Hanesbrands Has Upside Potential in Its Deleveraging Journey

Hanesbrands Inc. (NYSE:HBI) has suffered significant losses over the past several years, with its share price falling over 80% from its all-time high of $33.70 in June 2015 to around $4 at the time of writing. Recently, activist fund manager Barington Capital Group, recognizing the company's potential for improvement, sent a letter to Hanesbrands Chairman Ronald L. Nelson urging immediate and decisive actions. Indeed, the company appears to be considerably undervalued, presenting numerous opportunities to enhance shareholder value.

Innerwear and activewear apparel leader

The company is a prominent manufacturer in the basic innerwear and activewear apparel market, boasting notable brands such as Hanes, Champion, Maidenform, Bras N Things and Wonderbra. In 2022, Hanesbrands generated approximately 69% of its net sales in the United States, with Walmart (NYSE:WMT) being its largest customer, contributing 16% to total sales. The U.S. consumer-directed channel, which includes e-commerce websites, accounted for about 17% of the total sales in the same year.

Regarding business segments, innerwear emerged as the top revenue generator in 2022, bringing in $2.4 billion and comprising 39% of total sales. The international segment followed closely, recording $1.9 billion in sales or 30.7% of overall revenue. The activewear segment ranked third, contributing $1.6 billion, nearly 25% of the total revenue.

Gross margin and operating margin trends

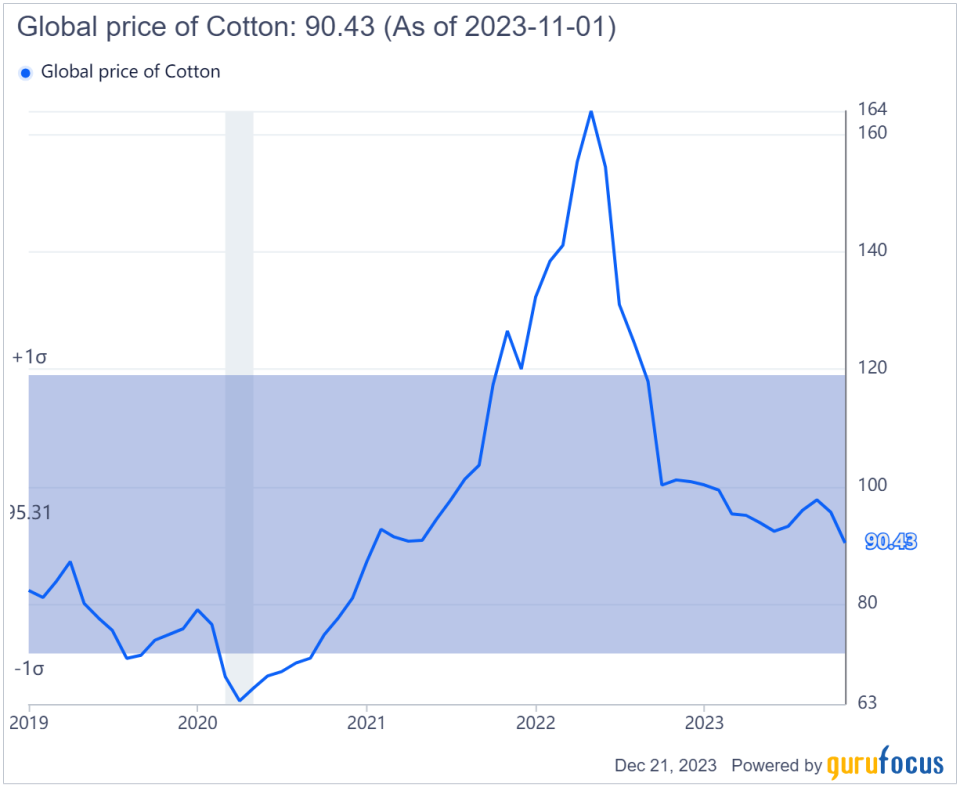

From 2012 to 2018, Hanesbrands experienced an upward trend in its gross margin, climbing from 31.3% to over 39%. However, there was a decline to 35.6% by 2022, further dipping to 32.70% in the first quarter of 2023. This decline can be attributed mainly to the rising costs of cotton, the company's primary raw material. Cotton prices escalated dramatically from 50 cents per pound in March 2020 to nearly $1.55 per pound in April 2021 due to the Covid-19 pandemic, resulting in higher costs of goods sold and a reduced gross margin. Fortunately, in the final quarter of 2022, cotton prices and freight rates began declining. Since then, cotton prices have stabilized between 76 cents and 90 cents per pound.

In its second-quarter earnings call, Hanesbrands' management noted a substantial decrease in cotton costs by nearly 40% year over year and an 80% reduction in ocean freight costs. These improvements were reflected in the gross margin, which increased to 35.5% in the third quarter. Given these trends, further enhancement in gross margin is anticipated in the next several quarters.

Concurrently, the company's operating margin has been decreasing. After peaking at 13.2% in 2019, it gradually fell to 8.3% in 2022. A major contributor to this decline is the significant increase in selling, general and administrative expenses, which rose nearly 87% from $911 million in 2012 to over $1.7 billion in 2022. These expenses, which are within management's control, suggest potential for improved operational efficiency and cost reduction. In its letter to the company, Barington Capital said it expects the company to cut selling, general and administrative expenses by a minimum of $300 million annually and allocate the savings toward reducing its debt.

