Helix Energy Solutions Group (HLX): Significantly Overvalued or Just a Misunderstanding?

Helix Energy Solutions Group Inc (NYSE:HLX) experienced a daily gain of 4.09%, with a 3-month gain of 63.82%. Despite a Loss Per Share of 0.08, the question remains: is the stock significantly overvalued? In this article, we will delve into the valuation analysis of Helix Energy Solutions Group, providing valuable insights for potential investors.

A Brief Introduction to Helix Energy Solutions Group Inc (NYSE:HLX)

Helix Energy Solutions Group, an offshore energy services company, offers specialty services to the offshore energy industry, focusing on well intervention and robotics operations. The company primarily operates in deepwater regions such as the Gulf of Mexico, Brazil, the North Sea, Asia Pacific, and West Africa. Despite its current stock price of $11.15 per share, the fair value (GF Value) of the company is estimated at $5.9, suggesting a potential overvaluation.

Understanding the GF Value

The GF Value is a unique measure of a stock's intrinsic value, calculated based on historical trading multiples, a GuruFocus adjustment factor, and future business performance estimates. The GF Value Line provides an overview of the fair value at which the stock should ideally be traded. If the stock price is significantly above the GF Value Line, it is considered overvalued and its future return is likely to be poor. Conversely, if it is significantly below the GF Value Line, its future return will likely be higher.

Currently, the stock of Helix Energy Solutions Group appears to be significantly overvalued according to the GuruFocus Value estimation. At its current price of $11.15 per share and a market cap of $1.70 billion, the future return of Helix Energy Solutions Group's stock is likely to be much lower than its future business growth.

Link: These companies may deliever higher future returns at reduced risk.

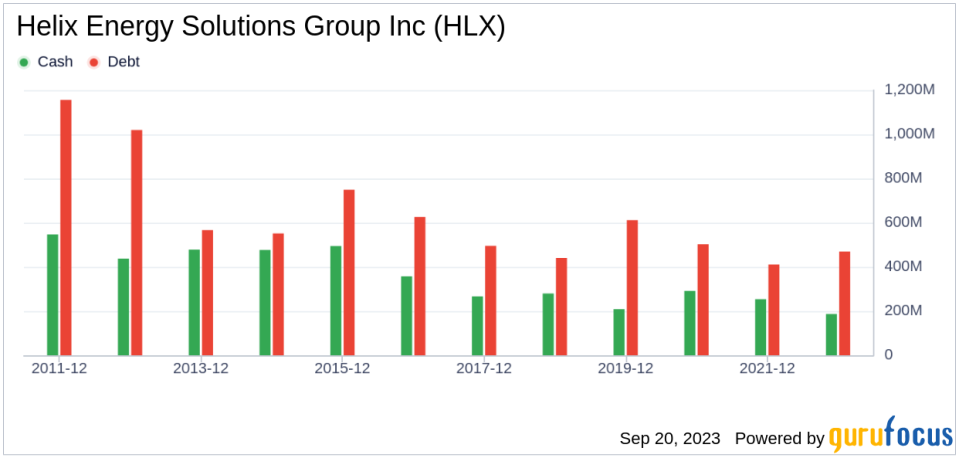

Financial Strength of Helix Energy Solutions Group

Investing in companies with low financial strength could result in permanent capital loss. Therefore, it's crucial to review a company's financial strength before deciding to buy shares. Helix Energy Solutions Group has a cash-to-debt ratio of 0.41, ranking worse than 54.32% of 1031 companies in the Oil & Gas industry. Based on this, GuruFocus ranks Helix Energy Solutions Group's financial strength as 6 out of 10, suggesting a fair balance sheet.

Profitability and Growth of Helix Energy Solutions Group

Investing in profitable companies, especially those with consistent profitability over the long term, poses less risk. Helix Energy Solutions Group has been profitable 6 over the past 10 years. Over the past twelve months, the company had a revenue of $1.10 billion and a Loss Per Share of $0.08. Its operating margin is 4.57%, ranking worse than 60.65% of 981 companies in the Oil & Gas industry. Overall, GuruFocus ranks the profitability of Helix Energy Solutions Group at 5 out of 10, indicating fair profitability.

Growth is probably the most important factor in the valuation of a company. The faster a company is growing, the more likely it is to be creating value for shareholders, especially if the growth is profitable. The 3-year average annual revenue growth rate of Helix Energy Solutions Group is 4.7%, which ranks worse than 61.28% of 860 companies in the Oil & Gas industry. The 3-year average EBITDA growth rate is -22.9%, ranking worse than 87.44% of 828 companies in the Oil & Gas industry.

ROIC vs WACC

Another way to look at the profitability of a company is to compare its return on invested capital and the weighted cost of capital. Return on invested capital (ROIC) measures how well a company generates cash flow relative to the capital it has invested in its business. The weighted average cost of capital (WACC) is the rate that a company is expected to pay on average to all its security holders to finance its assets. For the past 12 months, Helix Energy Solutions Group's return on invested capital is 9.54, and its cost of capital is 14.11.

Conclusion

In summary, the stock of Helix Energy Solutions Group appears to be significantly overvalued. The company's financial condition is fair, and its profitability is also fair. However, its growth ranks worse than 87.44% of 828 companies in the Oil & Gas industry. To learn more about Helix Energy Solutions Group stock, you can check out its 30-Year Financials here.

To find out the high-quality companies that may deliver above-average returns, please check out GuruFocus High Quality Low Capex Screener.

This article first appeared on GuruFocus.