It raises rates, it lowers rates. Whatever it does, the Federal Reserve always catches headlines for its decisions on monetary policy.

In an effort to reform the nation’s banking system, six men met at the Jekyll Island Club in 1910 and drafted the framework for a central bank of the United States. Three years later, President Woodrow Wilson signed it into law, creating the Federal Reserve System that we hear so much about today.

In its modern form, the Fed does more than just make decisions on monetary policy. It also ensures financial stability and supervises and regulates financial institutions.

As the central bank for the world’s largest economy, Fed decisions are not only critical for the U.S. — they have ripple effects across the world.

Although the Fed’s decisions sound extremely technical, changes to monetary policy have an impact on everyday life, too. Fed decisions on interest rates, for example, have an impact on mortgage rates and the yield you earn on deposits.

But what is the Federal Reserve and how does it conduct monetary policy to steer the economy?

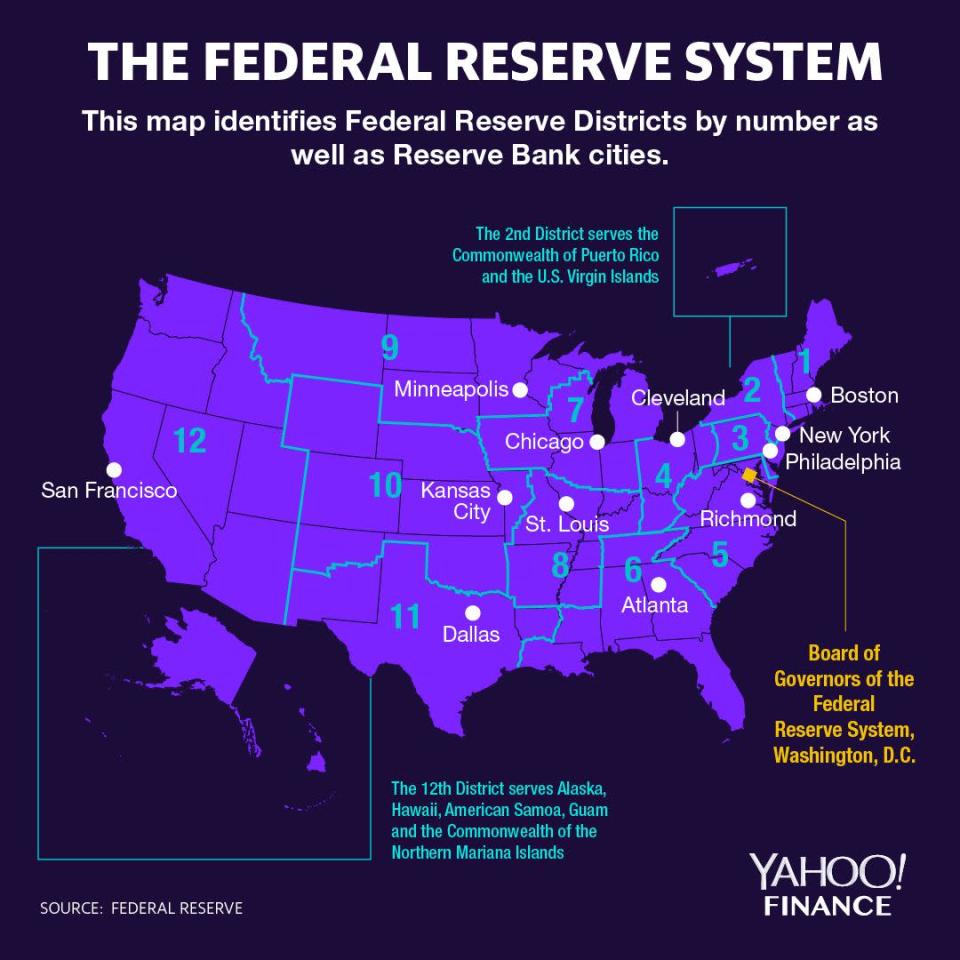

One board, 12 districts

The Federal Reserve System is a network of reserve banks scattered across the country, all reporting to a board of governors based out of Washington, D.C.

There are 12 reserve banks, each of which has a president who is tasked with monitoring the economic conditions in their assigned geographical boundaries. They report to Washington, D.C., where the Fed Chair and six other governors head the system and form aggregated views of the U.S. economy.

