Here's How The TJX Companies (TJX) Is Placed Ahead of 2024

The TJX Companies, Inc. TJX has been reaping the benefits of its off-price business model. Strategic store locations, impressive brands and fashion products and efficient supply-chain management have been working well for the company amid elevated cost concerns.

Markedly, this Zacks Rank #3 (Hold) company has been benefiting from its solid store and e-commerce growth efforts. These upsides are likely to continue working well for the company.

The Zacks Consensus Estimate for the current and next fiscal year earnings per share (EPS) has increased from $3.71 to $3.75 and from $4.04 to $4.08, respectively, over the past 60 days.

Image Source: Zacks Investment Research

Sales Picture Looks Bright

The TJX Companies has been seeing strength in the Marmaxx segment. In the third quarter of fiscal 2024, net sales came in at $8,107 million, up 9% year over year in the Marmaxx (U.S.) division. U.S. comparable store sales grew 7% in Marmaxx, buoyed by solid apparel and home categories’ sales. Customer traffic remained the key driver behind comparable store sales growth. We believe that strength in Marmaxx is likely to continue aiding the company’s overall sales.

The TJX Companies has been witnessing solid momentum in its HomeGoods (U.S.) division, driven by a rise in customer traffic. In the HomeGoods (U.S.) division, the company’s net sales amounted to $2,208 million in the fiscal third quarter, up 13% from the figure reported in the year-ago quarter. In the quarter, U.S. comparable store sales rose 9% in the HomeGoods category. In addition, the recovery of the TJX Canada and TJX International segments with comparable store sales growth of 3% and 1%, respectively, has been a tailwind.

Overall comparable store sales increased by 6% in the third quarter of fiscal 2024, witnessing an increase in U.S. customer traffic. For fiscal 2024, management expects overall comparable store sales growth of 4-5%, excluding sales from the 53rd week. It expects consolidated sales in the band of $53.7-$53.9 billion, suggesting 7.6-8% year-over-year growth. For the fourth quarter, comparable store sales are expected to rise 3-4%, and consolidated sales are anticipated to increase approximately 10% to $15.9-$16.1 billion.

The TJX Companies has been rapidly expanding its footprint in the United States, Europe, Canada and Australia. Further, with an increasing number of consumers resorting to online shopping, The TJX Companies has undertaken several initiatives to boost online sales and strengthen its e-commerce business.

Cost Woes to be Countered?

The TJX Companies has been dealing with the adverse impacts of the high cost of sales and operating expenses. In the third quarter of fiscal 2024, the company's cost of sales increased by 6%, and selling, general and administrative expenses rose by 18%. TJX has also been witnessing incremental wage and payroll costs along with higher incentive accruals. It expects these cost headwinds to remain hurdles in fiscal 2024.

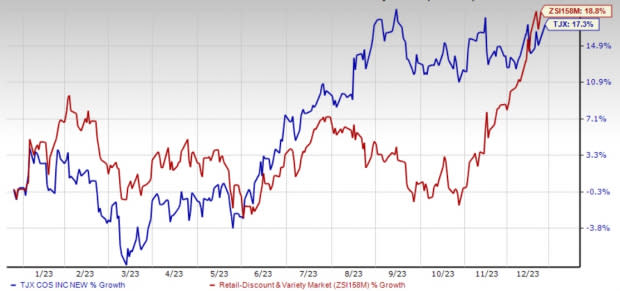

However, strength in the abovementioned factors is likely to drive sales and help the company counter cost-related challenges, keeping it well-positioned for the new year. Shares of TJX have rallied 17.3% in a year compared with the industry’s growth of 18.8%.

3 Impressive Picks

Abercrombie & Fitch ANF, a specialty retailer, currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here

The Zacks Consensus Estimate for Abercrombie & Fitch’s current financial-year sales suggests growth of 13.3% from the year-ago reported number. ANF’s bottom line has outpaced the Zacks Consensus Estimate by a wide margin in the trailing four quarters, on average.

The Gap, Inc. GPS, a fashion retailer of apparel and accessories, currently sports a Zacks Rank #1. GPS has a trailing four-quarter earnings surprise of 137.9%, on average.

The Zacks Consensus Estimate for Gap’s current financial year EPS indicates growth of 387.5% year over year.

American Eagle Outfitters AEO, a retailer of casual apparel, accessories and footwear, currently has a Zacks Rank #2 (Buy). AEO delivered a trailing four-quarter average earnings surprise of 23%.

The Zacks Consensus Estimate for American Eagle Outfitters’ current financial year sales and EPS implies growth of 4% and 39.2%, respectively, from that reported a year ago.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The TJX Companies, Inc. (TJX) : Free Stock Analysis Report

Abercrombie & Fitch Company (ANF) : Free Stock Analysis Report

American Eagle Outfitters, Inc. (AEO) : Free Stock Analysis Report

The Gap, Inc. (GPS) : Free Stock Analysis Report