Here's Why You Should Hold on to Emerson (EMR) Stock for Now

Emerson Electric Co. EMR is poised for growth on the back of solid demand across the process and hybrid markets, and improving supply chains despite headwinds from rising cost of sales, restructuring expenses and adverse foreign currency movements.

Let’s delve deeper to unearth the factors that are aiding this Zacks Rank #3 (Hold) company.

Business Strength: Strong demand in the process and hybrid markets is boosting underlying EMR’s orders (up 3% in the fiscal third quarter). The company anticipates double-digit sales growth for the process end market in 2023, driven by growth in energy transition and energy security. For hybrid, the company expects a low double-digit increase in sales due to strength in the life sciences, metals and mining markets.

A robust demand environment and improving supply chains are supporting underlying sales growth (up 14% in the fiscal third quarter). Within the Intelligent Devices business unit, the company is seeing strength in the measurement and analytical, and final control businesses due to strong demand in the hybrid and process end markets. Revenues from the unit increased 7% year over year in the first nine months of fiscal 2023. Improved supply chains, easier availability of electronic components, and strong backlogs are driving growth of the Software and Control business group. Revenues from the unit jumped 27% year over year in the first nine months of fiscal 2023.

Given the strength across its end markets, Emerson has raised its fiscal 2023 guidance. For fiscal 2023, the company expects net sales to increase 10.5% compared with a rise of 9-10.5% predicted earlier. Underlying sales are expected to increase approximately 10% compared with 8.5-10% rise estimated earlier. Adjusted earnings per share are predicted to be between $4.40 and $4.45 compared with $4.15–$4.25 forecasted earlier.

Expansion Initiatives: Acquisitions have been Emerson's preferred mode of business expansion so far. In August, the company announced two separate deals to acquire Afag and Flexim. The acquisition of Afag will expand Emerson’s capabilities in factory automation, helping the company expand into lucrative end markets — battery manufacturing, automotive, packaging, medical, life sciences and electronics — currently served by Afag. The acquisition of Flexim will add to EMR’s existing flow measurement positions in coriolis, differential pressure, magmeter and vortex flow measurement and expand its automation portfolio and measurement capabilities. Both acquisitions are expected to close by the end of Emerson’s fiscal 2023.

Emerson’s move to acquire National Instruments in an $8.2 billion deal is aligned with its focus on global automation to drive growth and profitability. The acquisition, expected to be completed in the first half of fiscal 2024, will strengthen EMR’s global automation foothold, helping the company expand into high-growth end markets, including semiconductor and electronics, transportation and electric vehicles and aerospace and defense.

Apart from expanding automation capabilities, the acquisition will open up industrial software opportunities for EMR. Emerson expects the transaction to generate cost savings of $165 million by the end of the fifth year upon completion. The buyout is expected to be immediately accretive to EMR’s adjusted earnings. The acquisition will also generate significant recurring revenues and improve EMR’s gross margins.

Rewards to Shareholders: Strong cash flows (free cash flow was up 47% in the first nine months of fiscal 2023) allow Emerson to effectively deploy capital to repurchase shares and pay out dividends. In the first nine months of fiscal 2023, the company paid dividends of $900 million. In the first quarter of fiscal 2023, EMR had completed its target to buyback $2 billion worth of shares in fiscal 2023. For 2023, the company expects to pay out dividends of approximately $1.2 billion. The company expects free cash flow of $2.2-$2.3 billion for fiscal 2023.

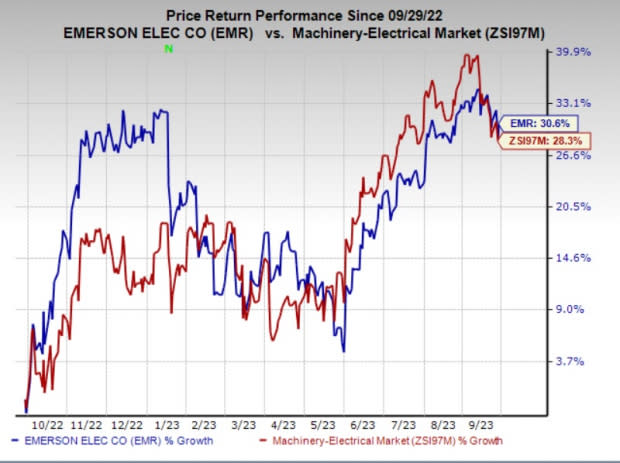

Price Performance: Backed by the abovementioned tailwinds, Emerson’s shares have outperformed its industry in a year. The stock gained 30.6% in a year compared with the industry’s 28.3% increase.

Image Source: Zacks Investment Research

Stocks to Consider

Some better-ranked stocks within the broader Industrial Products sector are as follows:

Flowserve Corporation FLS presently sports a Zacks Rank #1 (Strong Buy). The company pulled off a trailing four-quarter earnings surprise of 6.2%, on average. You can see the complete list of today’s Zacks #1 Rank stocks.

Flowserve has an estimated earnings growth rate of 79.1% for the current year. The stock has jumped 29.2% so far this year.

Graham Corporation GHM currently flaunts a Zacks Rank #1. The company pulled off a trailing four-quarter earnings surprise of 243.1%, on average.

Graham has an estimated earnings growth rate of 400% for the current fiscal year. The stock has rallied 65% so far this year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Emerson Electric Co. (EMR) : Free Stock Analysis Report

Flowserve Corporation (FLS) : Free Stock Analysis Report

Graham Corporation (GHM) : Free Stock Analysis Report