loss. Therefore, understanding a company's financial strength, such as its cash-to-debt ratio and interest coverage, is crucial. Fabrinet has a strong financial strength, with a cash-to-debt ratio of 31.57, ranking better than 85.69% of companies in the Hardware industry.

Profitability and Growth

Investing in profitable companies, especially those demonstrating consistent profitability over the long term, is typically less risky. Fabrinet has been profitable over the past 10 years, with an operating margin of 9.8%, ranking better than 75.15% of companies in the Hardware industry. Furthermore, its growth is impressive, with a 3-year average annual revenue growth rate of 12.6%, ranking better than 73.58% of companies in the Hardware industry.

ROIC vs WACC

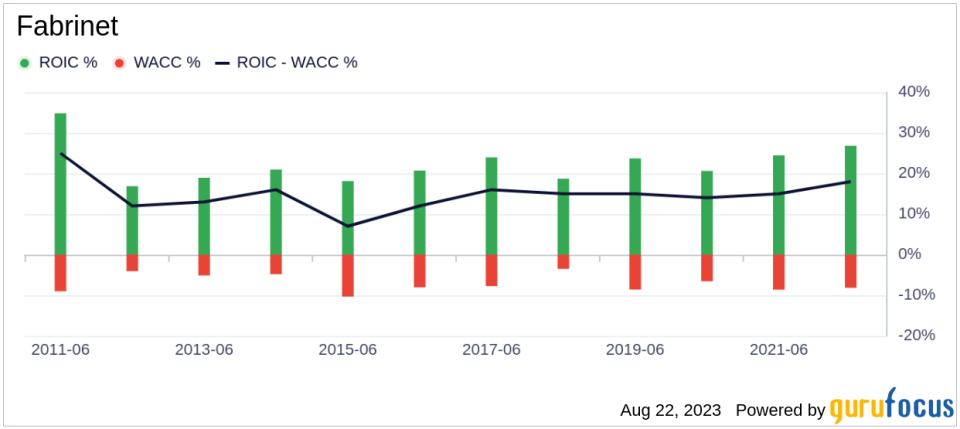

Comparing a company's return on invested capital (ROIC) to its weighted cost of capital (WACC) is another way to evaluate its profitability. If the ROIC is higher than the WACC, it indicates that the company is creating value for shareholders. Over the past 12 months, Fabrinet's ROIC was 28.23, while its WACC came in at 10.14.

Conclusion

In conclusion, Fabrinet (NYSE:FN) appears to be modestly overvalued. Despite strong financial condition and profitability, its growth ranks better than 58.39% of 1949 companies in the Hardware industry. For more details about Fabrinet stock, check out its 30-Year Financials here.

For high-quality companies that may deliver above-average returns, visit the GuruFocus High Quality Low Capex Screener.

This article first appeared on GuruFocus.