Here's Why You Should Add Primerica (PRI) to Your Portfolio

Primerica Inc.’s PRI distribution channel, strong agent force, market presence, positive premium outlook and solid capital position make it worth adding to one’s portfolio.

Earnings of this second-largest issuer of term-life insurance coverage in North America have risen 14.4% over the last five years, outperforming the industry’s average of 2.6%.

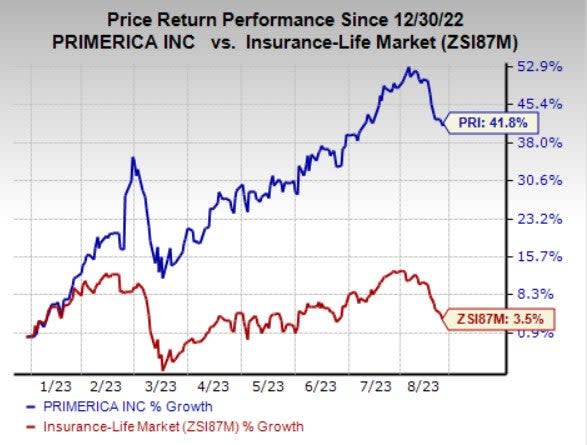

Zacks Rank & Price Performance

Primerica currently carries a Zacks Rank #2 (Buy). Year to date, the stock has gained 41.8% compared with the industry’s growth of 3.5%.

Image Source: Zacks Investment Research

Return on Equity

Return on equity (ROE), a profitability measure to identify how efficiently a company is utilizing its shareholders’ funds, has been improving over the last several years. PRI’s trailing 12-month ROE of 28.5% is better than the industry’s average of 13.1%.

Rising Estimates

The Zacks Consensus Estimate for PRI’s 2023 earnings is pegged at $15.63 per share, indicating a 36.6% increase on 3.1% higher revenues of $2.8 billion.

The consensus estimate for 2024 earnings is pegged at $17.37, indicating an increase of 11.2% on 4.7% higher revenues of $2.9 billion.

The company beat earnings estimates in each of the last four quarters, the average surprise being 6.5%.

Business Tailwinds

Primerica should gain from strong demand for protection products that drive sales growth and policy persistence. A strong business model makes it well-poised to cater to the middle market's increased demand for financial security. Thus, Primerica envisions being a successful senior health business while continuing to enhance its shareholders’ value.

The insurer stays focused on increasing the size of the life license sales force through continued recruiting and licensing. PRI anticipates a 3-4%% rise in sales force size in 2023. Licensed representatives play a pivotal role in driving operational results for PRI.

PRI expects Term Life insurance issued policy growth in the range of 4-6% in 2023. The company noted that new rate classes through new products should accelerate growth, and inflationary pressure will weigh on the upside. The company expects adjusted direct premiums to grow 6% in 2023.

In Investment and Savings Products, the insurer’s second-quarter 2023 sales declined 4% year over year. Inflationary pressure and attractive alternatives to the equity market may hamper sales and client asset values.

Life insurers are direct beneficiaries of an improving interest-rate environment. The Fed raised interest rates seven times in 2022 and twice so far in 2023, with more on the horizon this year. The Federal Open Market Committee indicated its intention to carry on with two more rate hikes in 2023. Thus, an improving interest rate environment should aid net investment income. The company expects net investment income of $34 million in each quarter for the remainder of 2023.

While the insurer has solid liquidity, Primerica has been strengthening its balance sheet by improving its leverage ratio. PRI scores strongly with credit rating agencies. The company repurchased $110.8 million worth of shares and paid dividends worth $24 million in the second quarter of 2023.

However, the company is exposed to foreign currency risks. Its Canadian operations’ functional currency is the Canadian dollar, and PRI translates all the balance sheet and income statement amounts to U.S. dollars. An increase or a decrease in U.S. dollars per Canadian dollar exchange rate should affect the consolidated results positively and negatively, respectively. The company’s rising expenses are also a concern. PRI expects insurance and other operating expenses to rise 5% in 2023.

Other Key Picks

Some other top-ranked stocks from the broader Finance space are Employers Holdings, Inc. EIG, Trupanion, Inc. TRUP and Aflac Incorporated AFL. Each of these companies presently carries a Zacks Rank #2. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The consensus mark for Employers Holdings’ current-year earnings indicates a 10.2% year-over-year increase. Furthermore, the consensus estimate for EIG’s revenues in 2023 suggests 20.5% year-over-year growth.

The Zacks Consensus Estimate for Trupanion’s current-year earnings has improved 9.2% in the past 30 days. Also, the consensus mark for TRUP’s revenues in 2023 suggests 19.2% year-over-year growth.

The consensus mark for Aflac’s current-year earnings indicates a 12.2% year-over-year increase. The Zacks Consensus Estimate for AFL’s current-year earnings has improved 3.3% in the past 30 days.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Aflac Incorporated (AFL) : Free Stock Analysis Report

Primerica, Inc. (PRI) : Free Stock Analysis Report

Employers Holdings Inc (EIG) : Free Stock Analysis Report

Trupanion, Inc. (TRUP) : Free Stock Analysis Report