FEMSA (FMX) Stock Rallies 65% in the Past Year: What's Ahead?

Fomento Economico Mexicano S.A.B. de C.V. FMX, alias FEMSA, appears to be a lucrative pick with solid growth prospects. The company has been in investors’ good books due to gains from growth across all business units, a solid online show and continued strength in OXXO Mexico and OXXO Gas. It has been on track with its strategy of creating a distribution platform in the United States by expanding its footprint in the specialized distribution industry.

The company is also poised for growth through investments in digital and technology-driven initiatives. Moreover, FEMSA displays solid financial flexibility.

FEMSA reported top and bottom line beat for the second consecutive quarter in second-quarter 2023. The company’s adjusted net majority earnings per ADS benefited from robust sales growth, improved gross margin and lower interest expenses. FEMSA's revenues improved 18.3% year over year in the local currency. Gains across its business units drove revenue growth. On an organic basis, total revenues rose 9.5%.

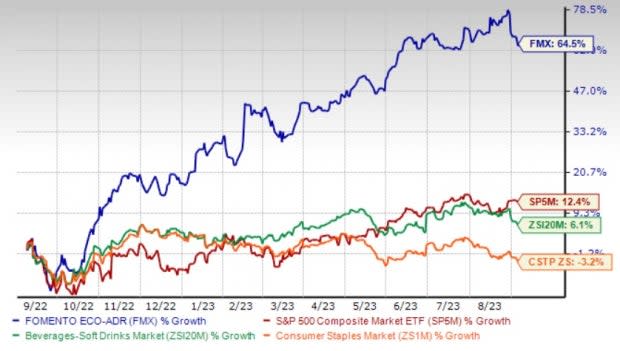

Shares of this Zacks Rank #1 (Strong Buy) company have rallied 64.5% in the past year compared with the industry’s growth of 6.1%. The FMX stock also compared favorably with the sector’s decline of 3.2% and the S&P 500’s 12.4% rise. You can see the complete list of today’s Zacks #1 Rank stocks here.

Image Source: Zacks Investment Research

Factors Likely to Drive Growth

FEMSA will likely continue witnessing momentum driven by strength across business units resulting from effective growth strategies and robust market demand.

FEMSA has been gaining pace in the digital space through its tech and innovation business unit — Digital@FEMSA. The unit is focused on building a value-added digital and financial ecosystem for end customers and businesses. It is also inclined toward enabling and leveraging the strategic assets of FEMSA’s core business verticals.

The company’s Coca-Cola FEMSA is leading the way with its omni-channel business, while the Proximity division is progressing with the adoption of digital initiatives for the OXXO stores. Within its OXXO store chains, the company is on track with investing in digital offerings, loyalty programs and fintech platforms, to evolve stronger over the long term. Its OXXO digital wallet, OXXO Premia and loyalty program have been performing well. The company made progress on its digital efforts, with the continued addition of Spin Premia and Spin by OXXO customers at an accelerated Pace.

Spin by OXXO received its definitive authorization to operate as a fintech in Mexico. Spin by OXXO reached 7.6 million users in second-quarter 2023, suggesting a 142.1% growth year over year. Active users at Spin by OXXO currently represent 75.8% of the acquired user base. Meanwhile, Spin Premia reached 32.7 million users in the second quarter, reflecting a year-over-year growth of 115%. Active users at Spin Premia represented 48.3% of the total acquired user base.

FEMSA’s venture in the specialized distribution industry relates to its plan of investing in adjacent businesses, which can leverage capabilities across different markets, providing an opportunity for attractive growth and risk-adjusted returns.

With the presence of its OXXO business and other retail operations, the company has become an expert in the organization and management of supply chains and distribution systems. FEMSA serves several businesses and retail customers through millions of interactions in different industries.

Key Picks

We have highlighted three top-ranked stocks from the Consumer Staple sector, namely PepsiCo Inc. PEP, McCormick & Company MKC and Ambev ABEV.

PepsiCo has a trailing four-quarter earnings surprise of 6.3%, on average. It currently carries a Zacks Rank #2. Shares of PEP have gained 1.2% in the past year.

The Zacks Consensus Estimate for PepsiCo’s current financial-year sales and earnings suggests growth of 6.7% and 10.2%, respectively, from the year-ago period's reported figures. PEP has an expected EPS growth rate of 8.1% for three to five years.

McCormick currently sports a Zacks Rank #2. The company has an expected EPS growth rate of 7.5% for three to five years. Shares of MKC have risen 1% in the past year.

The Zacks Consensus Estimate for McCormick’s current financial year’s sales and earnings per share suggests 6.4% and 5.1% growth, respectively, from the year-ago period’s reported figures. MKC has a trailing four-quarter negative earnings surprise of 4.2% on average.

Ambev has a trailing four-quarter earnings surprise of 20.8% on average. It currently carries a Zacks Rank #2. Shares of ABEV have declined 5.1% in the past year.

The Zacks Consensus Estimate for Ambev’s current financial-year sales suggests growth of 4.5% from the year-ago period's reported figure. Meanwhile, the consensus estimate for earnings indicates a decline of 5.6% from the year-ago quarter’s reported figure. ABEV has an expected EPS growth rate of 7% for three to five years.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Fomento Economico Mexicano S.A.B. de C.V. (FMX) : Free Stock Analysis Report

PepsiCo, Inc. (PEP) : Free Stock Analysis Report

McCormick & Company, Incorporated (MKC) : Free Stock Analysis Report

Ambev S.A. (ABEV) : Free Stock Analysis Report