FLEX Stock Surges 23% YTD: Will the Upward Trend Continue?

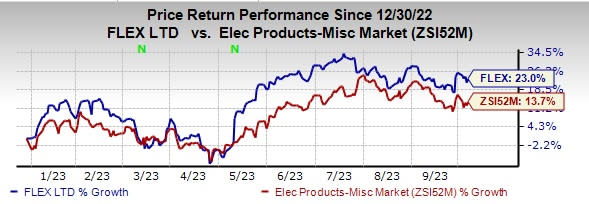

Flex FLEX witnessed strong momentum this year so far, with its shares rallying 23% compared with the sub-industry’s rise of 13.7%.

The company has a diverse workforce across 30 countries and offers advanced manufacturing solutions and supply-chain services throughout the product lifecycle development, including fulfillment, after-market support and circular economy solutions.

Image Source: Zacks Investment Research

Catalysts Behind the Price Surge

Let’s delve into the factors working in favor of this Zacks Rank #3 (Hold) stock.

The company is benefiting from the continued momentum in the company’s Reliability Solutions segment, backed by a strong customer backlog. In the last reported quarter, segmental revenues improved 11% year over year to $3.3 billion.

The company’s automotive sector benefits from the increasing demand for electric vehicles and advanced driver-assistance systems. The company’s healthcare segment is expected to benefit from strong demand for elective procedures and a continued ramp-up in large medical device programs.

The industrial segment is likely to benefit from solid demand for renewables, automation and critical power. Over the long term, the company expects Communications & Enterprise Compute to benefit from secular growth trends in cloud and networking technology.

For fiscal 2024, Flex expects revenues between $30.5 billion and $31.5 billion. It anticipates adjusted earnings per share (EPS) in the range of $2.35-$2.55. Adjusted operating margin is projected in the band of 5-5.2%.

FLEX’s fiscal 2024 and 2025 revenues are anticipated to rise 4.2% and 4.8% year over year, respectively. The company’s earnings are expected to increase 4.7% and 12.4% on a year-over-year basis in fiscal 2024 and 2025, respectively.

However, the increasing slowdown in enterprise IT spending due to rising macroeconomic uncertainty is a headwind. The lifestyle segment is likely to suffer from weakness in consumer-related demand. A leveraged balance sheet is an added concern.

Stocks to Consider

Some better-ranked stocks in the broader technology space are Asure Software ASUR, Woodward WWD and Watts Water Technologies WTS. Asure Software currently sports a Zacks Rank #1 (Strong Buy), whereas Woodward and Watts Water Technologies carry a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Asure Software’s 2023 EPS has increased 35% in the past 60 days to 54 cents.

Asure Software’s earnings beat the Zacks Consensus Estimate in all the last four quarters, the average being 676.4%. Shares of ASUR have surged 68% in the past year.

The Zacks Consensus Estimate for Woodward’s fiscal 2023 EPS has increased 5.6% in the past 60 days to $4.15.

WWD’s long-term earnings growth rate is 18.8%. Shares of WWD have gained 44.7% in the past year.

The Zacks Consensus Estimate for Watts Water’s 2023 EPS has increased 4.8% in the past 60 days to $7.78. The company’s long-term earnings growth rate is 7.5%.

Watts Water’s earnings beat estimates in all the trailing four quarters, delivering an average surprise of 12.5%. Shares of WTS have rallied 37.2% in the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Flex Ltd. (FLEX) : Free Stock Analysis Report

Asure Software Inc (ASUR) : Free Stock Analysis Report

Watts Water Technologies, Inc. (WTS) : Free Stock Analysis Report

Woodward, Inc. (WWD) : Free Stock Analysis Report