Is Good Times Restaurants a Value Trap? A Comprehensive Analysis

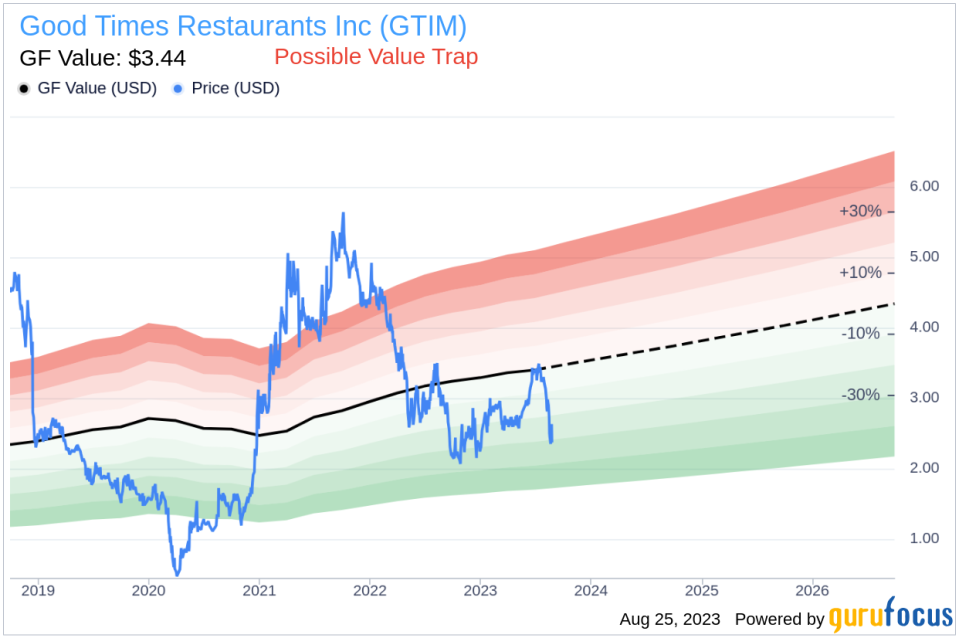

Value-focused investors are constantly seeking stocks priced below their intrinsic value. One such stock that warrants attention is Good Times Restaurants Inc (NASDAQ:GTIM). Currently priced at $2.37, the stock recorded a day loss of 9.89% and a 3-month decrease of 14.75%. According to its GF Value, the fair valuation of the stock is $3.44.

Understanding the GF Value

The GF Value represents the current intrinsic value of a stock derived from our exclusive method. The GF Value Line on our summary page provides an overview of the fair value that the stock should be traded at. It is calculated based on three factors: historical multiples (PE Ratio, PS Ratio, PB Ratio and Price-to-Free-Cash-Flow) that the stock has traded at, the GuruFocus adjustment factor based on the company's past returns and growth, and future estimates of the business performance. If the stock price is significantly above the GF Value Line, it is overvalued and its future return is likely to be poor. Conversely, if it is significantly below the GF Value Line, its future return will likely be higher.

However, a more in-depth analysis is necessary before making an investment decision. Despite its seemingly attractive valuation, certain risk factors associated with Good Times Restaurants should not be overlooked. These risks are primarily reflected through its low Altman Z-score of 1.48, and a Beneish M-Score of -1.58 that exceeds -1.78, the threshold for potential earnings manipulation. These indicators suggest that Good Times Restaurants, despite its apparent undervaluation, might be a potential value trap. This complexity underscores the importance of thorough due diligence in investment decision-making.

Altman Z-Score and Beneish M-Score Explained

The Altman Z-score, invented by New York University Professor Edward I. Altman in 1968, is a financial model that predicts the probability of a company entering bankruptcy within a two-year time frame. The Z-Score combines five different financial ratios, each weighted to create a final score. A score below 1.8 suggests a high likelihood of financial distress, while a score above 3 indicates a low risk.

Developed by Professor Messod Beneish, the Beneish M-Score is based on eight financial variables that reflect different aspects of a company's financial performance and position. These are Days Sales Outstanding (DSO), Gross Margin (GM), Total Long-term Assets Less Property, Plant and Equipment over Total Assets (TATA), change in Revenue (?REV), change in Depreciation and Amortization (?DA), change in Selling, General and Admin expenses (?SGA), change in Debt-to-Asset Ratio (?LVG), and Net Income Less Non-Operating Income and Cash Flow from Operations over Total Assets (?NOATA).

Company Overview: Good Times Restaurants Inc (NASDAQ:GTIM)

