Five9 (NASDAQ:FIVN) Posts Better-Than-Expected Sales In Q3 But Stock Drops On Weak Guidance

Call center software provider Five9 (NASDAQ: FIVN) reported Q3 FY2023 results exceeding Wall Street analysts' expectations , with revenue up 16% year on year to $230.1 million. However, next quarter's revenue guidance of $237.6 million was less impressive, coming in 2.52% below analysts' estimates. Turning to EPS, Five9 made a non-GAAP profit of $0.52 per share, improving from its profit of $0.39 per share in the same quarter last year.

Is now the time to buy Five9? Find out by accessing our full research report, it's free.

Five9 (FIVN) Q3 FY2023 Highlights:

Revenue: $230.1 million vs analyst estimates of $224.5 million (2.48% beat)

EPS (non-GAAP): $0.52 vs analyst estimates of $0.44 (18.9% beat)

Revenue Guidance for Q4 2023 is $237.6 million at the midpoint, below analyst estimates of $243.7 million

Free Cash Flow of $31.5 million, up 108% from the previous quarter

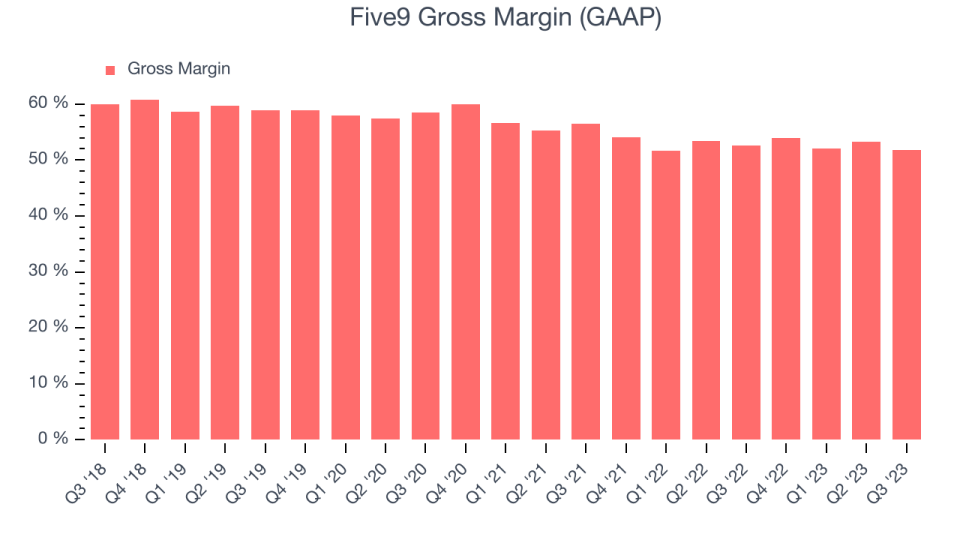

Gross Margin (GAAP): 51.7%, down from 52.6% in the same quarter last year

Started in 2001, Five9 (NASDAQ: FIVN) offers software as a service that makes it easier for companies to set up and efficiently run call centers, and offer more tailored customer support.

Video Conferencing

Work is becoming more distributed, both across geographies and devices. In order for businesses to keep functioning efficiently, they need to be able to communicate as well as they did when the teams were co-located, which drives the demand for integrated communication platforms.

Sales Growth

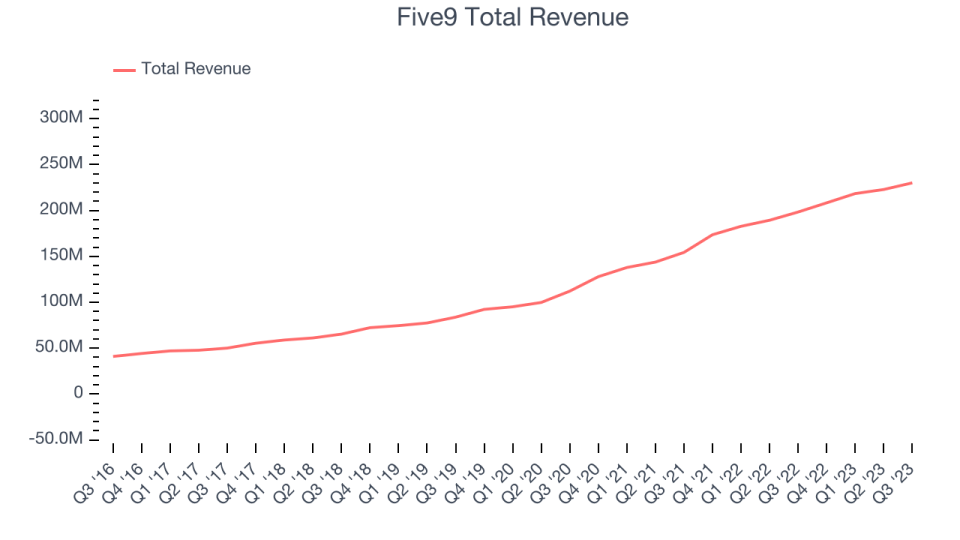

As you can see below, Five9's revenue growth has been strong over the last two years, growing from $154.3 million in Q3 FY2021 to $230.1 million this quarter.

This quarter, Five9's quarterly revenue was once again up 16% year on year. We can see that Five9's revenue increased by $7.22 million quarter on quarter, which is a solid improvement from the $4.44 million increase in Q2 2023. Shareholders should applaud the acceleration of growth.

Next quarter's guidance suggests that Five9 is expecting revenue to grow 14% year on year to $237.6 million, slowing down from the 20% year-on-year increase it recorded in the same quarter last year. Looking ahead, analysts covering the company were expecting sales to grow 16.4% over the next 12 months before the earnings results announcement.

The pandemic fundamentally changed several consumer habits. There is a founder-led company that is massively benefiting from this shift. The business has grown astonishingly fast, with 40%+ free cash flow margins. Its fundamentals are undoubtedly best-in-class. Still, the total addressable market is so big that the company has room to grow many times in size. You can find it on our platform for free.

Profitability

What makes the software as a service business so attractive is that once the software is developed, it typically shouldn't cost much to provide it as an ongoing service to customers. Five9's gross profit margin, an important metric measuring how much money there's left after paying for servers, licenses, technical support, and other necessary running expenses, was 51.7% in Q3.

That means that for every $1 in revenue the company had $0.52 left to spend on developing new products, sales and marketing, and general administrative overhead. Five9's gross margin is poor for a SaaS business and it's dropped significantly since the previous quarter. This is probably the exact opposite of what shareholders would like to see.

Key Takeaways from Five9's Q3 Results

With a market capitalization of $4.02 billion, Five9 is among smaller companies, but its $700.3 million cash balance and positive free cash flow over the last 12 months give us confidence that it has the resources needed to pursue a high-growth business strategy.

It was good to see Five9 beat analysts' revenue expectations this quarter. That really stood out as a positive in these results. On the other hand, its revenue guidance for next quarter underwhelmed and its gross margin decreased. Overall, this was a mediocre quarter for Five9. The company is down 6.88% on the results and currently trades at $52.5 per share.

Five9 may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.

The author has no position in any of the stocks mentioned in this report.