Here's Why Boot Barn Holdings (BOOT) Is a Smart Choice

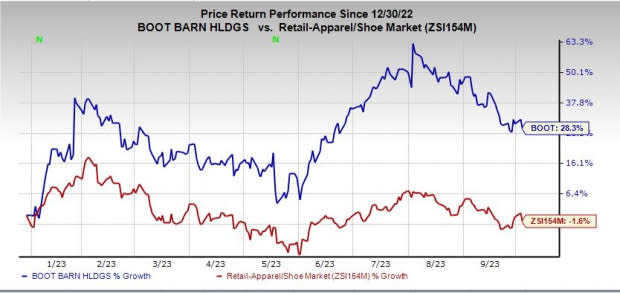

Boot Barn Holdings, Inc. BOOT has not only navigated market challenges but also showcased remarkable resilience and growth potential. Based in Irvine, CA, the company has defied industry trends, with its stock surging an impressive 28.3% year to date, a stark contrast to the industry's decline of 1.6%.

The cornerstone of Boot Barn Holdings’ success lies in its effective merchandising strategies, robust omnichannel capabilities, meticulous expense management and customer-centric approach. These, coupled with a strategic expansion of its store base, have enabled this Zacks Rank #2 (Buy) company to gain market share and fortify its position in the industry.

Let’s Delve Deep

Boot Barn Holdings has emerged as an attractive investment prospect, driven by its robust fundamental drivers and strategic initiatives. In the first quarter of fiscal 2024, BOOT demonstrated its resilience with a 4.9% increase in total sales, primarily driven by the successful integration of new stores.

The company's aggressive expansion plan, evidenced by the opening of 86 stores in the last two years, underscores its market penetration strategy. With 16 new stores added in the first quarter, Boot Barn Holdings concluded the quarter with 361 stores spanning 44 states. The company remains confident about attaining its ambitious long-term goal of establishing 900 or more stores across the United States.

Moreover, BOOT's focus on customer segmentation has yielded impressive results, with 23% growth in its active member base. The introduction of artificial intelligence in both in-store and online interactions exemplifies the company’s commitment to enhancing customer experience, fostering brand loyalty and consequently driving sales.

Image Source: Zacks Investment Research

A pivotal aspect of Boot Barn Holdings’ success lies in its exclusive brand penetration, which increased more than 600 basis points to 38% of sales in the last reported quarter. This strategic move not only enriches product offerings but also significantly boosts the company's margin profile. Coupled with efficient expense control and an 80-basis point expansion in the product margin, BOOT surpassed earnings per share expectations in the first quarter.

Management now anticipates fiscal 2024 total sales to hit the upper end of the guidance range, ranging from $1.715 billion to $1.748 billion, representing growth of 3.5% to 5.5% over the prior year. Gross profit is projected to land between $629.7 million and $645.7 million, or approximately 36.7% to 36.9% of sales, showcasing an estimated 160-basis point increase in the merchandise margin.

Wrapping Up

With an expanding store network, a growing and loyal customer base and a focus on high-margin exclusive brands, Boot Barn Holdings stands poised for sustained growth. Investors seeking a promising opportunity in the retail market should consider BOOT as a stock poised to deliver substantial returns, underpinned by its strategic initiatives and robust financial fundamentals.

3 More Stocks Looking Hot

Here, we have highlighted some other top-ranked stocks, namely Urban Outfitters URBN, American Eagle Outfitters AEO and Abercrombie & Fitch ANF.

Urban Outfitters, the leading lifestyle product and services company, sports a Zacks Rank #1 (Strong Buy). URBN has a trailing four-quarter earnings surprise of 19.2%, on average. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Urban Outfitters’ current fiscal sales and EPS suggests growth of 6.6% and 83.4%, respectively, from the year-ago reported figure.

American Eagle Outfitters is a leading global specialty retailer offering on-trend clothing, accessories and personal care under its American Eagle and Aerie brands. The company sports a Zacks Rank #1.

The Zacks Consensus Estimate for American Eagle Outfitters’ current fiscal sales and EPS suggests growth of 2.2% and 33%, respectively, from the year-ago reported figure. AEO has a trailing four-quarter earnings surprise of 43.2%, on average.

Abercrombie & Fitch, a leading, global, omnichannel specialty retailer of apparel and accessories for men, women and kids, sports a Zacks Rank #1. The company delivered a trailing four-quarter earnings surprise of 724.8%, on average.

The Zacks Consensus Estimate for Abercrombie & Fitch’s current financial-year sales suggests growth of 10% from the year-ago period.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Abercrombie & Fitch Company (ANF) : Free Stock Analysis Report

American Eagle Outfitters, Inc. (AEO) : Free Stock Analysis Report

Urban Outfitters, Inc. (URBN) : Free Stock Analysis Report

Boot Barn Holdings, Inc. (BOOT) : Free Stock Analysis Report