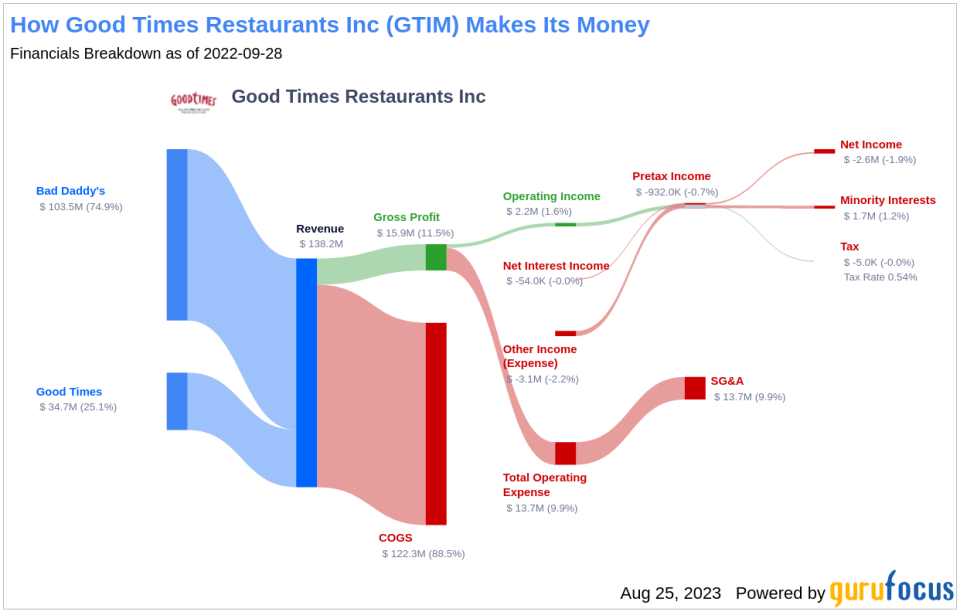

Good Times Restaurants Inc is engaged in developing, owning, operating, and franchising hamburger-oriented drive-through restaurants. It operates through two segments: Good Times Burgers and Frozen Custard restaurants, which operate in the quick-service drive-through dining industry; and Bad Daddy's Burger Bar restaurants, which operate in the full-service upscale casual dining industry. The company generates maximum revenue from the Bad Daddy's Burger Bar restaurants segment. Its menu categories include burgers; chicken; kids; breakfast; frozen custard; slides and drinks.

The income breakdown of Good Times Restaurants is as follows:

A Closer Look at Good Times Restaurants's Low Altman Z-Score

A breakdown of Good Times Restaurants's Altman Z-score reveals that the company's financial health may be weak, suggesting potential financial distress:

The Retained Earnings to Total Assets ratio provides insights into a company's capability to reinvest its profits or manage debt. Evaluating Good Times Restaurants's historical data, 2021: -0.30; 2022: -0.32; 2023: -0.21, a recent decline following an initial increase in this ratio indicates Good Times Restaurants's diminishing ability to reinvest in its business or effectively manage its debt. This negatively impacts its Z-Score.

The EBIT to Total Assets ratio serves as a crucial barometer of a company's operational effectiveness, correlating earnings before interest and taxes (EBIT) to total assets. An analysis of Good Times Restaurants's EBIT to Total Assets ratio from historical data (2021: 0.20; 2022: 0.02; 2023: -0.01) indicates a recent dip following an initial rise. This reduction suggests that Good Times Restaurants might not be utilizing its assets to their full potential to generate operational profits, negatively affecting the company's overall Z-score.

Examining Good Times Restaurants's Beneish M-Score

The days sales outstanding (DSO) is an important financial metric that denotes the average time a company takes to collect payment after a sale is completed. Looking at the historical data from the past three years (2021: 1.20; 2022: 1.47; 2023: 1.57), there appears to be a recent surge following an initial decline in Good Times Restaurants's DSO. A rising DSO figure warrants scrutiny as it can signal financial distress or questionable accounting practices within the company.

The Gross Margin index tracks the evolution of a company's gross profit as a proportion of its revenue. A downward trend could indicate issues such as overproduction or more generous credit terms, both of which are potential red flags for earnings manipulation. By examining the past three years of Good Times Restaurants's historical data (2021: 15.30; 2022: 11.88; 2023: 11.43), we find that its Gross Margin has contracted by 2.03%. Such a contraction in the gross margin can negatively impact the company's profitability as it signifies lesser income from each dollar of sales. This could put a strain on the company's capacity to manage operating costs, potentially undermining its financial stability.

The asset quality ratio, calculated as Total Long-term Assets minus Property, Plant, and Equipment, divided by Total Assets, gauges the proportion of intangible or less tangible assets within a company's asset structure. Analyzing Good Times Restaurants's asset quality ratio over the past three years (2021: 0.10; 2022: 0.11; 2023: 0.23), an increase might signal underlying issues, such as capitalizing normal operating expenses or goodwill impairment. These factors can inflate assets and mask true operational costs, potentially misrepresenting the company's actual financial position, and raising concerns for investors about its true value and risk profile.

The change in Depreciation, Depletion, and Amortization (DDA) reflects the rate at which a company's assets lose value over time. Analyzing Good Times Restaurants's DDA data over the past three years (2021: 7.48; 2022: 5.09; 2023: 7.59), a decreasing rate might be a cause for concern. This decline may suggest that the company is prolonging the useful life of its assets, possibly to manipulate earnings. By extending the lifespan of assets, depreciation charges are spread over a longer period, thereby reducing annual expenses and artificially boosting reported profits. While this may create a more favorable short-term financial picture, it could also distort the true value and condition of the company's assets, misleading investors and potentially hiding underlying operational or financial issues.

The TATA (Total Accruals to Total Assets) ratio, calculated as the Net Income less Non-Operating Income and Cash Flow from Operations, divided by Total Assets, is a key indicator of the quality of a company's earnings. For Good Times Restaurants, the current TATA ratio (TTM) stands at 0.075. A positive TATA ratio can be a warning sign, suggesting that the earnings are composed more of accruals rather than cash flow, which could be an indication of aggressive income recognition. Accrual accounting permits management some discretion in recognizing revenue and expenses, and a company intent on artificially boosting its earnings might exploit this flexibility.

Conclusion: Is Good Times Restaurants a Value Trap?

Given the analysis, there are several indicators that suggest Good Times Restaurants might be a potential value trap. Despite its seemingly attractive valuation, the company's financial health appears to be weak, raising concerns about potential financial distress. The low Altman Z-score and the high Beneish M-Score, which exceeds the threshold for potential earnings manipulation, further underscore these concerns. Therefore, investors should exercise caution and conduct thorough due diligence before making an investment decision.

GuruFocus Premium members can find stocks with high Altman Z-Score using the following Screener: Walter Schloss Screen . To find out the high-quality companies that may deliver above-average returns, please check out GuruFocus High Quality Low Capex Screener.

This article first appeared on GuruFocus.