How Financially Strong Is Methanex Corporation (TSE:MX)?

Small-cap and large-cap companies receive a lot of attention from investors, but mid-cap stocks like Methanex Corporation (TSX:MX), with a market cap of CA$7.23B, are often out of the spotlight. While they are less talked about as an investment category, mid-cap risk-adjusted returns have generally been better than more commonly focused stocks that fall into the small- or large-cap categories. Today we will look at MX’s financial liquidity and debt levels, which are strong indicators for whether the company can weather economic downturns or fund strategic acquisitions for future growth. Remember this is a very top-level look that focuses exclusively on financial health, so I recommend a deeper analysis into MX here. View our latest analysis for Methanex

How does MX’s operating cash flow stack up against its debt?

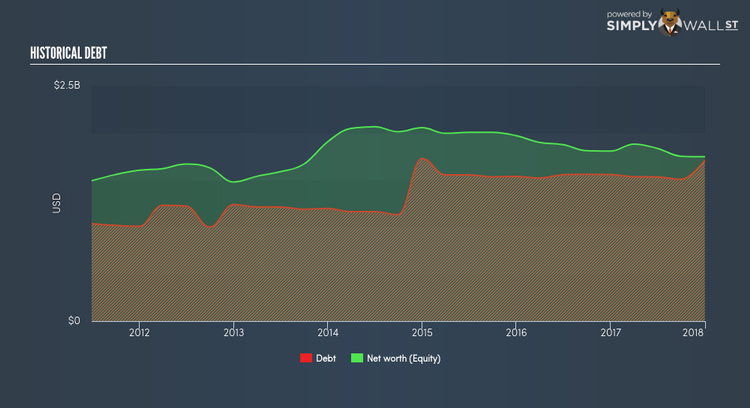

Over the past year, MX has ramped up its debt from US$1.56B to US$1.71B , which is made up of current and long term debt. With this increase in debt, the current cash and short-term investment levels stands at US$375.48M for investing into the business. On top of this, MX has produced cash from operations of US$787.74M in the last twelve months, resulting in an operating cash to total debt ratio of 46.16%, signalling that MX’s debt is appropriately covered by operating cash. This ratio can also be a sign of operational efficiency as an alternative to return on assets. In MX’s case, it is able to generate 0.46x cash from its debt capital.

Can MX pay its short-term liabilities?

With current liabilities at US$747.95M, the company has maintained a safe level of current assets to meet its obligations, with the current ratio last standing at 1.66x. Generally, for Chemicals companies, this is a reasonable ratio since there is a bit of a cash buffer without leaving too much capital in a low-return environment.

Can MX service its debt comfortably?

MX is a relatively highly levered company with a debt-to-equity of 97.79%. This is not uncommon for a mid-cap company given that debt tends to be lower-cost and at times, more accessible. No matter how high the company’s debt, if it can easily cover the interest payments, it’s considered to be efficient with its use of excess leverage. A company generating earnings after interest and tax at least three times its net interest payments is considered financially sound. In MX’s case, the ratio of 5.84x suggests that interest is appropriately covered, which means that debtors may be willing to loan the company more money, giving MX ample headroom to grow its debt facilities.

Next Steps:

Although MX’s debt level is towards the higher end of the spectrum, its cash flow coverage seems adequate to meet obligations which means its debt is being efficiently utilised. Since there is also no concerns around MX’s liquidity needs, this may be its optimal capital structure for the time being. I admit this is a fairly basic analysis for MX’s financial health. Other important fundamentals need to be considered alongside. I suggest you continue to research Methanex to get a better picture of the mid-cap by looking at:

Future Outlook: What are well-informed industry analysts predicting for MX’s future growth? Take a look at our free research report of analyst consensus for MX’s outlook.

Valuation: What is MX worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether MX is currently mispriced by the market.

Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.