Here's Why You Should Hold Onto Albemarle (ALB) Stock for Now

Albemarle Corporation ALB is benefiting from higher lithium volumes on strong demand, capacity expansion and productivity actions amid headwinds from the weakness in the specialties unit.

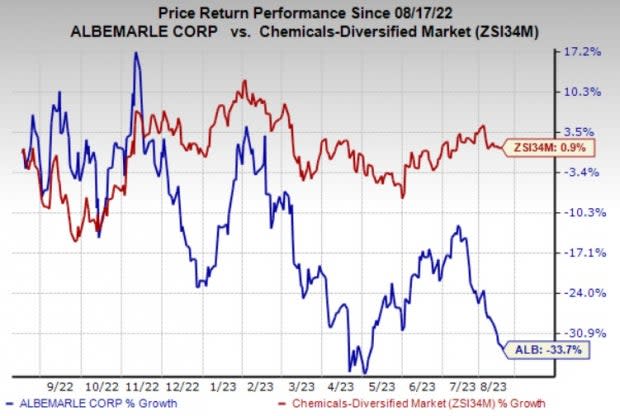

Shares of Albemarle are down 33.7% over a year compared with a 0.9% rise of the industry.

Image Source: Zacks Investment Research

Let’s find out why this Zacks Rank #3 (Hold) stock is worth retaining at the moment.

Strong Lithium Demand, Expansion Moves to Drive Results

The North Carolina-based company is gaining from higher volumes in its lithium business. Increased customer demand, capacity expansion and improvements in plant productivity are contributing to higher volumes.

Albemarle saw higher volumes in the Energy Storage unit in the second quarter of 2023, primarily driven by the expansion of La Negra III/IV in Chile and a surge in tolling volumes to meet the growing demand from customers. Production from the processing plant in Qinzhou, China also contributed to the volume growth.

Albemarle is also benefiting from cost-saving and productivity initiatives. It sees $250 million in productivity benefits over 2023 and 2024 through operational discipline. The company’s cost actions are expected to support its margins in 2023.

The company is also strategically executing its projects aimed at boosting its global lithium conversion capacity. It remains focused on investing in high-return projects to drive productivity. The company is well placed to gain from long-term growth in the battery-grade lithium market.

Albemarle's Kemerton I lithium hydroxide conversion plant in Western Australia achieved first product in July 2022. Kemerton II is also progressing through the commissioning phase. Kemerton III and IV projects have also been moved into execution. Moreover, the Qinzhou plant in China will also boost the growth of conversion capacity and drive lithium volumes. Mechanical completion of the Meishan facility is also expected in early 2024. The Salar yield improvement project has also moved into the commissioning phase.

Softness in Specialties Ails

The company’s Specialties unit is exposed to headwinds from demand weakness. Sales from the segment tumbled around 20% year over year in the second quarter, hurt by lower volumes and pricing related to weakness in certain end markets.

The segment faces demand headwinds in consumer and industrial electronics and elastomers markets. The demand weakness is expected to continue in the third quarter of 2023. Albemarle has reduced its adjusted EBITDA outlook for the segment for 2023 factoring in the demand softness.

Albemarle Corporation Price and Consensus

Albemarle Corporation price-consensus-chart | Albemarle Corporation Quote

Stocks to Consider

Albemarle currently carries a Zacks Rank #3 (Hold).

Better-ranked stocks worth a look in the basic materials space include Carpenter Technology Corporation CRS, PPG Industries, Inc. PPG and Universal Stainless & Alloy Products, Inc. USAP.

The Zacks Consensus Estimate for current fiscal-year earnings for CRS is currently pegged at $3.48, implying year-over-year growth of 205.3%. Carpenter Technology currently carries a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Carpenter Technology has a trailing four-quarter earnings surprise of roughly 10%, on average. The stock has rallied around 55% in a year.

PPG Industries currently carries a Zacks Rank #2 (Buy). The Zacks Consensus Estimate for PPG's current-year earnings has been revised 3.6% upward over the past 60 days.

PPG Industries’ earnings beat the Zacks Consensus Estimate in three of the last four quarters. It has a trailing four-quarter earnings surprise of roughly 7.3%, on average. PPG shares have gained around 4% in a year.

Universal Stainless & Alloy Products currently carrying a Zacks Rank #2. It has a projected earnings growth rate of 160.8% for the current year.

The Zacks Consensus Estimate for USAP's current-year earnings has been revised 181% upward over the past 60 days. USAP shares are up around 63% in a year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

PPG Industries, Inc. (PPG) : Free Stock Analysis Report

Carpenter Technology Corporation (CRS) : Free Stock Analysis Report

Albemarle Corporation (ALB) : Free Stock Analysis Report

Universal Stainless & Alloy Products, Inc. (USAP) : Free Stock Analysis Report