Generac (GNRC) Q4 Earnings & Revenues Miss Estimates, Up Y/Y

Generac Holdings Inc GNRC reported fourth-quarter 2023 adjusted earnings per share (EPS) of $2.07, which missed the Zacks Consensus Estimate of $2.10. GNRC reported adjusted EPS of $1.78 in the prior year.

Net sales increased 1% year over year to $1.06 billion but fell short of the consensus estimate by 3.07%. The year-over-year performance was driven by improvement across both the segments.

In the quarter under review, core sales growth (excluding the impact of acquisitions and foreign currency) remained unchanged year over year.

For 2023, GNRC reported a 12% decline in revenues to $$4.02 billion. However, the company expects sales to return to growth in 2024.

For 2024, GNRC expects revenues to increase in the range of 3-7%, including a slight net favorable impact from foreign currency changes. Revenues will be driven by momentum in residential product sales growth which is forecast to be in the mid-teens range. Residential product sales growth will gain from shipments of home standby generators and residential energy technology products.

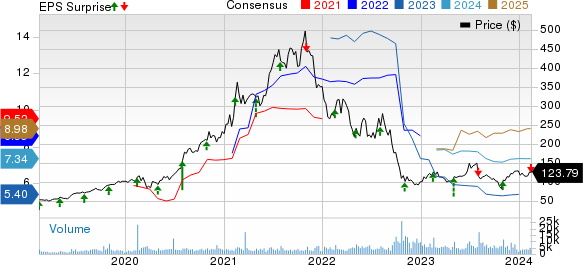

Generac Holdings Inc. Price, Consensus and EPS Surprise

Generac Holdings Inc. price-consensus-eps-surprise-chart | Generac Holdings Inc. Quote

However, C&I product sales are anticipated to decline 10% owing to weakness with certain direct rental, telecom and “beyond standby” customer, added GNRC.

Net income margin (before deducting for non-controlling interests) is now anticipated in the 6.5-7.5% range. Adjusted EBITDA margin is estimated in the 16.5-17.5% band.

Shares of GNRC are down 6.1% in the pre-market trading on Feb 14. The stock has lost 8.5% of its value compared with the sub-industry’s decline of 49.6%.

Image Source: Zacks Investment Research

Quarter in Details

Segment-wise, Domestic revenues were up 1% year over year to $891 million. Revenues rose on the back of higher home standby generator shipments and an increase in C&I product shipments. Reduced portable generator sales and a lower C&I product shipments to telecom and national rental equipment clients acted as headwinds.

International revenues fell 13% to $190.1 million, with acquisitions and favorable foreign currency movement and acquisitions providing a positive impact of 7%. Core revenues were down 20% due to weak inter-segment sales (owing to softness in the telecom market) and reduced portable generator shipments in Europe.

Product-wise, revenues from Residential inched up 1% to $580 million. C&I revenues were $363 million compared with $361 million in the year-ago quarter. Revenues from the Other product class totaled $120.4 million, gaining 6.5% year over year.

The Zacks Consensus Estimate for Residential and C&I products’ fourth-quarter revenues was pegged at $606 million and $372 million, respectively.

Margins

Gross profit was $388.7 million, up from $343.2 million in the prior-year quarter, with respective margins of 36.5% and 32.7%. Gross profit margin performance gained from favorable product mix, production efficiencies, and lower raw material and logistics expenses.

Total operating expenses were $237.8 million, up 0.8% year over year.

Operating income came in at $151 million, up 40.8% year over year. Adjusted EBITDA, before deducting for non-controlling interests, was $213 million compared with $174 million a year ago.

Cash Flow & Liquidity

In the fourth quarter, the company generated $317 million of net cash from operating activities. Free cash outflow totaled $266 million.

As of Dec 31, GNRC had $201 million of cash and cash equivalents, with $1.448 billion of long-term borrowings and finance lease obligations.

During the reported quarter, the company repurchased 1.3 million shares worth $151 million. GNRC bought back 2.2 million shares for $252 million in 2023.

In February 2024, GNRC approved a new stock buyback authorization that allows for the repurchase of up to $500 million over the next 24 months. It replaced the remaining balance on the earlier program.

Zacks Rank

Generac currently has a Zacks Rank #3 (Hold).

Stocks to Consider

Some better-ranked stocks worth consideration in the broader technology space are Watts Water Technologies WTS, Manhattan Associates MANH and Microsoft MSFT. While Manhattan Associates currently sports a Zacks Rank #1 (Strong Buy), Watts Water and Microsoft carry a Zacks Rank of 2 each. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Watts Water’s 2024 EPS has improved by 3 cents to $8.35 in the past 60 days. The long-term earnings growth rate is pegged at 7.8%. Shares of WTS have jumped 11.9% in the past year.

The Zacks Consensus Estimate for MANH’s 2024 EPS has increased by 3.6% in the past 60 days to $3.76.

Manhattan Associates’ earnings beat the Zacks Consensus Estimate in each of the last four quarters, the average surprise being 27.6%. Shares of MANH have surged 65.8% in the past year.

The Zacks Consensus Estimate for Microsoft’s fiscal 2024 EPS is pegged at $11.60, indicating growth of 18.3% from the year-ago levels. Microsoft’s earnings beat the Zacks Consensus Estimate in each of the last four quarters, the average surprise being 8.8%. The long-term earnings growth rate is pegged at 16.2%. MSFT has gained 50.9% in the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Microsoft Corporation (MSFT) : Free Stock Analysis Report

Manhattan Associates, Inc. (MANH) : Free Stock Analysis Report

Watts Water Technologies, Inc. (WTS) : Free Stock Analysis Report

Generac Holdings Inc. (GNRC) : Free Stock Analysis Report