Here's Why First BanCorp (FBP) Stock is Worth Betting on

Though the U.S. regional banking crisis earlier this year hurt investor sentiments and turned them bearish on the sector, they have regained some confidence. Further, several new macroeconomic data indicate that the Federal Reserve is done rising rates this cycle. Hence, First BanCorp. FBP stock looks like an attractive investment option now.

Supported by higher interest rates and decent loan demand, FBP’s top line is expected to improve in the near term. Analysts are optimistic regarding the company’s earnings potential. The Zacks Consensus Estimate for FBP’s earnings has been revised 5.9% and 1.9% upward for 2023 and 2024, respectively, over the past two months. It currently carries a Zacks Rank #2 (Buy).

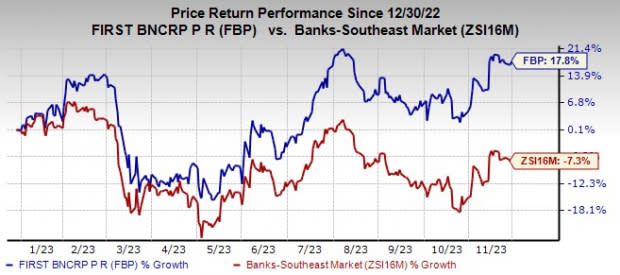

Shares of First BanCorp have gained 17.8% so far this year against the industry’s 7.3% decline.

Image Source: Zacks Investment Research

Mentioned below are some factors that make First BanCorp a stock a solid pick right now.

Earnings Growth: In the last three to five years, First BanCorp witnessed earnings growth of 31%, higher than the industry’s average of 9.4%. The trend is expected to continue in the near- term, with earnings projected to rise 1.3% in 2023.

Also, FBP has an impressive earnings surprise history. The company’s earnings surpassed the Zacks Consensus Estimate in three of the trailing four quarters, with the average beat being 8.94%.

Revenue Strength: First BanCorp’s revenues witnessed a CAGR of 8.7% over the last five years (2018-2022), with the upward trend continuing in the first three quarters of 2023. Revenues are expected to keep improving in the near term. In 2023 and 2024, the company’s top line is expected to witness growth of 2.7% and 1.4%, respectively.

Solid Capital Distributions: FBP has been raising dividend payouts on a regular basis. In the last five years, the company hiked dividends five times. The last increase of 16.7% to 14 cents per share was announced in February 2023.

Also, First BanCorp has a share repurchase plan in place. In July, the company announced a new share repurchase program of up to $225 million, effective till Sep 30, 2024. In the first nine months of 2023, it repurchased almost 9 million shares for $125 million under its previous plan that authorized the buyback of $350 million worth of shares.

Given the company’s decent liquidity and balance sheet position, its capital distributions seem sustainable going forward.

Superior Return on Equity (ROE): First BanCorp’s ROE of 21.55% is higher than the industry average of 11.04%. This shows that it reinvests its cash more efficiently than its peers.

Favorable Valuation: First BanCorp has a Value Score of B. The Value Style Score condenses all valuation metrics into one actionable score, helping investors steer clear of 'value traps' and identify stocks that are truly trading at a discount. Our research shows that stocks with a Value Score of A or B, when combined with a Zacks Rank #1 (Strong Buy) or 2, offer the best upside potential.

Other Bank Stocks Worth Considering

A couple of other top-ranked stocks from the banking space are Hilltop Holdings HTH and Byline Bancorp BY.

Earnings estimates for HTH have been revised 4.5% upward for 2023 over the past 30 days to $1.62. The company’s shares have gained almost 1% over the past six months. Hilltop currently carries a Zacks Rank #2. You can see the complete list of today’s Zacks #1 Rank stocks here.

Byline Bancorp’s earnings estimates have been revised 2.2% north for the current year to $2.79 over the past 30 days. In six months’ time, BY’s shares have rallied 14.2%. The company carries a Zacks Rank #2 at present.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Hilltop Holdings Inc. (HTH) : Free Stock Analysis Report

First BanCorp. (FBP) : Free Stock Analysis Report

Byline Bancorp, Inc. (BY) : Free Stock Analysis Report