Here's What We Like About Weyco Group's (NASDAQ:WEYS) Upcoming Dividend

Weyco Group, Inc. (NASDAQ:WEYS) stock is about to trade ex-dividend in four days. The ex-dividend date is one business day before a company's record date, which is the date on which the company determines which shareholders are entitled to receive a dividend. The ex-dividend date is important because any transaction on a stock needs to have been settled before the record date in order to be eligible for a dividend. Therefore, if you purchase Weyco Group's shares on or after the 24th of November, you won't be eligible to receive the dividend, when it is paid on the 2nd of January.

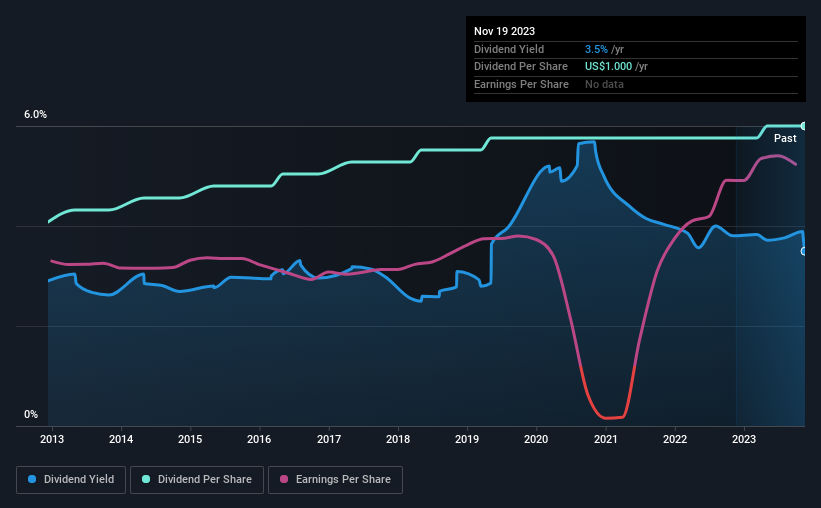

The company's upcoming dividend is US$0.25 a share, following on from the last 12 months, when the company distributed a total of US$1.00 per share to shareholders. Last year's total dividend payments show that Weyco Group has a trailing yield of 3.5% on the current share price of $28.6. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. So we need to check whether the dividend payments are covered, and if earnings are growing.

Check out our latest analysis for Weyco Group

Dividends are typically paid from company earnings. If a company pays more in dividends than it earned in profit, then the dividend could be unsustainable. Weyco Group paid out a comfortable 29% of its profit last year. Yet cash flow is typically more important than profit for assessing dividend sustainability, so we should always check if the company generated enough cash to afford its dividend. Luckily it paid out just 13% of its free cash flow last year.

It's positive to see that Weyco Group's dividend is covered by both profits and cash flow, since this is generally a sign that the dividend is sustainable, and a lower payout ratio usually suggests a greater margin of safety before the dividend gets cut.

Click here to see how much of its profit Weyco Group paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Stocks in companies that generate sustainable earnings growth often make the best dividend prospects, as it is easier to lift the dividend when earnings are rising. If business enters a downturn and the dividend is cut, the company could see its value fall precipitously. For this reason, we're glad to see Weyco Group's earnings per share have risen 16% per annum over the last five years. The company has managed to grow earnings at a rapid rate, while reinvesting most of the profits within the business. Fast-growing businesses that are reinvesting heavily are enticing from a dividend perspective, especially since they can often increase the payout ratio later.

The main way most investors will assess a company's dividend prospects is by checking the historical rate of dividend growth. Weyco Group has delivered an average of 3.9% per year annual increase in its dividend, based on the past 10 years of dividend payments. It's good to see both earnings and the dividend have improved - although the former has been rising much quicker than the latter, possibly due to the company reinvesting more of its profits in growth.

To Sum It Up

Is Weyco Group an attractive dividend stock, or better left on the shelf? We love that Weyco Group is growing earnings per share while simultaneously paying out a low percentage of both its earnings and cash flow. These characteristics suggest the company is reinvesting in growing its business, while the conservative payout ratio also implies a reduced risk of the dividend being cut in the future. It's a promising combination that should mark this company worthy of closer attention.

While it's tempting to invest in Weyco Group for the dividends alone, you should always be mindful of the risks involved. For example - Weyco Group has 1 warning sign we think you should be aware of.

Generally, we wouldn't recommend just buying the first dividend stock you see. Here's a curated list of interesting stocks that are strong dividend payers.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.