Every year, four of the reserve bank presidents rotate into the Federal Open Market Committee, a panel of Fed officials tasked with setting monetary policy. By design, this system ensures that the committee decisions include a diversity of economic views from different corners of the country.

The FOMC makes decisions eight times a year in two-day meetings that usually conclude on a Wednesday. At the conclusion of those meetings, the FOMC announces updates on its stance of monetary policy, usually to much media attention. The Fed chair used to host press conferences in every other FOMC meeting, but current Chairman Jerome Powell has made himself available for press questions after every FOMC meeting.

Interest Rates

The Fed has said that interest rates are its main tool for steering monetary policy.

But when the Fed announces changes to its interest rates, what is the central bank actually doing?

In its FOMC meetings, the Fed sets a target range for the federal funds rate — the benchmark interest rate that ripples through the economy and affects the cost of borrowing for businesses and individuals.

When the Fed adjusts rates, it is effectively changing the price of money. Think of a bank loan; the cost is not the principal of the loan itself, it's the interest payments that you pay on the loan. Higher interest makes for more expensive borrowing costs and lower interest makes for cheaper borrowing costs.

The Fed serves as the bankers’ bank, and pays interest on reserves that banks park at the central bank overnight. So when the FOMC decides to, for example, raise the federal funds rate by 25 basis points, they will set a target like 2.25% to 2.50%. To nudge interest rates up into that range, the Fed notches up its interest rate on bank reserves to set a new benchmark reference rate for the nation’s largest lenders.

The Fed also sets a floor for the effective federal funds rate through its reverse repurchase program, a more in-the-weeds system that involves temporarily swapping securities for cash at a specified interest rate.

Generally, higher interest rates encourage banks to leave more money at the Federal Reserve, therefore reducing the amount of money that the bank is willing to lend. For the loans that they do issue, such as mortgages and other consumer credit, banks will also raise rates and thus increase borrowing costs across the economy.

The reverse happens when the Fed lowers interest rates; banks would have less incentive to leave money at the Fed and would instead use its money to lend to businesses and consumers at lower borrowing cost levels.

For this reason, increasing interest rates are often referred to as “tight” or “contractionary” policy since it is aimed at reducing borrowing activity in an economy that might be running hot. Lowering interest rates is referred to as “loose” or “expansionary” policy because lower rates are generally aimed at stimulating a tepid economy.

The Fed makes judgment calls on rate changes depending on how it assesses the U.S. economy. But Congress gave the Fed mandated goals that lawmakers could refer to when checking the Fed’s work on steering the economy. Those two goals are maximum employment and stable prices. Currently, the Fed gauges maximum employment as a low unemployment rate and looks at stable prices from the lens of a 2% inflation target.

The Balance Sheet

But interest rates aren’t the only lever that the Fed uses to steer the economy.

After the financial crisis, the Fed took on trillions of dollars in assets to absorb the negative shock of the mortgage collapse. As part of an effort to stop the contagion of the housing market, the Fed booked a large amount of agency mortgage-backed securities and agency debt in a strategy of unconventional monetary policy called “quantitative easing.”

The move was designed to absorb the deteriorating assets and, in turn, inject liquidity into the economy.

The Fed also added long-term Treasurys to its balance sheet as part of its “Operation Twist” program, which flattened the yield curve and signaled its commitment to accommodative monetary policy as it attempted to crawl out of recession.

With the Fed now in an effort to normalize rates, the Fed hopes to undo its holdings of these unconventional assets, as well. Through the process of “quantitative tightening,” the Fed wants to clean its balance sheet so that it is primarily comprised of shorter-term Treasurys.

But why did the Fed undertake this new monetary policy tool to begin with? The Fed lowered interest rates in order to stimulate an economy that was spiraling out of control and ended up hitting the zero bound, meaning that policymakers — under then Fed Chairman Ben Bernanke — were forced to turn to a strategy of balance sheet management that had never been done before.

By undoing quantitative easing the Fed is again entering uncharted territory, sparking some uneasiness in markets over the impact of the process on market liquidity.

Over just the last 15 years, the Fed has not only been the focus of financial market participants around the world — it’s been the focus of speculators who wonder how these new monetary policy tools will change central banking in the future.

Brian Cheung is a reporter covering the banking industry and the intersection of finance and policy for Yahoo Finance. You can follow him on Twitter @bcheungz.