Hain Celestial (HAIN) Stock Plunges 38% in a Year: Here's Why

The Hain Celestial Group, Inc. HAIN has been grappling with several headwinds for a while now. Macroeconomic issues, including inflationary pressures, along with supply constraints and other headwinds have been weighing on the company’s performance. Sluggishness in the company’s North American unit is an added deterrent.

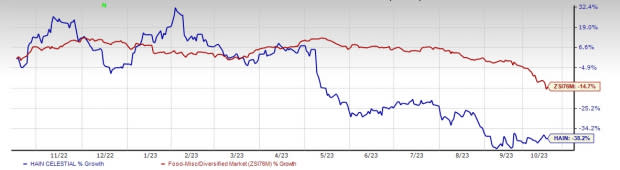

Driven by such limitations, shares of this Zacks Rank #4 (Sell) company have plunged 38.2% over the past year, wider than the industry’s 14.7% decline. The industry ranks in the bottom 29% of the Zacks classified industries.

Let’s Delve Deeper

Hain Celestial has been witnessing softness across its North America segment for a while now. During fourth-quarter fiscal 2023, net sales in the North America unit tumbled 5.1% from the year-ago fiscal quarter’s reported figure. After adjusting currency movements, divestitures and discontinued brands, adjusted net sales fell 4.3%. The decline was owing to lower sales in personal care and ParmCrisps, which was somewhat offset by increased sales in yogurt, tea and baby. Lower distribution and customer promotions, in relation to the ParmCrisps brand, hurt the sales.

Image Source: Zacks Investment Research

Overall, the company had posted soft fourth-quarter fiscal 2023 results, wherein the top line declined year over year. The top line dipped 2% from the year-ago fiscal quarter’s reported figure. After adjusting for foreign exchange, acquisitions, divestitures and discontinued brands, adjusted net sales slipped 1.5% from the year-ago fiscal quarter’s reported figure.

Going forward, management expects the investments, along with the refunding of the company’s incentive plan, to hurt the adjusted EBITDA by nearly $20 million. In its last earnings call, the company highlighted that it expects multiple headwinds to hurt the North American business in the first quarter of fiscal 2024. It is likely to witness industry-wide supply constraints with respect to its Earth's Best organic baby formula business. Also, the company has been optimizing promotional activity for Terra chips, leading to a near-term revenue headwind.

Additionally, there has been a timing shift in the personal care program. On the margin front, carryover inflation in the first quarter is likely to be higher than the rest of the fiscal year. For the quarter, adjusted net sales are projected to decrease by a low-single-digit percentage year over year and adjusted EBITDA is expected to be between $20 million and $21 million.

What Else?

Although the company is struggling with various headwinds, management has announced its Hain Reimagined strategy to drive profitable growth. This is a multi-year transformation plan created to boost sustainable growth in the long term and maximize shareholder returns. Management further stated that fiscal 2024 highlights the foundational year of the plan for simplifying the business, resetting the global operating model, initiating the Fuel Program, investing in jumpstart critical capabilities and starting to pivot to growth.

Although the aforesaid initiative makes us optimistic about the company over the long haul, it is best to remain cautious about the stock in the near term. A Momentum Score of F further adds to the weakness. For fiscal 2024, the Zacks Consensus Estimate for HAIN’s earnings per share (EPS) is currently pegged at 38 cents, indicating a decrease of 24% from the year-ago period’s figure.

Some Solid Staple Bets

Inter Parfums IPAR, which manufactures, markets and distributes a range of fragrances and fragrance-related products, currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Inter Parfums’ current financial-year sales indicates 19.7% growth from the year-ago reported figure. IPAR has a trailing four-quarter earnings surprise of 45.9% on average.

Helen of Troy HELE, a provider of several consumer products, currently has a Zacks Rank #2 (Buy). HELE’s expected earnings per share growth rate for three to five years is 8%.

The Zacks Consensus Estimate for Helen of Troy’s current fiscal-year sales suggests a decline of 2.9% from the year-ago reported numbers. HELE has a trailing four-quarter earnings surprise of 8.1%, on average.

Ingredion Incorporated INGR, a producer and distributor of sweeteners, nutrition ingredients and biomaterial solutions, currently carries a Zacks Rank of 2.

The Zacks Consensus Estimate for INGR’s current financial-year EPS is expected to rise 23.9% from the corresponding year-ago reported figure.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The Hain Celestial Group, Inc. (HAIN) : Free Stock Analysis Report

Helen of Troy Limited (HELE) : Free Stock Analysis Report

Ingredion Incorporated (INGR) : Free Stock Analysis Report

Inter Parfums, Inc. (IPAR) : Free Stock Analysis Report