GoPro's (GPRO) Q2 Loss In Line, Revenues Surpass Estimates

GoPro, Inc GPRO reported second-quarter 2023 non-GAAP loss of 7 cents per share, in line with the Zacks Consensus Estimate. The company reported earnings of 8 cents in the year-ago quarter.

GoPro generated revenues of $241 million, down 4% from the year-ago quarter’s levels. However, the top line beat the consensus mark by 9.1%.

Quarter in Details

GoPro shipped 704 million camera units during the reported quarter, up 10% year over year.

GPRO recorded 2.44 million subscribers, marking 27% year-over-year growth at the end of the quarter under discussion. Quik subscribers soared 6% to 294,000 from the prior-year quarter.

Region-wise, revenues from the Americas totaled $121.6 million (50.4% of total revenues), down 4% from the year-ago quarter’s levels. Revenues from Europe, the Middle East and Africa were $66.5 million (27.6%), declining 7% year over year. The Asia Pacific generated revenues of $52.9 million (22%), flat on a year-over-year basis.

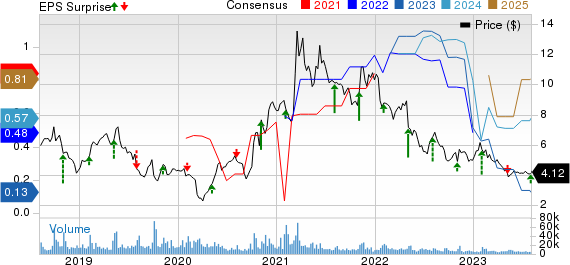

GoPro, Inc. Price, Consensus and EPS Surprise

GoPro, Inc. price-consensus-eps-surprise-chart | GoPro, Inc. Quote

Based on channels, revenues from GoPro.com reached $75.6 million (31.4% of total revenues), up 20.7% year over year. In this channel, hardware revenues totaled $51.2 million compared with $75.2 million in the previous-year quarter. Subscription revenues amounted to $24.4 million, climbing 21.4% year over year.

Retail channel registered revenues of $165.4 million (68.6%), up 6.4% from the year-ago quarter’s levels. Our estimate for segmental revenues was pegged at $123 million.

The company had $135.4 million in inventory compared with $126 million in the year-earlier quarter.

Other Details

Gross profit of $75.8 million decreased 21% year over year. Total operating expenses of $98.3 million improved 7.6% year over year. Operating loss totaled $22.5 million against operating income of $4.7 million in the prior-year quarter.

Non-GAAP gross margin was 31.6% compared with 38.5% in the year-ago quarter. Adjusted EBITDA loss was $10.3 million against adjusted EBITDA income of $16.9 million in the year-ago quarter. This was mainly due to the company’s price protection charges related to the new pricing strategy, and momentum in lower margin entry-level cameras.

Cameras with suggested retail prices at or above $400 contributed 75% to revenues in the reported quarter compared with 93% in the prior-year quarter.

Cash Flow & Liquidity

In the quarter under review, GoPro used $7.9 million of net cash from operating activities against $12.9 million of cash generated from operations in the year-ago period.

As of Jun 30, the company had $189.9 million of cash and cash equivalents with $141.5 million of long-term debt.

GPRO repurchased 3.6 million shares worth $15 million.

Guidance

For the third quarter of 2023, revenues are estimated to be $280 million (+/- $10 million). Non-GAAP adjusted earnings are expected to be 2 cents per share (+/- 2 cents).

Gross margin is anticipated to be 34% (+/- 50 basis points). Street ASP is projected to be nearly $355.

GoPro currently has a Zacks Rank #4 (Sell).

Stocks to Consider

Some better-ranked stocks worth consideration in the broader technology space are Badger Meter BMI, Salesforce CRM and Autodesk ADSK. Badger Meter flaunts a Zacks Rank #1 (Strong Buy) while each of Salesforce and Autodesk carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Badger Meter’s 2023 earnings has gained 6.3% in the past 60 days to $2.86 per share. BMI’s earnings beat the Zacks Consensus Estimate in the last four quarters, the average surprise being 6.7%. Shares of BMI have surged 70% in the past year.

The consensus mark for Salesforce’s fiscal 2024 earnings is pegged at $7.44 per share, up 0.3% in the past 60 days. The long-term earnings growth rate is anticipated to be 19.3%.

CRM’s earnings beat the Zacks Consensus Estimate in the last four quarters, the average surprise being 15.5%. Shares of CRM have grown 13.8% in the past year.

The consensus estimate for Autodesk’s fiscal 2024 earnings of $7.25 per share remained flat in the past 60 days. The long-term earnings growth rate is anticipated to be 24.3%.

ADSK’s earnings beat the Zacks Consensus Estimate in the last four quarters, the average beat being 2.1%. Shares of ADSK have declined 8.6% in the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Salesforce Inc. (CRM) : Free Stock Analysis Report

Badger Meter, Inc. (BMI) : Free Stock Analysis Report

GoPro, Inc. (GPRO) : Free Stock Analysis Report

Autodesk, Inc. (ADSK) : Free Stock Analysis Report