Goldman Sachs Says Attractive Valuations Make Small-Cap Stocks Appealing; Here Are 2 ‘Strong Buy’ Names With Solid Upside Potential

The S&P 500 is up by 14% year-to-date but it has not gone unnoticed that the robust performance has been driven by strong displays from the tech mega-caps.

According to Goldman Sachs strategist Lily Calcagnini, there are better investment opportunities right now further down the food chain.

“Small stocks trade at a valuation discount relative to large caps, suggesting now is an attractive entry point for investors with multi-year investing time horizons,” Calcagnini explained. “Even within the large cap universe, smaller companies look inexpensive relative to larger ones in the context of both the last 10 and 35 years.”

In fact, while Calcagnini makes the case that the S&P 500 will gain another 9% over the next year and hit 4,700, she anticipates a 14% rise in the small-cap focused Russell 2000 index, which will represent a 5 pp of outperformance vs. the S&P 500 outlook.

Meanwhile, the analysts at Goldman Sachs have been getting into the details and seeking out those small-caps with solid upside potential. We ran a couple of their picks through the TipRanks database to also gauge widespread Street sentiment. Turns out the Goldman experts are not the only ones keen on these Russell 2000-included names; both are rated as ‘Strong Buys’ by the analyst consensus. Let’s find out what makes them appealing investment choices right now.

Springworks Therapeutics (SWTX)

First up on our small-cap list, we’ll take a look at Springworks Therapeutics, a clinical-stage biopharma company with a $1.57 billion market cap. Springworks uses a precision medicine strategy to acquire, develop, and bring transformative medications to market, with the aim of improving the lives of individuals afflicted by debilitating cancers.

With biotechs it’s all about the pipeline, and Springworks currently has two drugs making headway in clinical trials across multiple programs.

The most advanced of these is oral, small-molecule, selective gamma secretase inhibitor nirogacestat, being assessed as a treatment for different cancers. Based on positive data from the Phase 3 DeFi trial, the FDA has accepted Springworks’ NDA (new drug application) for nirogacestat in desmoid tumors and a PDUFA date has been set for November 27 (extended from the prior August 27 date).

There’s another catalyst in the pipeline from the anticipated readout of topline data from the Phase 2b ReNeu study of allosteric MEK1/2 inhibitor mirdametinib in NF-1-associated plexiform neurofibroma. This should take place during the second half of the year. NF1 is a genetic disorder associated with a heightened susceptibility to tumors, making it one of the most prevalent syndromes of its kind. It currently impacts approximately 100,000 individuals in the US.

Assessing the pipeline and upcoming catalysts, Goldman Sachs analyst Corinne Jenkins highlights the potential of both these drugs: “Based on the available clinical data, we anticipate a high likelihood of approval for niro in DT… Additionally, we expect a strong launch given the high degree of physician awareness and support for niro in DT observed across our channel checks and SWTX’s market research. Beyond niro, we view the upcoming data from the Ph2b ReNeu study of mirdametinib in pediatrics and adults with NF-1-associated plexiform neurofibroma in 2H23 as driving the next leg of the story.”

These comments underpin Jenkins’ Buy rating on SWTX, while her $43 price target implies one-year share appreciation of ~71%. (To watch Jenkins’ track record, click here)

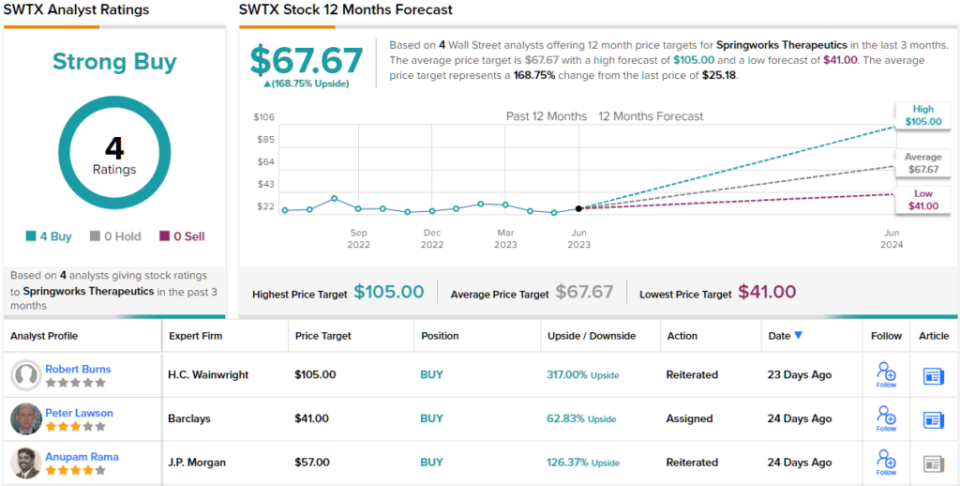

Other analysts are even more optimistic. Of the four investment banks that have rated SWTX over the past three months, all four agree the stock is a “buy” — and on average, they think it’s worth $67.67 a share — ~169% ahead of current pricing. (See SWTX stock forecast)

