Here's Why You Should Hold Onto DuPont (DD) Stock for Now

DuPont de Nemours, Inc. DD is expected to benefit from its innovation-driven investment, productivity and pricing actions and the Spectrum Plastics Group acquisition amid certain challenges including weaker demand in specific businesses.

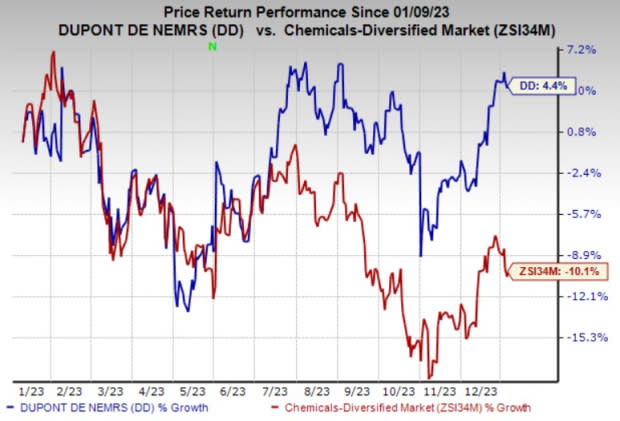

The company’s shares are up 4.4% over a year against a 10.1% decline of its industry.

Image Source: Zacks Investment Research

Let’s find out why this Zacks Rank #3 (Hold) stock is worth retaining at the moment.

Productivity, Innovation & Spectrum Buyout to Aid Results

DuPont remains focused on driving growth though innovation and new product development. Its innovation-driven investment is focused on several high-growth areas. DD remains committed to drive returns from its R&D investment.

The company, in August 2023, completed the buyout of leading manufacturer of specialty medical devices and components, Spectrum Plastics Group from AEA Investors for $1.75 billion. The acquired business, with annual sales of around $500 million, has been integrated into the industrial solutions line of business within the Electronics & Industrial segment.

The acquisition strengthens DuPont’s existing position in stable and fast-growing healthcare end markets. It is also in sync with its focus on high-growth, customer-driven innovation for the healthcare market. The addition of Spectrum is expected to boost revenues in the Electronics & Industrial segment.

Moreover, DuPont is benefiting from cost synergy savings and productivity improvement actions. Its structural cost actions are contributing to its bottom line. DD also continues to implement strategic price increases in the wake of cost inflation. These actions are likely to support its results. DuPont is also planning additional restructuring actions and expects savings from these actions to be realized from the first quarter of 2024.

The company is also managing its portfolio with an aim for value creation. It is divesting non-core assets to focus more on high-growth, high-margin businesses.

Weakness in Water Business a Concern

DuPont’s water business is exposed to headwinds from the slowdown in China. Its water solutions business is likely to see sales moderation in the fourth quarter of 2023 due to softer demand in China resulting from the slowdown in the industrial economy and inventory de-stocking.

The softness in construction end markets is also expected to impact the shelter solutions business within the Water & Protection segment. Also, customer de-stocking in shelter solutions is expected to continue in the fourth quarter.

While the company is seeing a recovery in Interconnect Solutions, the business is expected to continue to be impacted by reduced consumer electronics spending in the near term. Interconnect Solutions witnessed an 11% year-over-year decrease in organic sales in the third quarter, partly driven by reduced consumer electronics volumes and inventory de-stocking. Softer smartphone, personal computing and tablet demand is likely to weigh on volumes in this business in the fourth quarter.

DuPont de Nemours, Inc. Price and Consensus

DuPont de Nemours, Inc. price-consensus-chart | DuPont de Nemours, Inc. Quote

Stocks to Consider

Better-ranked stocks worth a look in the basic materials space include, Cameco Corporation CCJ, Koppers Holdings Inc. KOP and Quaker Chemical Corporation KWR.

Cameco has a projected earnings growth rate of 156% for the current year. The Zacks Consensus Estimate for CCJ’s current-year earnings has been revised upward by 6.7% over the past 60 days. The stock is up around 70% in a year. CCJ currently carries a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

In the past 60 days, the consensus estimate for Koppers’ current-year earnings has been revised upward by 0.7%. KOP, carrying a Zacks Rank #2 (Buy), beat the Zacks Consensus Estimate in each of the last four quarters, with the average earnings surprise being 22.3%. The company’s shares have surged around 61% in the past year.

Quaker Chemical, carrying a Zacks Rank #2, has a projected earnings growth rate of 28.3% for the current year. KWR has a trailing four-quarter earnings surprise of roughly 16.7%, on average. KWR shares have gained 14% in a year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

DuPont de Nemours, Inc. (DD) : Free Stock Analysis Report

Cameco Corporation (CCJ) : Free Stock Analysis Report

Koppers Holdings Inc. (KOP) : Free Stock Analysis Report

Quaker Houghton (KWR) : Free Stock Analysis Report