Fair Isaac (FICO) Q1 Earnings Lag Estimates, Revenues Up Y/Y

Fair Isaac FICO reported first-quarter fiscal 2024 earnings of $4.81 per share, missing the Zacks Consensus Estimate by 0.41% but rising 13% year over year.

Revenues of $382.1 million increased 10.8% on a year-over-year basis but lagged the consensus mark by 1.16%. Americas, EMEA and Asia Pacific contributed 85%, 9% and 6% to total revenues, respectively.

Mortgage originations revenues increased 188%. Auto originations revenues declined 3% year over year. Credit card and personal loan revenues declined 5%.

The company’s shares have outperformed the Zacks Computer & Technology sector year to date. While FICO’s shares have gained 47%, the Computer & Technology sector has increased 38.4%.

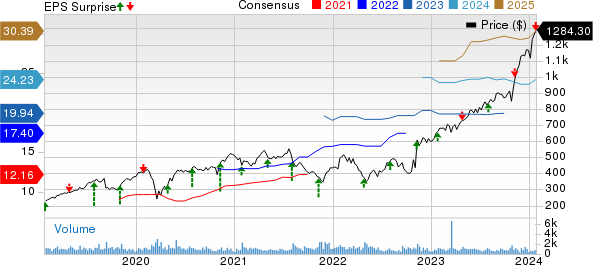

Fair Isaac Corporation Price, Consensus and EPS Surprise

Fair Isaac Corporation price-consensus-eps-surprise-chart | Fair Isaac Corporation Quote

Top-Line Details

Software revenues, which include Fair Isaac’s analytics and digital decisioning technology, as well as associated professional services, increased 13.8% year over year to $189.9 million.

Software Annual Recurring Revenues (ARR) increased 18% year over year, consisting of 43% platform ARR growth and 11% non-platform growth. Software Dollar-Based Net Retention Rate was 114% in the fiscal first quarter, with platform software at 136% and non-platform software at 108%.

Annual contract value bookings decreased 15% year over year to $18.3 million.

On-premises and SaaS Software (44.1% of revenues) increased 16.7% year over year to $168.7 million. Professional services (5.6% of revenues) were $21.3 million, down 4.7% year over year.

Scores (50.3% of revenues) increased 7.9% year over year to $192.1 million. Scores include FICO’s business-to-business (B2B) scoring solutions and business-to-consumer (B2C) scoring solutions.

B2B revenues increased 12% year over year, driven primarily by unit price increases, partially offset by declines in mortgage origination volumes. B2C revenues dropped 3% year over year due to lower volumes on myFICO.com business.

Operating Details

Research & development expenses, as a percentage of revenues, increased 50 basis points (bps) on a year-over-year basis to 11.2%.

Selling, general and administrative expenses, as a percentage of revenues, increased 30 bps year over year to 27.3%.

Operating margin was 39.6% in the reported quarter, which contracted 110 bps year over year.

Balance Sheet & Cash Flow

As of Dec 31, 2023, FICO had $160.4 million in cash and cash equivalents and total debt was $1.87 billion. In comparison, as of Sep 30, 2023, FICO had $136 million in cash and cash equivalents and total debt of $1.87 billion.

Cash flow from operations was $122.1 million in the fiscal first quarter compared with $164 million in the previous quarter. Free cash flow was $120.8 million compared with $163 million reported in the previous quarter.

Guidance

For fiscal 2024, FICO anticipates revenues to be $1.675 billion.

Non-GAAP earnings are still projected to be $22.45 per share.

Zacks Rank & Other Stocks to Consider

Currently, FICO carries a Zacks Rank #2 (Buy).

Shopify SHOP, Pinterest PINS and AvidXchange AVDX are some other top-ranked stocks that investors can consider in the broader sector, each sporting a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Shopify shares have gained 25.8% in the past six-month period. SHOP is set to report its fourth-quarter 2023 results on Feb 13.

Pinterest shares have gained 37.7% in the past six-month period. PINS is set to report its fourth-quarter 2023 results on Feb 8.

AvidXchange shares have declined 9.5% in the past six-month period. AVDX is set to report its fourth-quarter 2023 results on Feb 28.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Fair Isaac Corporation (FICO) : Free Stock Analysis Report

Shopify Inc. (SHOP) : Free Stock Analysis Report

AvidXchange Holdings, Inc. (AVDX) : Free Stock Analysis Report

Pinterest, Inc. (PINS) : Free Stock Analysis Report