General Mills (GIS) Q4 Earnings Top Estimates, Sales Rise Y/Y

General Mills, Inc. GIS posted fourth-quarter fiscal 2023 results, wherein the top and bottom lines improved year over year, and the latter came ahead of the Zacks Consensus Estimate.

Management remains focused on executing its Accelerate strategy. To this end, it has been committed to brand building and innovation, solidifying its capacities and reshaping its portfolio. GIS is on track with prioritizing core markets, global platforms and local brands, along with reshaping its portfolio via strategic acquisitions and divestitures.

Quarterly Highlights

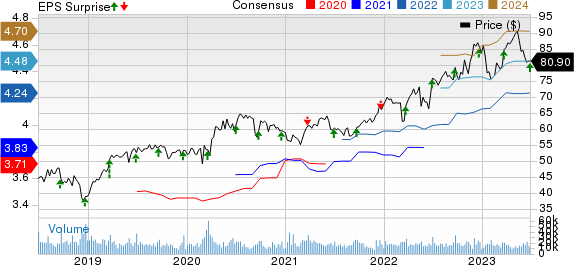

General Mills posted adjusted earnings of $1.12 per share, which beat the Zacks Consensus Estimate of $1.05. The bottom line rose 1% year over year on a constant-currency (cc) basis. The upside can be mainly attributed to decreased net shares outstanding, somewhat negated by reduced benefit plan non-service income.

General Mills, Inc. Price, Consensus and EPS Surprise

General Mills, Inc. price-consensus-eps-surprise-chart | General Mills, Inc. Quote

GIS reported net sales of $5,030 million, which came below the Zacks Consensus Estimate of $5,182 million. The top line advanced 3% from the year-ago quarter’s figure. The metric included a one-point unfavorable impact each from net divestitures, acquisition activity and currency movements. Organic net sales rose 5% due to the favorable organic net price realization and mix, partly countered by the reduced organic pound volume.

The adjusted gross margin expanded 120 basis points (bps) to 35% due to the positive net price realization and mix. These were somewhat offset by elevated input costs, with input cost inflation being 9% in the quarter.

The cc adjusted operating profit remained nearly flat year over year at $889 million as increased adjusted gross profit dollars were offset by higher adjusted SG&A expenses (which included a double-digit spike in media investments). The adjusted operating profit margin contracted 60 bps to 17.7%.

Segmental Performance

North America Retail: Revenues in the segment came in at $3,066 million, up 2% year over year. The uptick can be attributed to the positive net price realization and mix, which more than offset the reduced pound volume, including the adverse impacts of divestitures and currency headwinds. Organic net sales grew 5% year over year. The segment’s operating profit increased 2% to $779.5 million.

International: Revenues in the segment came in at $744.7 million, down 1% year over year. The downside can be attributed to the reduced pound volume, which includes the adverse impacts of divestitures and unfavorable currency rates. That said, the favorable net price realization and mix offered some respite.

Organic net sales grew 6% year over year due to solid growth in Europe & Australia and China. The segment’s operating profit tumbled 12% to $66.8 million.

Pet: Revenues came in at $655 million, which ascended 7% year over year due to the positive net price realization and mix, partly hurt by the lower pound volume. Organic sales also rose 7%. Segment net sales benefited from strong growth in dry pet food and pet treats. The segment’s operating profit came in at $133.2 million compared with the $113.3 million reported in the year-ago period.

North America Foodservice: Revenues came in at $564.3 million, up 7% year over year. Net sales were mainly backed by a six-point gain from the TNT Crust buyout. Organic sales rose 1%, including an adverse impact of two points from market index pricing on bakery flour. The segment’s operating profit fell 10% to $72.5 million.

Other Financial Aspects

General Mills ended the quarter with cash and cash equivalents of $585.5 million, long-term debt of $9,965.1 million and total shareholders’ equity of $10,449.6 million.

GIS generated $2.8 billion in cash from operating activities in fiscal 2023. Capital investments amounted to $690 million during the same period. Free cash flow conversion was 80% of the company’s adjusted after-tax earnings in fiscal 2023.

The company paid out dividends worth $1.3 billion and bought roughly 18 million shares for $1.4 billion in fiscal 2023. Concurrently, management announced a 9% hike in its quarterly dividend, taking it to 59 cents per share. This is payable on Aug 1, 2023 to stockholders of record as of Jul 10.

Other Developments

Cc sales from the joint ventures of Cereal Partners Worldwide increased 8%. In Haagen-Dazs Japan, sales remained flat year over year at cc with the prior-year figure.

Fiscal 2024 Guidance

General Mills expects that the biggest factors impacting its show in fiscal 2024 are likely to be consumers’ economic status, cost inflation and the rising stability of supply-chain status.

For fiscal 2024, management expects input cost inflation of 5% percent of the total cost of goods sold, stemming from labor inflation. Labor inflation continues to impact the costs of sourcing, manufacturing and logistics. Management expects HMM cost savings of 4% of the cost of goods sold in fiscal 2024.

For fiscal 2024, organic net sales are anticipated to increase 3-4%, driven by robust marketing, innovation and in-store support. Also, gains from net price realization through the company’s Strategic Revenue Management initiative are likely to aid.

The net impact of divestitures and foreign currency movements is likely to lower the full-year reported net sales growth by about half a percent.

The adjusted operating profit growth at cc is anticipated at 4-6%. Adjusted EPS growth at cc is also envisioned between 4% and 6%. Currency woes are likely to have a negligible impact on the adjusted operating profit and adjusted EPS growth.

This Zacks Rank #3 (Hold) company’s shares have rallied 8.2% in the past year compared with the industry’s growth of 6.2%.

Solid Staple Stocks

Some better-ranked consumer staple stocks are Nomad Foods NOMD, McCormick & Company, Incorporated MKC and Lamb Weston LW.

Nomad Foods, a frozen food product company, currently sports a Zacks Rank #1 (Strong Buy). NOMD has a trailing four-quarter earnings surprise of 8.5%, on average. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Nomad Foods’ current fiscal-year sales suggests growth of around 8% from the year-ago reported figures.

McCormick, which operates as a manufacturer, marketer and distributor of spices, seasonings, specialty foods and flavors, currently carries a Zacks Rank #2 (Buy). MKC has a trailing four-quarter negative earnings surprise of 3.7%, on average.

The Zacks Consensus Estimate for McCormick’s current fiscal-year sales and earnings suggests growth of 6.4% and 3.6%, respectively, from the year-ago reported numbers.

Lamb Weston, which is a frozen potato product company, currently carries a Zacks Rank #2. LW has a trailing four-quarter earnings surprise of 47.6%, on average.

The Zacks Consensus Estimate for Lamb Weston’s current fiscal-year sales and earnings suggests growth of 30% and 117.3%, respectively, from the year-ago reported numbers.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

General Mills, Inc. (GIS) : Free Stock Analysis Report

McCormick & Company, Incorporated (MKC) : Free Stock Analysis Report

Lamb Weston (LW) : Free Stock Analysis Report

Nomad Foods Limited (NOMD) : Free Stock Analysis Report