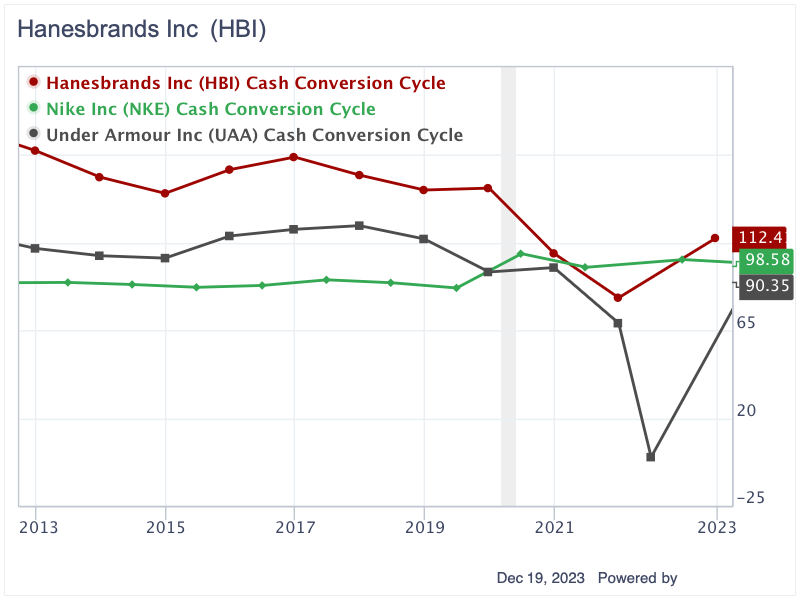

Inefficient operations with high cash conversion cycle and days inventory

Hanesbrands has experienced an improvement in its cash conversion cycle, which is the metric used to gauge the duration from when a company invests in inventory and operating resources to when it collects cash from sales. Over the past decade, the company has seen its CCC decrease from 143.6 days in 2013 to approximately 82 days in 2021, though it did rise to 112.4 days in 2022. Compared to other peers like Nike (NYSE:NKE) and Under Armour (NYSE:UAA), Hanesbrands has not achieved the same efficiency level. In 2022, Nike reported a CCC of 98.6 days, while Under Armour outperformed both, recording the lowest CCC at 90.35 days.

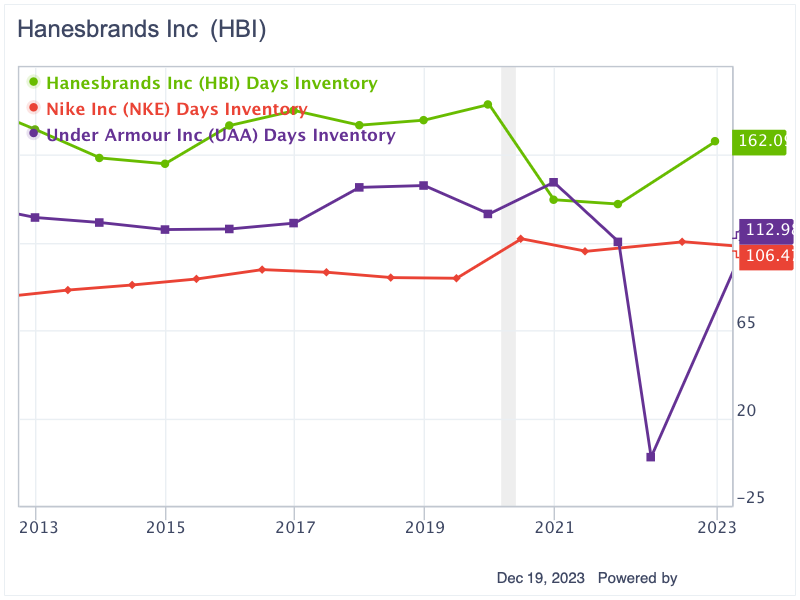

The elevated cash conversion cycle of Hanesbrands can be largely attributed to its low inventory turnover, indicated by the high number of days inventory remains before being sold. Over the past decade, Hanesbrands' inventory days have varied widely between 130 and 181 days and in 2022, the company's inventory days stood at 162. In contrast, both Nike and Under Armour have managed to maintain lower inventory days of 106 days and 110 days, reflecting more efficient inventory management.

High leverage and staggered debt maturities

Hanesbrands has been operating with a substantial amount of leverage. As of the third quarter of 2023, the company reported a modest $274 million in stockholders' equity compared to a hefty $3.31 billion in long-term debt, with an additional $59 million of debt due within the next year. This has resulted in a record-high debt-to-equity ratio of 10.80.

However, two positive indicators offer some reassurance. First, the interest coverage ratio was a manageable 3.3 times in 2022. Second, the debt maturities are spread out until 2031, with only $200 million due in May 2024 and $900 million in May 2026. This staggered schedule allows Hanesbrands to reduce costs and invest those savings to lower its debt levels over time.

Estimated significant undervaluation

For 2023, Hanesbrands is projected to generate sales ranging from $6.05 billion to $6.2 billion and an operating profit between $446 million and $496 million. The diluted earnings per share are anticipated to be between 14 cents and 25 cents. If Hanesbrands achieves an Ebitda margin that aligns with its 10-year average of 12%, this would translate to an Ebitda of approximately $732 million, assuming the sales are at the estimated midpoint of $6.1 billion. With the company's five-year average Ebitda multiple at around 20 times, an Ebitda of $732 million would imply a total enterprise value of approximately $14.64 billion, notably three times the present market valuation.

Conclusion

Despite its recent challenges and operational inefficiencies, Hanesbrands shows potential for a promising turnaround. The company's strong brand portfolio, decreasing costs and strategic steps toward cost optimization indicate improving profitability. Additionally, its current significant undervaluation in the market presents an attractive investment opportunity for those willing to bet on its potential for recovery and long-term growth.

This article first appeared on GuruFocus.