Arvinas, Inc. (ARVN)

We’ll stay in the biotech space for the next Goldman-backed small-cap. Boasting a market cap of $1.44 billion, Arvinas is a company focused on developing innovative protein degradation therapies to address a wide range of diseases. The company utilizes its proprietary PROTAC (PROteolysis TArgeting Chimera) platform, which harnesses the body’s natural protein disposal system to selectively eliminate disease-causing proteins. By targeting specific proteins for degradation, Arvinas aims to provide more effective and durable treatments compared to traditional small molecule inhibitors or antibodies.

Most of Arvinas’ pipeline is still in the pre-clinical stage but several drugs are in various stages of clinical testing. The most recent update concerned the progress of ARV-766, an investigational orally bioavailable PROTAC protein degrader being assessed in men with metastatic castration-resistant prostate cancer (mCRPC). Data from the Phase 1/2 dose escalation and expansion trial showed that ARV-766 was well-tolerated and displayed promising activity in a heavily pre-treated, post-NHA (novel hormonal agents), all-comers patient group.

Arvinas is also making headway in the development of bavdegalutamide (ARV-110), an additional orally administered PROTAC protein degrader. This potential treatment offers a beacon of hope for men battling metastatic castration-resistant prostate cancer (mCRPC) who have not responded to previously approved systemic therapies. The company is slated to kick off a Phase 3 trial in the latter half of 2023, and intends to disclose the data on radiographic progression-free survival from the Phase 1/2 trial within the same timeframe.

Despite the rich pipeline of therapeutic candidates, Arvinas shares are down 21% this year. According to Goldman Sachs analyst Madhu Kumar, this presents an opportunity for the stock to undergo substantial growth.

“Given the early signal, ARVN will advance ARV-766 in combination with abiraterone to pre-novel hormonal agent (NHA) patients in 2H23. Beyond ARV-766, updated data from the Phase 1/2 trial of AR PROTAC bavdegalutamide (bav), including radiographic progression-free survival (rPFS), will be presented at a medical congress in 2H23. Given the weakness in ARVN shares YTD, we believe even modest positive signals for the AR PROTAC franchise could generate upside,” Kumar noted.

How does this all translate to investors? Kumar rates ARVN a Buy along with a $91 price target. Should the figure be met, investors stand to pocket returns of an impressive 237% a year from now. (To watch Kumar’s track record, click here)

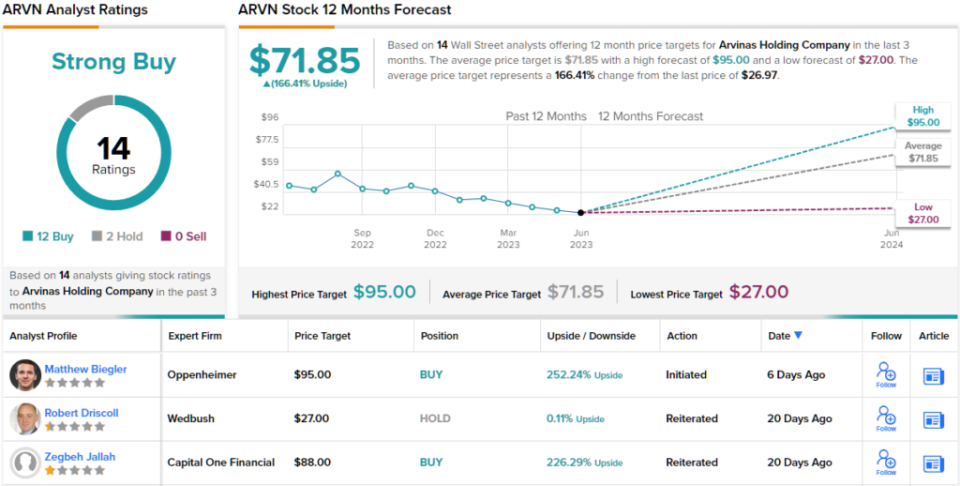

The view from the rest of the Street is hardly less upbeat. While 2 analysts prefer sitting this one out, all 12 other recent analyst reviews are positive, providing the stock with a Strong Buy consensus rating. The average target currently stands at $71.85, suggesting shares will post growth of 72% in the months ahead. (See ARVN stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a newly launched tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.