Griffon Corp (GFF) Reports Mixed Q1 Results with Strong Free Cash Flow and Share Repurchases

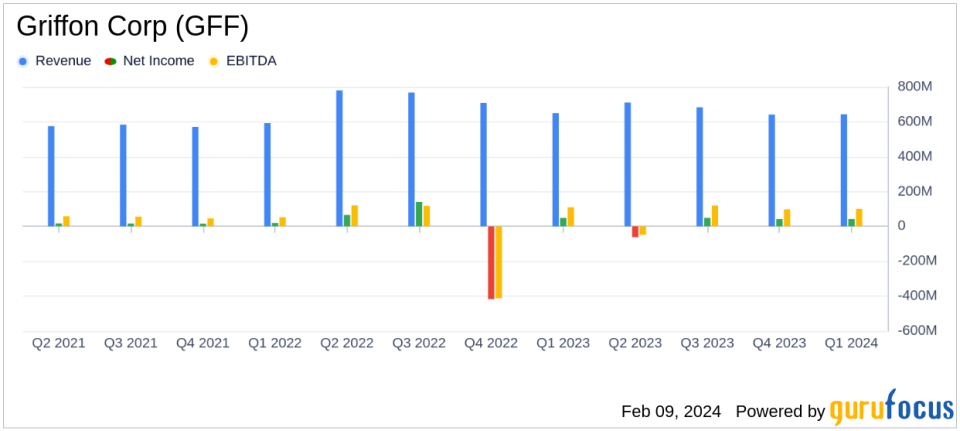

Revenue: Slight decrease to $643.2 million in Q1 FY2024 from $649.4 million in Q1 FY2023.

Net Income: Declined to $42.2 million, or $0.82 per share, from $48.7 million, or $0.88 per share year-over-year.

Adjusted Net Income: Increased to $55.3 million, or $1.07 per share, from $47.4 million, or $0.86 per share.

Adjusted EBITDA: Improved by 7% to $116.4 million from $108.6 million in the prior year quarter.

Free Cash Flow: Strong performance with $133 million, significantly up from the previous year.

Share Repurchases: $70 million of share repurchases executed, showcasing confidence in financial health.

On February 7, 2024, Griffon Corp (NYSE:GFF) released its 8-K filing, announcing the financial results for the first quarter of fiscal year 2024, which ended on December 31, 2023. The company, a conglomerate known for manufacturing and marketing residential, commercial, and industrial garage doors, as well as providing non-powered landscaping products, reported a slight decrease in revenue and a drop in net income compared to the same quarter in the previous year. However, adjusted net income and adjusted EBITDA both showed improvements, indicating underlying business strength.

Performance Highlights and Challenges

Griffon Corp's revenue for the first quarter totaled $643.2 million, a 1% decrease compared to the previous year's quarter. The net income saw a more significant decrease, from $48.7 million to $42.2 million year-over-year. Despite these challenges, the company's adjusted net income rose to $55.3 million, or $1.07 per share, compared to $47.4 million, or $0.86 per share, in the prior year quarter. This performance is particularly important as it reflects the company's ability to maintain profitability in a challenging environment.

The company's Home and Building Products (HBP) segment maintained its revenue, while the Consumer and Professional Products (CPP) segment experienced a 2% decrease, primarily due to reduced consumer demand in North America. Griffon's strong free cash flow of $133 million underscores its operational efficiency and ability to generate cash, which is critical for meeting financial obligations and pursuing growth opportunities.

Financial Achievements and Industry Significance

Griffon's financial achievements, such as the 7% increase in adjusted EBITDA to $116.4 million, are significant as they demonstrate the company's ability to grow its earnings before interest, taxes, depreciation, and amortization, which is a key indicator of financial health for conglomerates. The strong free cash flow performance is also noteworthy, as it provides the company with the liquidity to support strategic initiatives, such as the CPP global sourcing strategy expansion aimed at achieving 15% EBITDA margins.

The company's capital allocation strategy, highlighted by $70 million in share repurchases, reflects confidence in its financial stability and commitment to delivering value to shareholders. This is particularly relevant in the conglomerate industry, where diversified operations can lead to varying performance across segments.

Key Financial Metrics and Commentary

Griffon Corp's balance sheet shows cash and equivalents of $110.5 million and total debt outstanding of $1.44 billion, resulting in net debt of $1.33 billion. The leverage ratio improved slightly to 2.5x net debt to EBITDA. Capital expenditures were $13.5 million for the quarter, and the company's borrowing availability under the revolving credit facility was $465.5 million, subject to loan covenants.

"Fiscal 2024 is off to a good start with the first quarter highlighted by strong free cash flow, continued solid operating performance at HBP, and improved profitability at CPP," said Ronald J. Kramer, Chairman and Chief Executive Officer. "We are well positioned to meet our financial targets for the year."

The company's tax rates for the quarters ended December 31, 2023, and 2022 were 29.9% and 28.4%, respectively. Excluding items that affect comparability, the effective tax rates were 27.9% and 29.1% for the respective quarters.

Analysis and Outlook

While Griffon Corp faces challenges such as a slight revenue decline and increased labor and distribution costs, its strategic initiatives, including the expansion of the CPP global sourcing strategy, are set to enhance profitability and free cash flow. The company's strong free cash flow and share repurchase activity signal a robust financial position and a commitment to shareholder value.

Investors should note the company's focus on operational efficiency and cost management, which are crucial in the current economic climate. Griffon's diversified business model and strategic growth initiatives position it to navigate market uncertainties and capitalize on new opportunities.

For more detailed information and financial tables, please refer to the full 8-K filing.

Explore the complete 8-K earnings release (here) from Griffon Corp for further details.

This article first appeared on GuruFocus.