Helen of Troy (HELE) Q1 Earnings Top Estimates, Decline Y/Y

Helen of Troy Limited HELE posted first-quarter fiscal 2024 results, with the top and the bottom line declining year over year but beating the Zacks Consensus Estimate. Results were hurt by ongoing pressure on some categories due to reduced consumer demand and changes in buying patterns. That said, strength in several Leadership Brands and greater International sales were an upside.

Quarter in Detail

Adjusted earnings of $1.94 per share beat the Zacks Consensus Estimate of $1.62. However, the bottom line declined 19.5% year over year. The metric was mainly hurt by reduced adjusted operating income in Home & Outdoor and higher interest expenses.

Consolidated net sales of $474.7 million surpassed the Zacks Consensus Estimate of $463.3 million. However, the metric fell 6.6% from the year-ago quarter’s levels. The downside was a result of softness in the organic business to the tune of 7.7%, partly compensated by the buyout contributions from Curlsmith ($6.1 million).

The organic business was hurt by lower sales in hair appliance, seasonal fan, air filtration, humidification, insulated beverage and houseware categories. The downside was due to SKU rationalization efforts, lower consumer demand, shifts in consumer spending patterns and less orders from retail customers among other reasons. Nevertheless, higher sales of thermometry and prestige market hair care products, growth in online channel sales, solid consumer demand for travel-related products and increased international sales were positives.

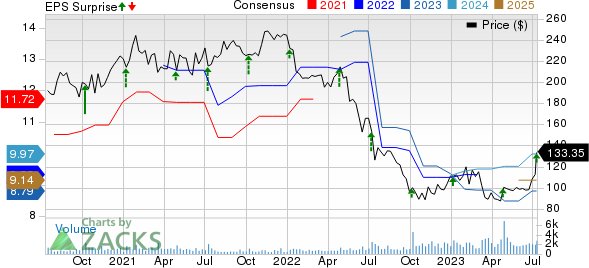

Helen of Troy Limited Price, Consensus and EPS Surprise

Helen of Troy Limited price-consensus-eps-surprise-chart | Helen of Troy Limited Quote

The consolidated gross profit margin expanded 380 basis points (bps) to 45.4% from 41.6% reported in the year-ago quarter. The upside can mainly be attributed to positive comparative impact of EPA compliance costs, favorable product mix for Beauty & Wellness and customer mix in the Home & Outdoor category. Also, reduced inbound freight costs contributed to the gain. However, increased inventory obsolescence expense hurt the metric.

The consolidated operating income stood at $40.6 million, up from the $33.9 million reported in the year-ago quarter. The consolidated operating margin came in at 8.6%, up from 6.7% reported in the year-ago quarter. We had expected operating margin to expand 100 bps to 7.7%.

The increase in consolidated operating margin was led by lower share-based compensation costs, positive product mix within Beauty & Wellness category and favorable customer mix in the Home & Outdoor business. Reduced inbound freight costs also contributed to the upside. Yet, these factors were somewhat offset by restructuring charges, increased inventory obsolescence costs, higher annual incentive compensation expense and greater outbound freight costs among others.

Segmental Performance

Net sales in the Home & Outdoor segment fell 7.3% to $217.1 million, as organic business fell 7.2%. The downside was mainly due to softness in insulated beverage category and reduced houseware sales. That said, higher online channel sales offered some respite.

Net sales in the Home & Outdoor segment dropped more than our expected decline of 3.9% to $225.1 million.

Net sales in the Beauty & Wellness segment declined 5.9% to $257.5 million due to the organic business’ decline of 8.1%, stemming from the soft sales of hair appliances, seasonal fans and air filtration and humidification products. In addition, drab consumer demand, change in consumer spending patterns and lower orders from retail customers were a downside.

We had expected Beauty & Wellness net sales decline of 13.2% to $237.7 million.

Image Source: Zacks Investment Research

Other Details

Helen of Troy ended the quarter with cash and cash equivalents of $38.9 million and total short-and long-term debt of $837.2 million. Net cash provided by operating activities for three months ended May 31, 2023 was $121.1 million.

