Here's Why You Should Hold EverQuote (EVER) in Your Portfolio

EverQuote, Inc. EVER is well-poised to grow from reduced operating expenses, the enhancement of its platform via machine learning and artificial intelligence and expected recovery in the auto insurance business.

Earnings Surprise History

EverQuote has a decent earnings surprise history. Its bottom line beat estimates in each of the last four quarters, the average being 29.72%.

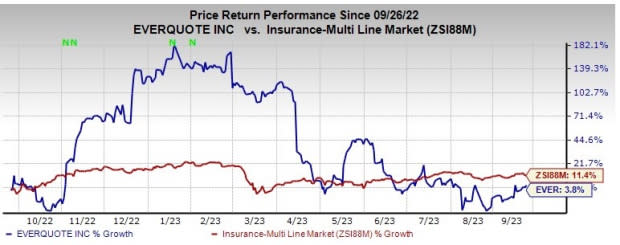

Zacks Rank & Price Performance

EVER currently carries a Zacks Rank #3 (Hold). In the past one year, the stock has gained 3.8% compared with the industry’s increase of 11.4%.

Image Source: Zacks Investment Research

Business Tailwinds

EVER remains focused on rapidly expanding into new verticals. Growth in overall consumer quote requests should benefit EverQuote as it reflects the insurer’s success in generating consumer traffic and the potential to increase the share of insurance-shopping consumers.

Variable marketing margin (VMM) is likely to gain from declining customer acquisition costs and a shift of revenue mix to local agent networks with higher VMM. The company also decided to reduce its non-marketing operating expenses by 15%. This is expected to drive an improvement in the VMM operating point for the business.

Increasing consumer traffic, higher quote request volume and innovating advertiser products and services will continue to boost revenues.

EverQuote boasts a debt-free balance sheet with cash balance improving over the last three years. The insurer aims to meet any future debt service obligations with the existing cash and cash equivalents and cash flows from operations, which are expected to be sufficient to fund operating expenses and capital expenditure requirements for at least the next 12 months, without considering liquidity available from the revolving line of credit.

However, EverQuote's top line has been decreasing over the past few quarters owing to the auto insurance downturn since 2021. The company expects revenues between $51 million and $56 million in the third quarter, implying a year-over-year decline of 48% from the midpoint. However, the company’s expectation of insurance premium increases and improving the profitability of insurance carriers should fuel its top-line growth in the near future due to higher demand for customer acquisition. Moreover, the cost of claims shows signs of stabilization, improving the prospects for EVER and the auto insurance industry.

EVER also has an impressive Growth Score of B. This style score helps analyze the growth prospects of a company.

Stocks to Consider

Some better-ranked stocks from the insurance industry are Old Republic International Corporation ORI, Lemonade, Inc. LMND and Radian Group Inc. RDN. While Old Republic International sports a Zacks Rank #1 (Strong Buy), Lemonade and Radian Group carry a Zacks Rank #2 (Buy) each at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Old Republic International’s earnings surpassed estimates in each of the last four quarters, the average earnings surprise being 29.85%.

The Zacks Consensus Estimate for ORI’s 2023 and 2024 earnings has moved 8.3% and 5.2% north, respectively, in the past 60 days. In the past year, the insurer has gained 34.2%.

Lemonade’s earnings surpassed estimates in three of the last four quarters and missed in one, the average earnings surprise being 10.57%.

The Zacks Consensus Estimate for LMND’s 2023 and 2024 earnings implies 20.9% and 16% year-over-year growth, respectively. In the past year, the insurer has lost 42.8%.

Radian’s earnings surpassed estimates in each of the last four quarters, the average earnings surprise being 30.88%.

The Zacks Consensus Estimate for RDN’s 2023 and 2024 earnings has moved 5.7% and 4% north, respectively, in the past 60 days. In the past year, the insurer has gained 32%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Radian Group Inc. (RDN) : Free Stock Analysis Report

EverQuote, Inc. (EVER) : Free Stock Analysis Report

Old Republic International Corporation (ORI) : Free Stock Analysis Report

Lemonade, Inc. (LMND) : Free Stock Analysis Report