Genesco (NYSE:GCO) Beats Q4 Sales Targets

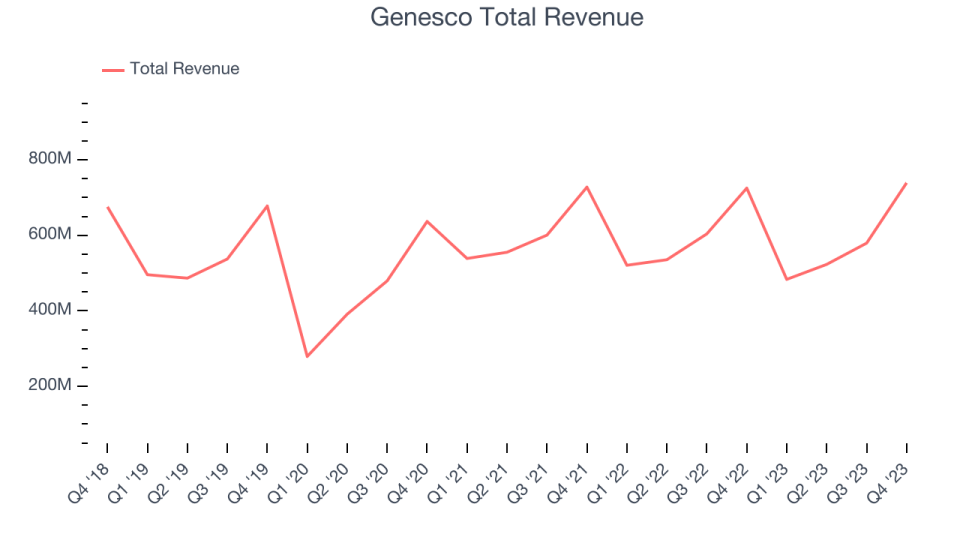

Footwear, apparel, and accessories retailer Genesco (NYSE:GCO) beat analysts' expectations in Q4 FY2024, with revenue up 1.9% year on year to $739 million. It made a non-GAAP profit of $2.59 per share, down from its profit of $3.06 per share in the same quarter last year.

Is now the time to buy Genesco? Find out by accessing our full research report, it's free.

Genesco (GCO) Q4 FY2024 Highlights:

Revenue: $739 million vs analyst estimates of $704.9 million (4.8% beat)

EPS (non-GAAP): $2.59 vs analyst expectations of $2.66 (2.5% miss)

Revenue guidance for the full year 2024 of a 2-3% decrease compared to 2023

EPS (non-GAAP) guidance for the full year 2024 missed expectations

Gross Margin (GAAP): 46.3%, in line with the same quarter last year

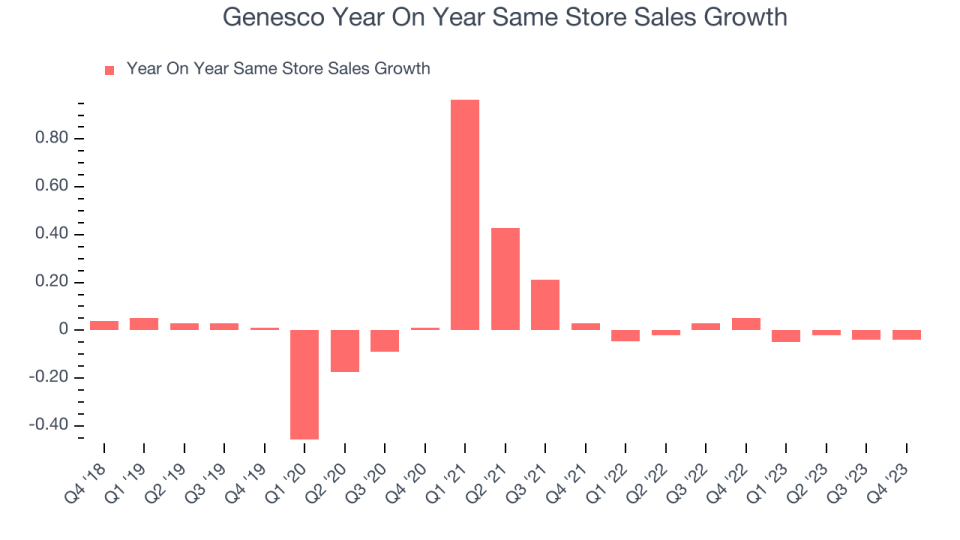

Same-Store Sales were down 4% year on year

Store Locations: 1,341 at quarter end, decreasing by 69 over the last 12 months

Market Capitalization: $336.3 million

Mimi E. Vaughn, Genesco’s Board Chair, President and Chief Executive Officer, said, “Our Fiscal 2024 results reflect the significant shift we’ve seen in our Journeys consumer’s shopping behavior. The year began with a very challenging start, and we reacted quickly to implement strategies that drove sequential improvement in Journeys comp every quarter of the year. Although the Holiday season started off positively, consumers subsequently shopped almost exclusively for key footwear items with a notable shift away from boots, putting more pressure on our core product assortment than we anticipated at the beginning of Q4. At the same time, we delivered another year of record sales for Schuh and Johnston & Murphy.”

Spanning a broad range of styles, brands, and prices, Genesco (NYSE:GCO) sells footwear, apparel, and accessories through multiple brands and banners.

Footwear Retailer

Footwear sales–like their apparel counterparts–are driven by seasons, trends, and innovation more so than absolute need and similarly face the bigger-picture secular trend of e-commerce penetration. Footwear plays a part in societal belonging, personal expression, and occasion, and retailers selling shoes recognize this. Therefore, they aim to balance selection, competitive prices, and the latest trends to attract consumers. Unlike their apparel counterparts, footwear retailers most sell popular third-party brands (as opposed to their own exclusive brands), which could mean less exclusivity of product but more nimbleness to pivot to what’s hot.

Sales Growth

Genesco is a small retailer, which sometimes brings disadvantages compared to larger competitors that benefit from economies of scale.

As you can see below, the company's annualized revenue growth rate of 1.4% over the last four years (we compare to 2019 to normalize for COVID-19 impacts) was weak as its store count dropped.

This quarter, Genesco reported decent year-on-year revenue growth of 1.9%, and its $739 million in revenue topped Wall Street's estimates by 4.8%. Looking ahead, Wall Street expects revenue to decline 6.1% over the next 12 months, a deceleration from this quarter.

Today’s young investors likely haven’t read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Same-Store Sales

A company's same-store sales growth shows the year-on-year change in sales for its brick-and-mortar stores that have been open for at least a year, give or take, and e-commerce platform. This is a key performance indicator for retailers because it measures organic growth and demand.

Genesco's demand has been shrinking over the last eight quarters, and on average, its same-store sales have declined by 1.7% year on year. The company has been reducing its store count as fewer locations sometimes lead to higher same-store sales, but that hasn't been the case here.

In the latest quarter, Genesco's same-store sales fell 4% year on year. This decline was a reversal from the 5% year-on-year increase it posted 12 months ago. We'll be keeping a close eye on the company to see if this turns into a longer-term trend.

Key Takeaways from Genesco's Q4 Results

We liked that revenue beat analysts' expectations this quarter despite a same store sales miss. We were also happy its gross margin narrowly outperformed Wall Street's estimates. On the other hand, the company expects revenue to decrease 2-3% in 2024 compared to 2023, and its full-year earnings forecast missed analysts' expectations. Zooming out, we think this was still a decent, albeit mixed, quarter, with the guidance likely dragging down shares. Investors were likely expecting more, and the stock is down 2.7% after reporting, trading at $28.5 per share.

So should you invest in Genesco right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.