Restructuring Plan

In the second quarter of fiscal 2023, Helen of Troy focused on developing a global restructuring plan, Project Pegasus. The plan aims to expand operating margins via initiatives designed to improve efficiency and reduce costs.

Project Pegasus includes efforts to optimize the company’s brand portfolio, streamline and simplify the organization, grow the cost of goods-saving projects and improve the efficiency of the supply-chain network. The project aims to streamline indirect spending and improve cash flow and working capital. As part of Project Pegasus, management expects to achieve annualized pre-tax operating profit improvements of $75-85 million, to be substantially generated by fiscal 2026-end.

During the fourth quarter of fiscal 2023, Helen of Troy undertook changes in the structure of its organization, as part of the global restructuring plan. The company has two reportable units — Home & Outdoor and Beauty & Wellness.

Fiscal 2024 Guidance

Helen of Troy expects fiscal 2024 consolidated net revenues in the range of $1.965-$2.015 billion, reflecting a decline of 5.2-2.8%. The year-over-year decline includes the removal of Bed, Bath & Beyond revenues and the reduction from the Pegasus SKU rationalization initiative. The top-line view reflects a continued slower economy and uncertainty in spending patterns mainly for discretionary categories. In addition, the company is seeing reduction of trade inventory on a sequential basis.

The company’s fiscal 2024 net sales view assumes Home & Outdoor segment net sales decline of 1.7% to growth of 1%. The view also considers Beauty & Wellness net sales decline of 5.8-8%.

HELE expects adjusted earnings per share (EPS) in the range of $8.50-$9.00. This indicates a consolidated adjusted EPS decline of 4.8-10.1%. The outlook reflects additional year-over-year expenses related to the restoration of annual incentive compensation expenses and increased interest and depreciation expenses. Management anticipates consolidated adjusted EBITDA of $338-$348 million, indicating growth of 3.2-6.3% for fiscal 2024.

The company envisions net sales decline of 6-8% in the second quarter of fiscal 2024. Management anticipates a decline in adjusted EPS of 20-30% in the first half of fiscal 2024 with almost offsetting growth in the second half of the year.

Shares of this Zacks Rank #2 (Buy) company have gained 52.6% in the past three months against the industry’s 14.3% decline.

Other Solid Bets

Here we have highlighted other three top-ranked stocks, namely TreeHouse Foods, Inc. THS, Lamb Weston Holdings LW and Celsius Holdings CELH.

TreeHouse Foods, a manufacturer of packaged foods and beverages, currently sports a Zacks Rank #1 (Strong Buy). THS has a trailing four-quarter earnings surprise of 49.3%, on average. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for TreeHouse Foods’ current financial-year sales suggests decline of 12.4%, from the year-ago reported numbers.

Lamb Weston, a leading supplier of frozen potato, sweet potato, appetizer and vegetable products to restaurants and retailers worldwide, currently carries a Zacks Rank #2 (Buy). LW has a trailing four-quarter earnings surprise of 47.6%, on average.

The Zacks Consensus Estimate for Lamb Weston’s current financial-year sales and earnings suggests growth of 29.6% and 117.3%, respectively, from the year-ago reported numbers. The expected EPS growth rate for three to five years is 42.7%.

Celsius Holdings, which offers functional drinks and liquid supplements, currently carries a Zacks Rank #2. CELH delivered an earnings surprise of 81.8% in the last reported quarter.

The Zacks Consensus Estimate for Celsius Holdings’ current fiscal-year sales and earnings suggests growth of 69.6% and 154.4%, respectively, from the year-ago reported numbers.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

TreeHouse Foods, Inc. (THS) : Free Stock Analysis Report

Helen of Troy Limited (HELE) : Free Stock Analysis Report

Lamb Weston (LW) : Free Stock Analysis Report

Celsius Holdings Inc. (CELH) : Free Stock Analysis Report