Here's Why You Should Hold on to Baker Hughes (BKR) Stock Now

Baker Hughes Company BKR has witnessed upward earnings estimate revisions for 2023 and 2024 in the past 60 days.

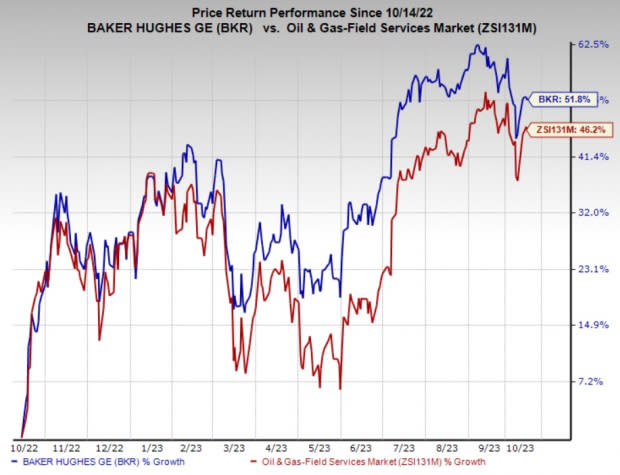

The company, currently carrying a Zacks Rank #3 (Hold), has gained 51.8% in the past year compared with 46.2% growth of the composite stocks belonging to the industry.

Image Source: Zacks Investment Research

What’s Favoring the Stock?

The West Texas Intermediate (WTI) crude oil is currently trading at around $84 per barrel, creating a favorable environment for exploration and production endeavors.

Strong oil prices will likely pave the way for rig additions despite a slowdown in drilling activities, as upstream energy players mainly focus on stockholder returns rather than boosting production.

Higher exploration and production activities will drive greater demand for oilfield service providers, such as Baker Hughes. For 2023, the company anticipates revenues of $15.1-$15.7 billion from its Oilfield Services and Equipment unit, marking an upturn from the $13.2 billion reported in 2022.

Apart from its significant role in the upstream markets, Baker Hughes is recognized as a leader in the liquefied natural gas (LNG) sector. With expectations of strong growth in LNG demand, particularly driven by Europe and Asia, the company envisions a continued rise in LNG demand over the next several years. The oilfield service player expects to receive massive orders for LNG equipment this year.

Baker Hughes has been a reliable dividend payer in the past two years. When compared to the composite stocks within the industry, the company has consistently provided higher dividend yields during this same period.

Baker Hughes boasts a robust financial position with a strong balance sheet. Over the past two years, BKR has consistently maintained a lower debt-to-capitalization ratio compared with the composite stocks within the industry.

Given these tailwinds, Baker Hughes, one of the leading oilfield service players in the United States, is poised for an upside in the coming days.

Risks

Oil and gas companies are highly exposed to commodity price fluctuations, thereby making business for oilfield service providers extremely volatile. This is because oilfield service players like Baker Hughes help upstream energy players efficiently set up oil and gas wells. Baker Hughes’ beta of 1.50 further confirms that the company experiences greater volatility than the broader market.

Stocks to Consider

Investors interested in the energy sector may look at some better-ranked companies mentioned below. The three companies presently sport a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

USA Compression Partners USAC is a leading energy infrastructure provider, which specializes in large-horsepower applications. The stability in cash flow for USA Compression Partners has enabled it to maintain a steady quarterly distribution of 52.50 cents since the second quarter of 2015.

USA Compression Partners has witnessed upward earnings estimate revisions for 2023 and 2024 in the past 30 days. The consensus estimate for USAC’s 2023 and 2024 earnings per share is pegged at 30 cents and 58 cents, respectively.

Matador Resources Company MTDR is among the leading oil and gas explorers in the shale and unconventional resources in the United States. MTDR’s prime priorities include lowering debt, delivering free cashflows and maintaining or increasing dividends.

Matador Resources has witnessed upward earnings estimate revisions for 2023 and 2024 in the past seven days. The consensus estimate for MTDR’s 2023 and 2024 earnings per share is pegged at $6.40 and $8.64, respectively.

Pioneer Natural Resources Company PXD is an explorer and producer of oil, natural gas and natural gas liquid. The upstream energy player’s debt to capitalization has been persistently lower than the industry over the past few years, reflecting considerably lower debt exposure.

Pioneer has witnessed upward earnings estimate revisions for 2023 and 2024 in the past seven days. The consensus estimate for PXD’s 2023 and 2024 earnings per share is pinned at $21.42 and $25.27, respectively.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Pioneer Natural Resources Company (PXD) : Free Stock Analysis Report

USA Compression Partners, LP (USAC) : Free Stock Analysis Report

Baker Hughes Company (BKR) : Free Stock Analysis Report

Matador Resources Company (MTDR) : Free Stock Analysis Report