Guess? (GES) Rallies on Q2 Earnings Beat, Raised Profit View

Guess? Inc. GES reported robust second-quarter fiscal 2024 results, as both the top and bottom lines increased year over year and beat their respective Zacks Consensus Estimate.

The company gained strength from its international business. The Americas Retail business witnessed a sequential improvement due to improved customer conversion. Guess?’s robust revenue performance, solid gross margin results and efficient cost management drove better-than-anticipated results in most businesses.

Guess?’s focus on elevating brands, together with its strong global distribution and diversified business model, has been working well. The solid performance keeps management encouraged about the second half of the year. Management raised its operating margin and earnings per share (EPS) guidance for fiscal 2024 considerably.

Shares of the company jumped 18.5% during the after-market trading session on Aug 23.

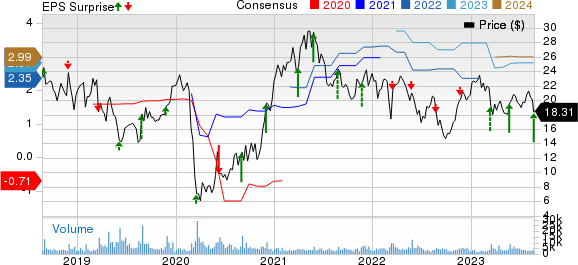

Guess?, Inc. Price, Consensus and EPS Surprise

Guess?, Inc. price-consensus-eps-surprise-chart | Guess?, Inc. Quote

Results in Detail

Guess? posted adjusted earnings of 72 cents per share, which soared 85% from 39 cents reported in the year-ago period. Earnings were positively impacted by share buybacks, partly negated by currency headwinds. The bottom line easily beat the Zacks Consensus Estimate of 39 cents per share.

Net revenues amounted to $664.5 million, surpassing the consensus mark of $639 million. The metric grew 3% from the figure reported in the year-ago quarter. On a constant-currency (cc) basis too, net revenues rose 3%. Revenues grew in Europe and Asia but declined in America.

The company’s gross margin expanded from 42.1% to 44.3% in the reported quarter. As a percentage of sales, SG&A expenses increased to 34.6% from 33.6% in the prior-year quarter’s level. We had expected a gross margin of 41% and SG&A expenses to be 35.3% of sales in the second quarter.

In the second quarter of fiscal 2024, adjusted earnings from operations came in at $65 million, up 17% year over year. The adjusted operating margin jumped 1.1% to 9.8% due to increased initial markups and a favorable business mix, partly offset by elevated expenses and currency woes.

Segment Performance

Revenues in the Americas Retail segment fell 8% year over year on a reported basis and at cc. Retail comp sales (including e-commerce) dropped 6% on a reported basis and at cc. The segment’s operating margin fell 4.1% to 9.1% in the quarter.

Americas Wholesale revenues fell 13% on a reported basis and 16% at cc. We had expected Americas Wholesales revenues to decline 14.3% on a reported basis. The segment’s operating margin jumped 2.5% to 25.3% in the quarter.

The Europe segment’s revenues jumped 9% on a reported basis and rose 8% at cc. Retail comp sales (including e-commerce) climbed 11% on a reported basis and at cc. The segmental operating margin was 12.9%, up 2.6% year over year.

Asia revenues advanced 19% on a reported basis and rose 22% at cc. Retail comp sales (including e-commerce) rose 2% on a reported basis, while the same increased 5% at cc.

Licensing revenues grew 13% on a reported basis and at cc. The segmental operating margin was 94.1% compared with 85.6% in the year-ago quarter.

Other Updates

This Zacks Rank #3 (Hold) company exited the quarter with cash and cash equivalents of $302.6 million and long-term debt and finance lease obligations of nearly $146 million. Stockholders’ equity was around $489 million. Net cash provided by operating activities for the six months ended Jul 29, 2023 was $47.3 million.

GES announced a quarterly dividend of 30 cents per share, payable on Sep 22, 2023, to shareholders on record as of Sep 6.

In April 2023, Guess? repurchased nearly 2.2 million shares, amounting to $42.8 million. Apart from this, the company did not make any other share buybacks during the six months ended Jul 29, 2023.

Guidance

For fiscal 2024, Guess? anticipates revenues to grow in the range of 2.5-4%.

The adjusted operating margin is likely to be 9-9.4%. The GAAP operating margin is likely to be 8.9-9.3%. Per the first-quarter earnings release, the adjusted operating margin was likely to be 8.2-8.8% in fiscal 2024, and the GAAP operating margin was projected at 8.1-8.7%.

Management expects adjusted EPS in the band of $2.88-$3.08 in fiscal 2024 compared with $2.74 recorded in fiscal 2023. On a GAAP basis, EPS is envisioned in the range of $2.22-$2.37 compared with $2.18 reported in fiscal 2023. Management had earlier forecasted adjusted EPS in the band of $2.60-$2.90 for fiscal 2024. On a GAAP basis, EPS was earlier envisioned in the range of $2.01-$2.25.

For the third quarter of fiscal 2024, management expects revenue growth of 2.5-4.5%. The company expects the adjusted operating margin and the GAAP operating margin in the range of 7.5-8.3%. On an adjusted basis, Guess? expects EPS in the band of 55-64 cents per share. On a GAAP basis, it expects EPS in the range of 46-53 cents for the third quarter of fiscal 2024.

GES stock has declined 2.6% in the past three months against the industry’s 3.7% growth.

Stocks to Consider

Here we have highlighted three better-ranked stocks.

Abercrombie & Fitch ANF, a specialty retailer, currently sports a Zacks Rank #1 (Strong Buy). ANF has a trailing four-quarter earnings surprise of 480.6%, on average. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Abercrombie & Fitch’s current financial-year EPS suggests growth of 736% from the year-ago reported figure.

Crocs, Inc. CROX, a casual lifestyle footwear and accessories company, carries a Zacks Rank #2 (Buy) at present. CROX has a trailing four-quarter earnings surprise of 19.9%, on average.

The Zacks Consensus Estimate for Crocs’ current financial-year revenues suggests growth of 12.9% from the year-ago reported figure.

lululemon athletica LULU, an athletic apparel, footwear and accessories company, currently carries a Zacks Rank #2. LULU has an EPS growth rate of 18.5% for three to five years.

The Zacks Consensus Estimate for lululemon’s current financial-year EPS suggests an increase of 18.5% from the year-ago reported figure. Lululemon has a trailing four-quarter earnings surprise of 9.9%, on average.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Abercrombie & Fitch Company (ANF) : Free Stock Analysis Report

Guess?, Inc. (GES) : Free Stock Analysis Report

lululemon athletica inc. (LULU) : Free Stock Analysis Report

Crocs, Inc. (CROX) : Free Stock Analysis Report