Here's Why Should You Add Methanex (MEOH) to Your Portfolio

Methanex Corporation MEOH recorded a 4.6% increase in its stock value in the last three months, primarily driven by its forecast-topping earnings performance on higher methanol demand in the third quarter.

The stock offers an attractive investment opportunity with strong growth prospects. MEOH carries a Zacks Rank #2 (Buy).

Positive Earnings Surprise History

In the third quarter, Methanex exceeded expectations by reporting earnings of 2 cents per share, surpassing the Zacks Consensus Estimate of a loss of 8 cents. The company exceeded bottom-line forecasts in each of the past four quarters, showcasing an impressive earnings surprise of 53.4% on average.

Healthy Growth Potential

The Zacks Consensus Estimate for 2023 earnings is currently pegged at $2. The consensus estimate for current-year earnings has been revised upward by 7% in the past 60 days.

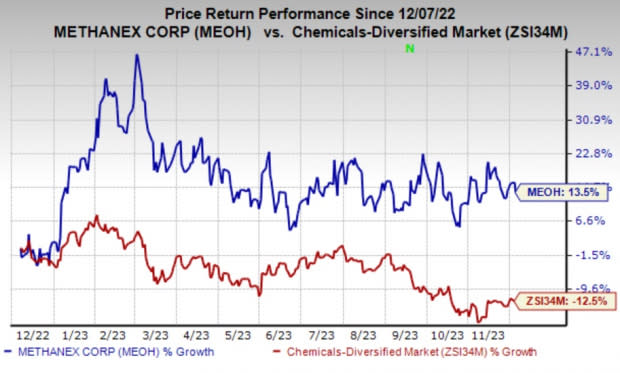

An Outperformer

Shares of MEOH are up 13.5% in a year compared with the industry’s decline of 12.5% in the same period.

Image Source: Zacks Investment Research

Higher Methanol Demand, Geismar 3 to Aid MEOH

In the third quarter, Methanex experienced a rise in methanol demand, attributing it to an improved market environment and increased activity in specific sectors. The company particularly witnessed a robust demand upswing in China, driven by a growing appetite for fuel applications. Methanol-to-Olefins (MTO) exhibited improved demand dynamics, with several MTO plants commencing operations during the quarter.

A key highlight for Methanex is the commendable progress made on the Geismar 3 project, which aligns seamlessly with the company's outlined plan. This strategic initiative will augment Methanex's asset portfolio and future cash generation and deliver long-term value to shareholders. The effective management of potential risks is a noteworthy aspect, with major equipment already on-site, mitigating concerns related to supply chain disruptions and inflation.

The projected capital expenditure for the Geismar 3 project is estimated to be $1.25-$1.3 billion, with additional financial outlays of $140-$190 million already secured through available cash reserves. Methanex expresses confidence in its robust liquidity position and anticipates utilizing its strong cash flow generation to fund the Geismar 3 project, expecting timely completion within budget.

In terms of shareholders’ value, Methanex returned $12 million during the third quarter through regular dividends, showcasing the company's commitment to delivering returns to investors. Closing the quarter with $529 million in cash or approximately $510 million — excluding non-controlling interests — and with an undrawn $300-million revolving credit facility, MEOH maintains financial flexibility to navigate evolving market conditions.

The company's proactive approach to capitalizing on rising methanol demand and the strategic advancement of the Geismar 3 project positions it favorably for sustained growth.

Methanex Corporation Price and Consensus

Methanex Corporation price-consensus-chart | Methanex Corporation Quote

Zacks Rank & Other Key Picks

Some other top-ranked stocks in the Basic Materials space are Axalta Coating Systems Ltd. AXTA, sporting a Zacks Rank #1 (Strong Buy), and The Andersons Inc. ANDE and Alamos Gold Inc. AGI, each carrying a Zacks Rank #2. You can see the complete list of today’s Zacks #1 Rank stocks here.

The consensus estimate for AXTA’s current-year earnings is pegged at $1.58, indicating year-over-year growth of 6.8%. AXTA beat the Zacks Consensus Estimate in three of the last four quarters and missed one, with the average earnings surprise being 6.7%. The company’s shares have increased 23.1% in the past year.

The Zacks Consensus Estimate for ANDE’s current-year earnings has been revised upward by 5.1% in the past 60 days. Andersons beat the Zacks Consensus Estimate in each of the last four quarters. It delivered a trailing four-quarter earnings surprise of 32.8% on average. ANDE’s shares have rallied around 48.9% in a year.

The consensus estimate for Alamos’ current fiscal year earnings is pegged at 53 cents, indicating year-over-year growth of 89.3%. AGI beat the Zacks Consensus Estimate in all of the last four quarters, with the average earnings surprise being 25.6%. The company’s shares have surged 43.1% in the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The Andersons, Inc. (ANDE) : Free Stock Analysis Report

Methanex Corporation (MEOH) : Free Stock Analysis Report

Alamos Gold Inc. (AGI) : Free Stock Analysis Report

Axalta Coating Systems Ltd. (AXTA) : Free Stock Analysis Report