Here's Why Deckers (DECK) Stock is Rallying Ahead of Industry

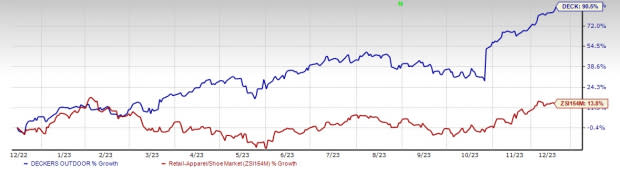

Deckers Outdoor Corporation DECK seems a promising pick now, thanks to its efforts related to product innovations, store expansion and enhancement of e-commerce capabilities. DECK’s focus on expanding its brand assortments, bringing a more innovative line of products and optimizing omnichannel distribution, bodes well. Buoyed by the aforesaid tailwinds, this major footwear and accessories designer’s shares have appreciated 90.5%, comfortably outperforming the industry’s 13.8% growth in the past year.

Analysts also seem quite optimistic about HOKA ONE ONE’s parent company. The Zacks Consensus Estimate for fiscal 2024 sales and earnings per share (EPS) is currently pegged at $4 billion and $23.42, respectively. These estimates show corresponding growth of 11.4% and 20.9% year over year. The consensus mark for next fiscal year’s sales and EPS is $4.4 billion and $26.44, respectively, reflecting a year-over-year increase of 9.3% and 12.9%.

Let’s Delve Deep

To resonate with the changing trends, Deckers is constantly developing its e-commerce portal to capture incremental sales. The company has made substantial investments to strengthen its online presence and improve shopping experience for customers. It is focused on opening smaller-concept omnichannel outlets and expanding programs such as Retail Inventory Online, Infinite UGG, Buy Online, Return In Store and Click and Collect to enhance customers’ shopping experience.

Additionally, Deckers, a Zacks Rank #2 (Buy) stock, is focused on product and marketing strategies that are more skewed toward customers. It has been implementing customer relationship management software and concentrating on the loyalty program. The company has been paying more emphasis on casual boots, winter and weather boots and casual shoes. It is selling directly to wholesale customers to capture incremental sales and margins.

Image Source: Zacks Investment Research

Markedly, the company has been witnessing solid momentum in its global wholesale business, driven by market share gains and robust consumer demand for UGG and HOKA ONE ONE brands in both domestic and international markets. During second-quarter fiscal 2024, its wholesale net sales increased 19.4% year over year to $760.2 million.

Deckers has been reaping the benefits of favorable trends and momentum across the HOKA ONE ONE direct-to-consumer (DTC) channel and broad-based UGG growth across regions and channels. In the fiscal second quarter, the company’s DTC business was the fastest-growing component of revenue growth, increasing 40% year over year, as HOKA ONE ONE and UGG brands witnessed more than 30% growth in consumer acquisition. DTC net sales advanced 38.8% while DTC comparable net sales surged 36.8% in the reported quarter.

The company’s HOKA ONE ONE brand continues to build its customer base through a combination of disruptive product innovation and a disciplined marketing approach. Greater acceptance of the UGG brand's diverse product line and strength in the international regions bode well. Deckers is progressing toward building HOKA into a multibillion-dollar major player and elevating UGG as a global lifestyle brand with diverse product offerings.

We believe that the company’s focus on ramping up inventory, optimizing channel mix to fulfill consumer demand, scaling production to support brands and implementing price increases should position it well for growth. Given all the aforesaid tailwinds, we believe Deckers will continue to perform well on the bourses.

Eye These Other Solid Picks

Some other top-ranked companies are G-III Apparel Group GIII, Royal Caribbean RCL and lululemon athletica LULU.

G-III Apparel sports a Zacks Rank #1 (Strong Buy), at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

GIII Apparel has a trailing four-quarter earnings surprise of 541.8%, on average. The Zacks Consensus Estimate for GIII’s fiscal 2024 EPS indicates an increase of 33% from the year-ago period’s reported level.

Royal Caribbean sports a Zacks Rank of 1, at present. RCL has a trailing four-quarter earnings surprise of 28.3%, on average.

The Zacks Consensus Estimate for RCL’s 2023 sales and EPS indicates increases of 57.7% and 187.9%, respectively, from the year-ago period’s reported levels.

lululemon athletica is a yoga-inspired athletic apparel company. LULU carries a Zacks Rank #2, at present.

The Zacks Consensus Estimate for lululemon athletica’s current financial-year sales and EPS suggests growth of 18.2% and 22.8%, respectively, from the year-ago corresponding figures. LULU has a trailing four-quarter earnings surprise of 9.2%, on average.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Royal Caribbean Cruises Ltd. (RCL) : Free Stock Analysis Report

Deckers Outdoor Corporation (DECK) : Free Stock Analysis Report

lululemon athletica inc. (LULU) : Free Stock Analysis Report

G-III Apparel Group, LTD. (GIII) : Free Stock Analysis Report