Goldman Sachs Lifts S&P 500 Price Target; Here Are 2 High-Upside Stocks to Play the Bounce

Year-to-date, the S&P 500 has delivered an impressive return of 14%. However, those gains are a bit deceiving as the bulk of the upside has been driven by only a few selected stocks, namely the tech Mega Caps (AAPL, MSFT, NVDA, META, AMZN). If we exclude those five stocks, the index has only advanced by 5%.

While one could argue that the market is due for a cooling down period after such a rally, Goldman Sachs Chief U.S. Equity Strategist David Kostin suggests otherwise, citing past evidence. “Prior episodes of sharply narrowing breadth have been followed by a ‘catch-up’ from a broader valuation re-rating,” Kostin explained.

As such, Kostin not only increased Goldman’s year-end price target for the S&P 500 from 4000 to 4500 (a 12.5% lift), but there’s also the prospect of stocks yet to reap the benefits of the rally closing the gap as the year progresses.

Against this backdrop, Goldman Sachs analysts have been seeking out those equities and have turned their focus to two that have plenty of upside, according to their calculations – in the order of 90%, or more. Running the tickers through the TipRanks database, it’s clear Goldman is not alone in thinking these stocks have plenty to offer investors; both are also rated as Strong Buys by the analyst consensus.

Rent the Runway (RENT)

Our first Goldman-backed stock is a disruptor in the fashion industry. Rent the Runway lives up to its moniker by accurately describing its activities, which involve offering clients the opportunity to rent high-end fashion items. This concept of temporary ownership allows customers to browse a diverse range of styles, sizes, and brands on the Rent the Runway website or mobile app. They can then choose items to rent for specific occasions or timeframes. The platform provides options for both one-time rentals and subscription plans. In line with the trends of 2023, the company utilizes AI algorithms and machine learning techniques to enhance various aspects of its business, including inventory management and personalization.

It’s a formula that helped the company deliver a strong set of results in its most recent readout – for the fiscal first quarter of 2023 (April quarter). Revenue rose by 10.6% year-over-year to $74.2 million, beating the Street’s expectations by $0.99 million. Likewise, EPS of -$0.46 came in better than the -$0.49 the prognosticators were looking for. That said, concerns about the outlook blotted the performance. The company sees FQ2 revenue hitting the range between $77 million to $79 million. Consensus was looking for 81 million.

Shares pulled back consequently and have generally lagged the market this year – declining by 24% so far. For Goldman Sachs analyst Eric Sheridan, however, the present valuation represents an opportunity for investors.

“In our view, RENT shares (at current levels) are not pricing-in the multi-year scenario of 25% topline growth and scaling margins that mgmt. outlined last quarter,” said the 5-star analyst. “Longer term, we still see RENT as the leader in the subscription-based effort to drive the adoption of the sharing economy theme in the apparel sector. In particular, we would flag RENT mgmt’s comments on AI as a potential positive for their platform and a broader disruptive force for the industry which warrants further attention in coming quarters.”

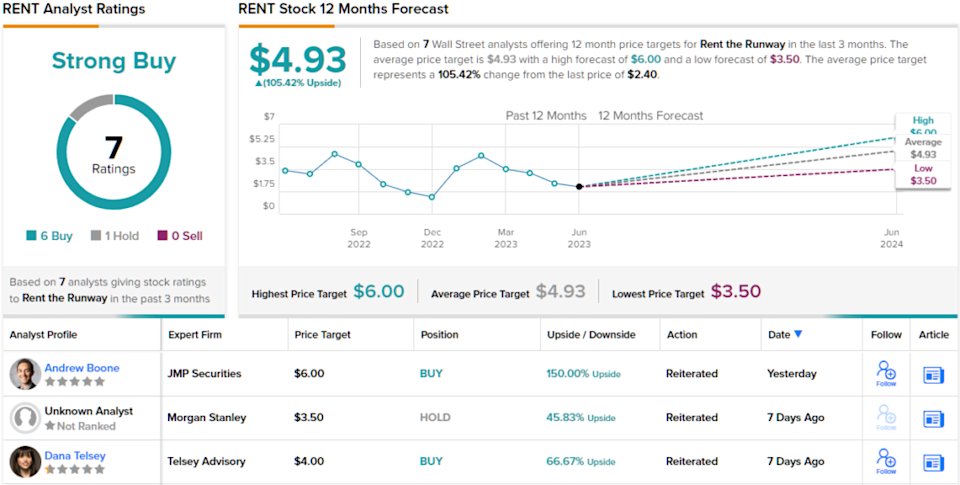

These comments underpin Sheridan’s Buy rating on RENT, while his $6 price target suggests the stock will run up by a bountiful 150% over the coming year. (To watch Sheridan’s track record, click here)

Sheridan’s upbeat thesis gets support on the Street. The stock’s Strong Buy consensus rating is based on 6 Buys vs. 1 Hold. Additionally, the $4.93 average target leaves room for one-year gains of 105%. (See RENT stock forecast)

Arrowhead Pharmaceuticals (ARWR)

For our next Goldman-backed name we’ll switch gears and head to the biotech space. Arrowhead Pharmaceuticals is at the forefront of RNA interference (RNAi) therapeutics, developing innovative medicines that target and silence specific disease-causing genes. The company’s cutting-edge technology, known as the Targeted RNAi Molecule (TRiM) platform, enables the precise delivery of RNAi drugs to specific tissues and organs, opening up new possibilities for the treatment of various diseases.

The company has a lengthy and diverse clinical pipeline and some eye-catching industry collaborations including Takeda, Amgen, and Horizon Therapeutics. Looking forward, Arrowhead expects to have 18 drug candidates in clinical studies by the end of 2023, addressing a broad range of cell types, such as liver, solid tumor, pulmonary, CNS, and skeletal muscle. It also already has candidates in Phase 3 studies.

Further back in development, but making some promising progress, the company is also developing ARO-RAGE, currently in a Phase 1/2 study for the treatment of patients with asthma. This drug has been showing some positive results. At Arrowhead’s recent R&D Day, the firm presented data that showed that a single inhaled dose of 184 mg knocked down the RAGE protein – which is correlated with lung diseases such as asthma – by an average of 90% and up to a maximum of 95%.

This drug’s potential has caught the eye of Goldman Sachs analyst Madhu Kumar, who lays down the bullish thesis for the therapy.

“There is significant market potential for ARO-RAGE in the broader asthma therapeutic landscape,” said the 5-star analyst. “Specifically, we estimate the biologics market for eosinophilic asthma to reach over $4B in 2023 and grow to about $7B over the next five years. This estimate takes into account sales estimates for Tezspire from AMGN and JNJ, Nucala from GSK, Fasenra from AZN, and Dupixent from REGN and SNY.”

“While many of these biologics share the same dosing regimen as ARO-RAGE of once every four weeks (although ARO-RAGE could potentially be dosed less frequently), we see potential for differentiation with respect to efficacy, including rate of exacerbation, forced expiratory volume in 1 second (FEV1), and fractional exhaled nitric oxide (FeNO),” Kumar went on to add.

How does this all translate to investors? Kumar rates the shares as Buy, backed by a $68 price target. Should the figure be met, investors will be pocketing returns of 92% a year from now. (To watch Kumar’s track record, click here)

Elsewhere on the Street, ARWR receives an additional 8 Buys and 3 Holds, all coalescing to a Strong Buy consensus rating. Going by the $61.45 average target, the shares will climb ~74% higher over the 12-month timeframe. (See ARWR stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.